@Plasma One:

The Debit Card That Actually Makes Sense

How #Plasma is Turning Crypto Into Cash (While Paying You 10% to Hold It)

Your bank account pays you 0.39% interest. Maybe 4-5% if you've hunted down one of those "high-yield" savings accounts everyone talks about. Meanwhile, inflation quietly eats away 2-3% of your purchasing power every year. You're not earning money. You're losing it in slow motion.

Now imagine this instead: Your checking account pays you 10%+ interest. You earn 4% cash back on everything you buy - groceries, coffee, gas, rent. You can send money to anyone, anywhere in the world, instantly, for free. And you can spend your balance with a regular debit card at 150+ million merchants globally, just like any other Visa card.

This isn't a credit card scheme with hidden fees. It's not a promotional rate that expires in 6 months. It's Plasma One - the world's first stablecoin-native neobank - and it's changing what "everyday banking" actually means.

The Banking Math That Doesn't Add Up

Let's be honest about traditional banking. The entire model is built to extract value from you, not create it for you.

As of February 2026, here's what "good" banking looks like:

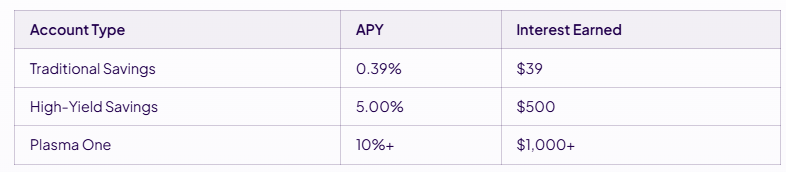

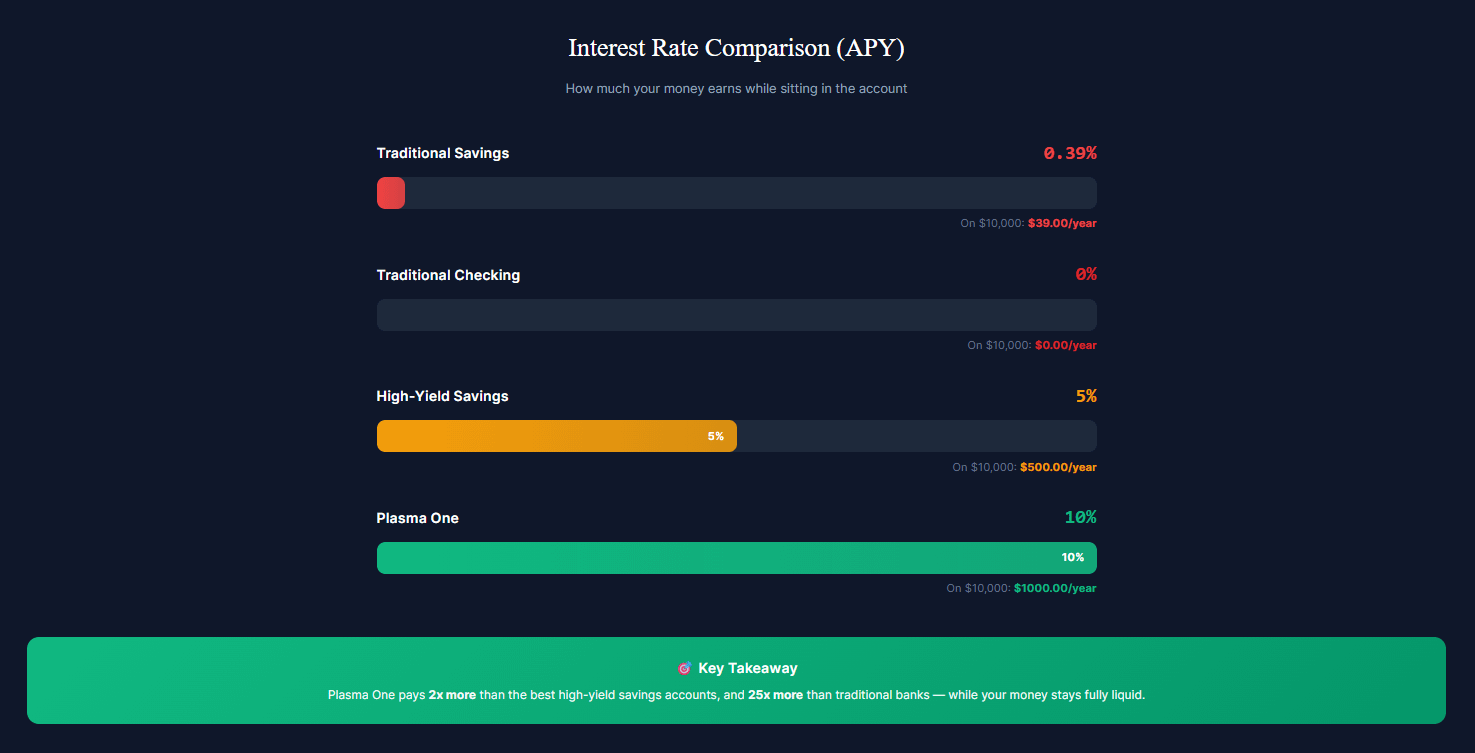

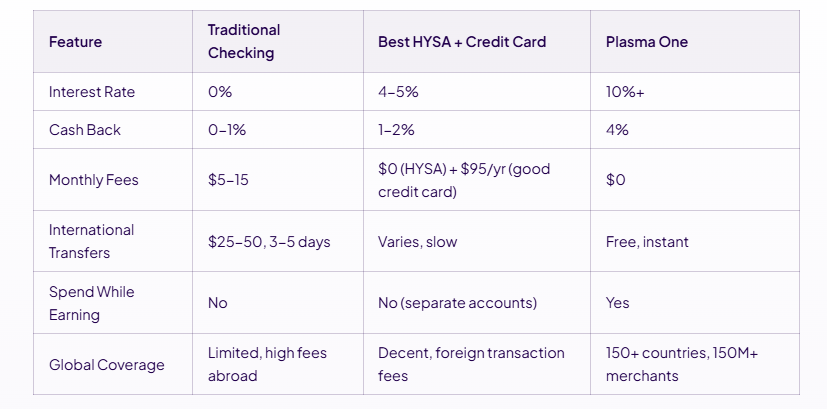

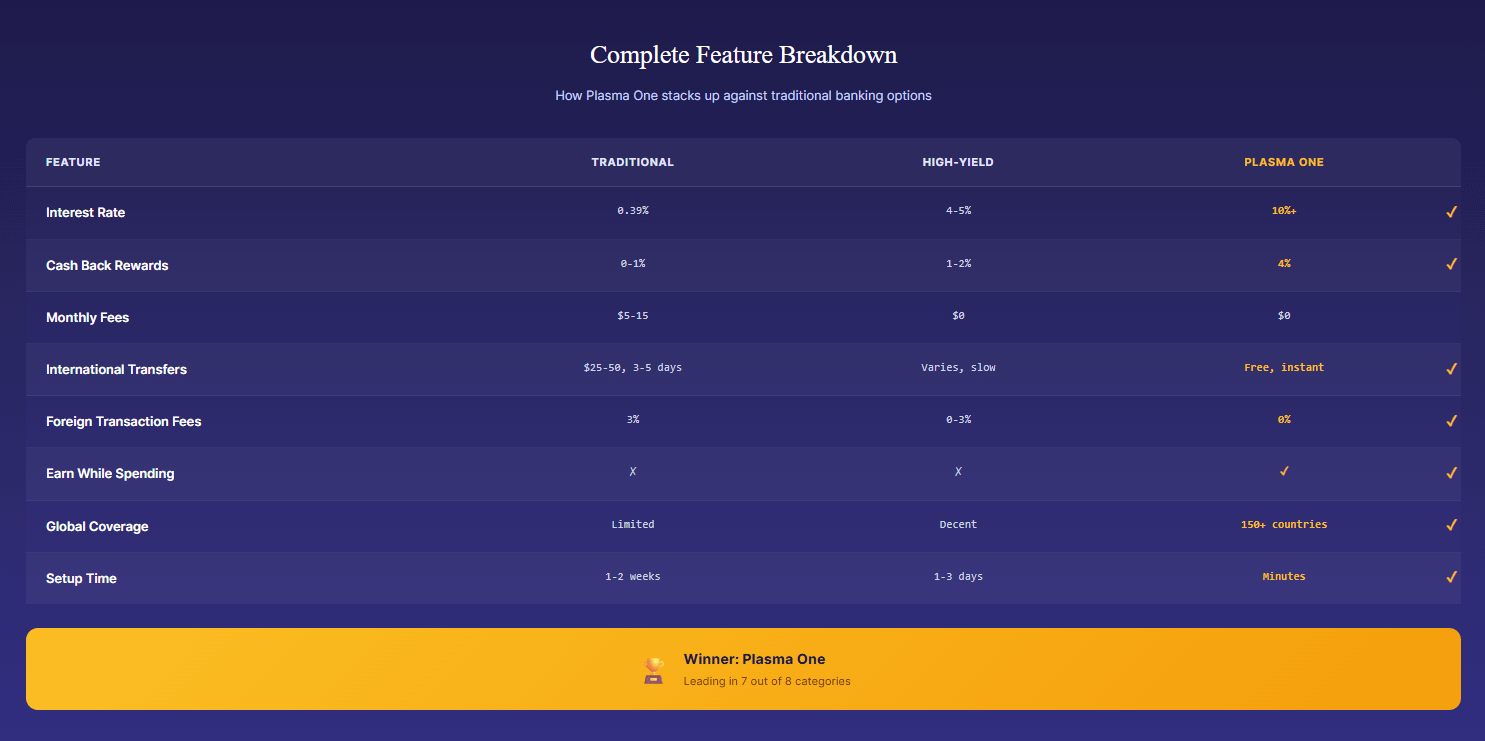

Traditional Savings: 0.01% - 0.39% APY (basically nothing)

"High-Yield" Savings: 4.00% - 5.00% APY (if you're lucky and shop around)

Checking Account: 0% APY (your money just sits there)

Debit Card Rewards: 1% cash back if you're lucky, usually 0%

International Transfers: $25-50 fees, 3-5 business days, terrible exchange rates

Monthly Fees: $5-15 unless you maintain minimum balances

Meanwhile, your bank takes your deposits and lends them out at 7-8% for mortgages, 12-18% for auto loans, and 20-30% for credit cards. You do all the work of earning and saving money. They pocket the spread. You get crumbs.

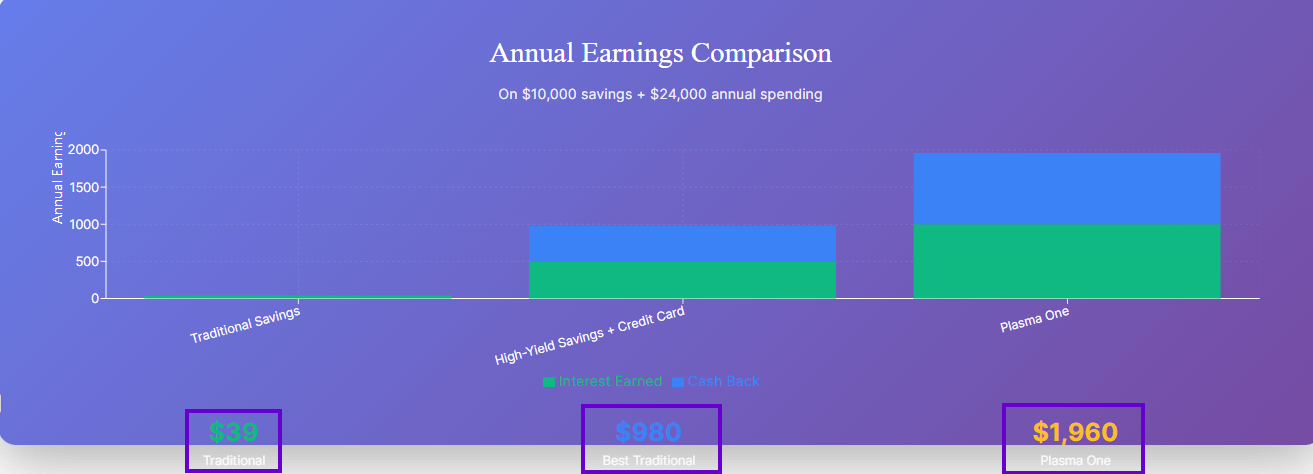

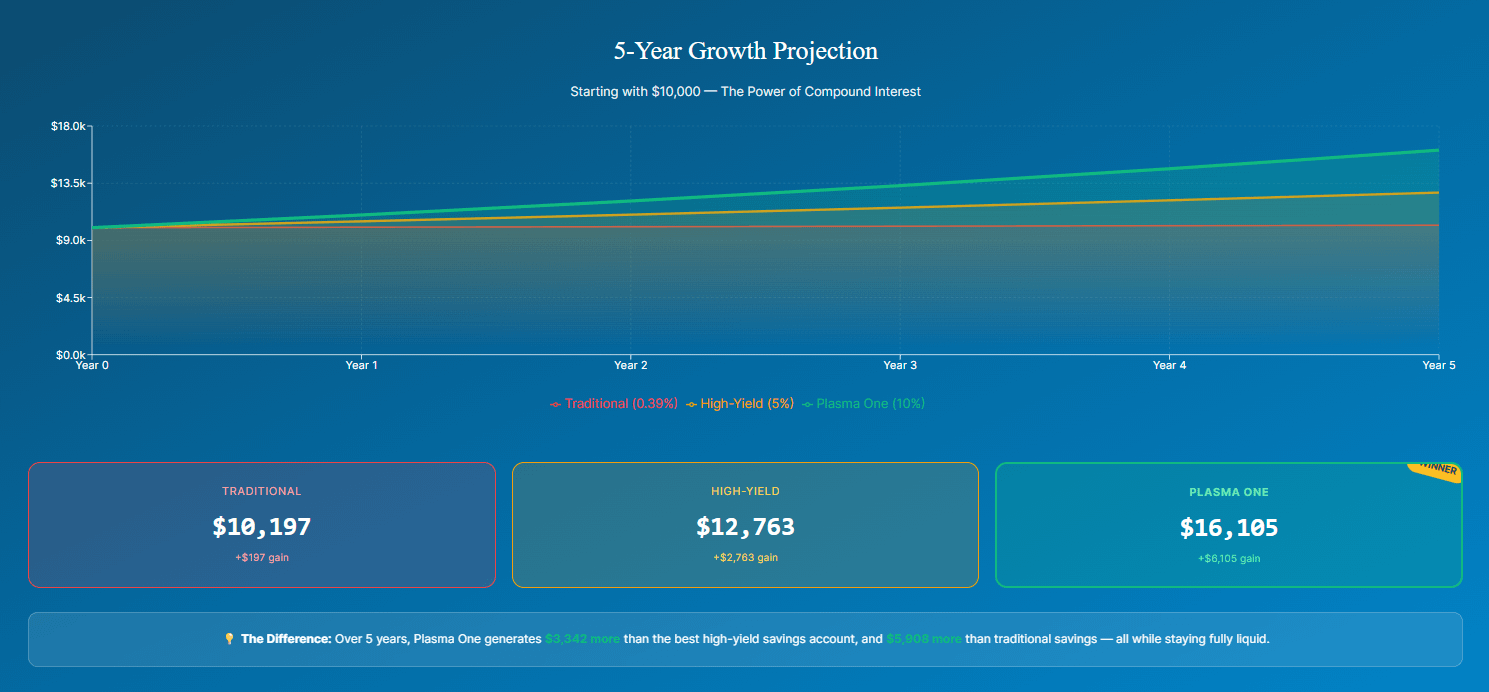

Let's do the math on $10,000 sitting in your account for one year:

That's the difference. And this is before we talk about the 4% cash back you're earning every time you spend. If you put $2,000/month through your Plasma One card for daily expenses, that's an additional $960/year just for buying the things you were going to buy anyway.

Total potential earnings: $1,000 (yield) + $960 (cash back) = $1,960 per year. On $10,000 in savings and $24,000 in annual spending. That's real money.

What Actually Is Plasma One?

Plasma One is what happens when you rebuild banking from scratch using stablecoins instead of traditional bank accounts. It's a mobile app with both virtual and physical Visa debit cards that let you hold, spend, and earn on digital dollars (USDT initially, expanding to other stablecoins).

Here's what you get:

10%+ Yield: Your balance earns yield automatically through Plasma's on-chain DeFi ecosystem. No lockup periods, no minimum balances, no "promotional rates" that expire.

4% Cash Back: Every purchase you make with your Plasma One card earns up to 4% back in XPL tokens (Plasma's native token). Groceries, gas, coffee, rent - everything.

Zero-Fee Transfers: Send USDT to anyone else on Plasma One instantly for free. No wire fees, no ACH delays, no "processing times."

Global Spending: Use your card at 150+ million merchants in over 150 countries. It works everywhere Visa is accepted - online and in-store.

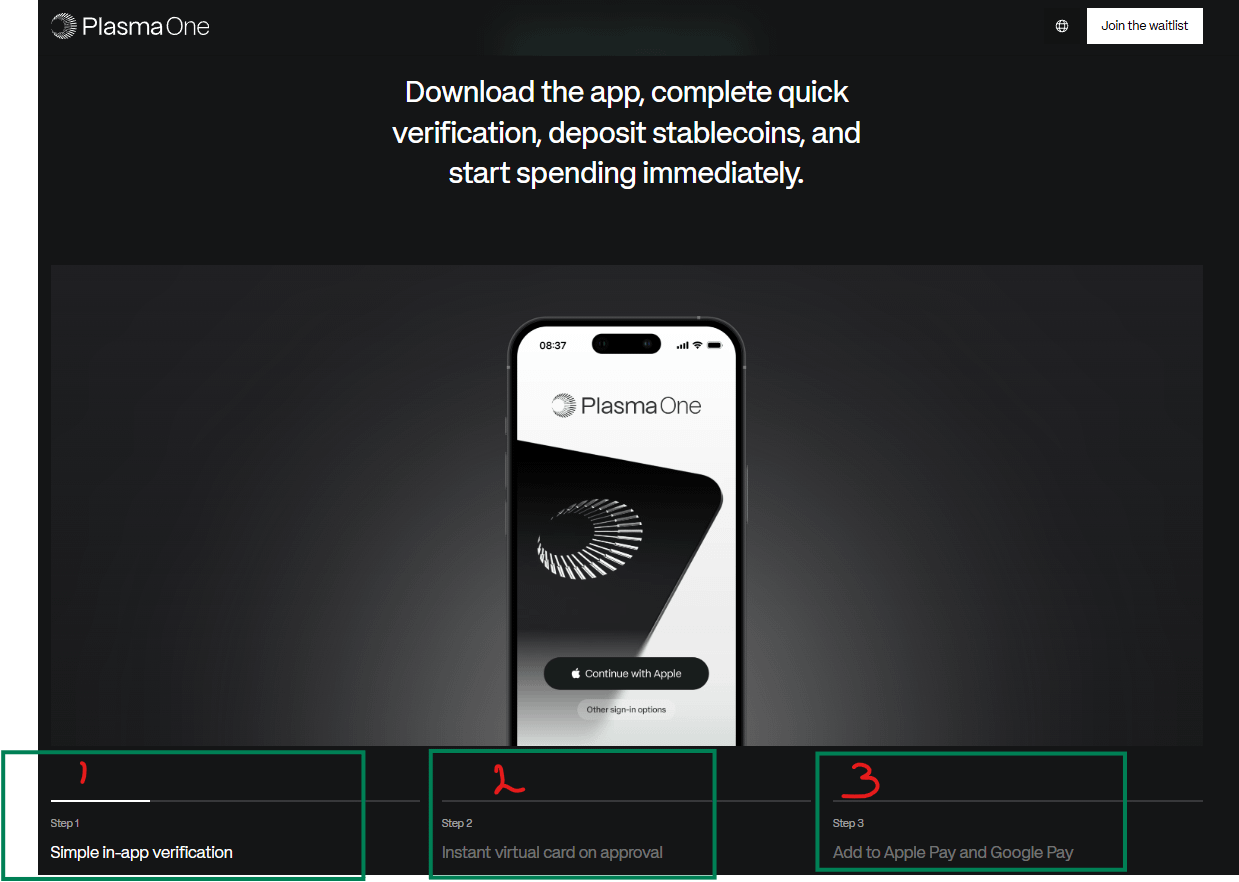

Instant Onboarding: Sign up, complete verification, and get a virtual card in minutes. Physical card ships shortly after.

Bank Withdrawals: You can still off-ramp to traditional bank accounts when needed. Timing and fees depend on your region and partner.

The card is issued by Signify Holdings via Visa, so from the merchant's perspective, it's just a normal Visa debit card. But on the backend, you're spending directly from your stablecoin balance, which is earning yield 24/7.

The Real Genius: Spend While You Earn

This is where Plasma One breaks the traditional banking model entirely. With a normal checking account, your money earns nothing. With a savings account, you earn interest but can't easily spend it (and if you make too many withdrawals, you get hit with fees).

Plasma One collapses these two accounts into one. Your balance is always earning 10%+ yield, even when you're actively spending from it. Pay for coffee with your Plasma One card? The remaining balance is still earning interest. Transfer rent to your landlord? Still earning. Buy groceries? Still earning.

There's no separation between "money I'm using" and "money that's earning interest." All of it does both, all the time.

And because the yield comes from Plasma's on-chain ecosystem (not promotional gimmicks or bank marketing), it's sustainable. The blockchain itself is optimized for stablecoin transactions with ultra-low fees. DeFi strategies on Plasma are more efficient because everything is built around non-volatile assets (stablecoins) rather than volatile crypto.

Who Is This Actually For?

The honest answer: almost everyone who has money sitting in a bank account right now. But let's get specific about who benefits most:

1. Anyone With an Emergency Fund

Financial advisors tell you to keep 3-6 months of expenses in a savings account for emergencies. That's smart advice. But if you're following it, you probably have $5,000 - $20,000 sitting in an account earning basically nothing.

With Plasma One, that emergency fund is still completely liquid (you can spend it instantly with your card or transfer it out), but it's earning 10%+ while it sits there. On $15,000, that's $1,500/year instead of $60.

2. Digital Nomads & Remote Workers

If you're earning in dollars but spending across multiple countries, Plasma One is a game-changer. No foreign transaction fees (those hidden 3% charges your credit card hits you with). No terrible exchange rates. No "this card doesn't work in this country" surprises.

Works in Istanbul, Dubai, Buenos Aires, Tokyo, wherever. 150+ countries, 150+ million merchants. And you're earning yield in dollars regardless of where you are.

3. People Sending Money Internationally

If you regularly send money to family abroad, you know the pain: Western Union takes 7-10%, wire transfers cost $25-50 and take days, PayPal international eats 4-5% in fees.

Plasma One? Zero fees. Instant settlement. If the recipient also has Plasma One, the money arrives in seconds for free. If they don't, you can still off-ramp to their local bank - still cheaper and faster than traditional methods.

4. Crypto-Curious But Skeptical

Maybe you've heard about crypto but don't want to deal with volatile assets, complicated wallets, seed phrases, and gas fees. Fair enough.

Plasma One gives you the benefits of blockchain technology (instant transfers, high yields, global access) without the complexity. Your balance is in USDT - a stablecoin pegged 1:1 to the US dollar. No price volatility. No confusing wallet management. Just a simple app and a debit card that works like any other.

Security is handled with biometric sign-in and hardware-backed keys instead of seed phrases. You can freeze your card instantly from the app. Set spending limits. Get real-time transaction alerts. It's simpler than most traditional banking apps.

The Catch (Yes, There's Always One)

Let's address the elephant in the room: this sounds too good to be true. So what's the catch?

1. It's Still in Rollout

Plasma One launched after the mainnet beta went live in September 2025, but it's rolling out in stages. There's currently a waitlist. Early access is prioritizing regions where stablecoin adoption is already strong (like the Middle East, parts of Latin America, Southeast Asia).

If you're in the US or Europe, you might have to wait a bit longer. But the waitlist is open at plasma.to/one.

2. Not FDIC Insured

Plasma One is a financial technology company, not a traditional bank. Your deposits aren't FDIC insured. Instead, your USDT is held on-chain, backed 1:1 by reserves held by Tether.

For context: USDT has a market cap of over $140 billion and has maintained its peg through multiple market crashes, bank runs, and regulatory storms since 2014. But it's not the same as FDIC insurance, and you should understand that distinction.

That said, Plasma has backing from Tether CEO Paolo Ardoino and PayPal co-founder Peter Thiel, plus $24 million in funding from serious institutional investors. This isn't a fly-by-night operation.

3. Yield Isn't Guaranteed

The 10%+ yield comes from DeFi opportunities within the Plasma ecosystem. These yields fluctuate based on market conditions, just like any investment return. During periods of low DeFi activity, yields could drop. During high activity, they could exceed 10%.

However, the yields are generated from actual productive activity (lending, liquidity provision, etc.) in a blockchain optimized for stablecoin efficiency, not from promotional budgets or Ponzi-style recruitment. That makes them more sustainable than "too good to be true" offers from fintech apps that burn VC cash for user growth.

4. Taxes Still Apply

You'll owe taxes on your yield earnings and any XPL tokens you receive as cash back. Plasma One isn't a tax shelter. But the same is true for high-yield savings accounts and credit card rewards - this is just more lucrative.

How It Compares to Traditional Options

Let's be practical and compare Plasma One to the best traditional alternatives available in February 2026:

Even if you combine a top-tier high-yield savings account (5% APY) with the best credit card rewards (2%), you're still not matching what Plasma One offers in a single integrated experience.

The Technology Behind It (Without the Jargon)

You don't need to understand blockchain to use Plasma One (just like you don't need to understand ACH networks to use Venmo). But if you're curious about how this works:

Plasma Is an L1 Blockchain Built for Stablecoins

Most blockchains are general-purpose. Plasma is laser-focused on one thing: making stablecoin transactions as cheap, fast, and efficient as possible. This specialization is why they can offer ultra-low fees (fractions of a cent) and why DeFi yields are competitive without excessive risk.Your Balance Lives On-Chain

When you load USDT into Plasma One, it's held on the Plasma blockchain. This means you have full custody (it's actually yours, not just a database entry at a bank), and you can verify it cryptographically. The app handles all the technical stuff in the background.Yields Come From Real DeFi Activity

Your stablecoins are deployed into lending protocols, liquidity pools, and other DeFi strategies within Plasma's ecosystem. Because the chain is optimized for stablecoins (not volatile assets), these strategies are more efficient and lower-risk than typical DeFi on chains like Ethereum.The Card Bridges Crypto to Traditional Payments

When you swipe your Plasma One card, the payment processor (Signify Holdings via Visa) handles the transaction in traditional payment rails. Behind the scenes, your USDT balance on-chain is decremented. To the merchant, it's a normal Visa transaction. To you, you're spending stablecoins that were earning 10% yield up until the moment you swiped.What This Means for XPL Token Holders

If you hold XPL (Plasma's native token), Plasma One is a major catalyst. Here's why:

Real Utility: Cash back rewards are paid in XPL tokens. Every Plasma One user becomes an XPL holder and has a reason to hold/accumulate it (to maximize rewards).

Transaction Volume: Every card swipe, every transfer, every DeFi interaction generates activity on the Plasma blockchain, which requires XPL for gas fees and staking.

Distribution at Scale: Plasma One puts the blockchain directly into everyday users' hands. This isn't speculative DeFi degens - it's regular people using it for groceries and rent. That's how you get to millions of users.

Network Effects: As more users join Plasma One, more merchants will want to integrate, more DeFi protocols will build on Plasma, and the entire ecosystem compounds in value.

Remember: Plasma raised $24 million from serious investors (Paolo Ardoino, Peter Thiel, Bitfinex, Framework Ventures) and attracted $1 billion in pre-deposits before mainnet. They're not a meme coin. They're building actual infrastructure, and Plasma One is the consumer front-end that makes it accessible.

The Bigger Picture: Banking's Unbundling

Plasma One is part of a larger trend: the complete unbundling of traditional banking.

For the past century, banks have been bundled service providers. They give you checking, savings, loans, credit cards, investments - everything under one roof. And because of that bundling, they've extracted massive value from customers who don't have better alternatives.

But technology is unbundling that model piece by piece:

Venmo/Cash App unbundled peer-to-peer payments

Robinhood/Coinbase unbundled investing

SoFi/LendingClub unbundled loans

Plasma One is unbundling savings + spending + global transfers

Each unbundled service does one thing better than banks ever could because they're not weighed down by legacy infrastructure, regulatory capture, and rent-seeking business models.

Plasma One isn't trying to replace your entire financial life. It's focused on being the best solution for liquid savings and everyday spending. And by being laser-focused on that, they can offer yields 2-5x higher than traditional alternatives.

How to Get Started (When It's Available)

Plasma One is rolling out in phases. Here's how to position yourself:

Join the Waitlist

Head to plasma.to/one and sign up. Early access is being prioritized for regions with high stablecoin adoption (Middle East, parts of Latin America, Southeast Asia), but the waitlist is global.Have Your Documents Ready

Like any financial account, you'll need to verify your identity (KYC). Have your government ID ready. The onboarding process is designed to take minutes, not days.Fund Your Account

Initially, Plasma One supports USDT (Tether), with plans to expand to other stablecoins. You can fund your account via:

Transferring USDT from another wallet/exchange

Using connected on-ramps to buy USDT directly with fiat

Receiving transfers from other Plasma One users

Get Your Card

Upon account creation, you'll receive a virtual card instantly (usable for online purchases). The physical card ships shortly after and works everywhere Visa is accepted.Start Earning Immediately

The moment your USDT hits your Plasma One balance, it starts earning yield. No lockup periods, no minimum balance requirements, no waiting. Spend it whenever you want with your card, and it keeps earning up until the moment you swipe.

Final Thoughts: The Debit Card That Actually Makes Sense

Most "crypto cards" are solutions looking for a problem. They require you to hold volatile assets, charge fees for conversion, and offer mediocre rewards that barely compensate for the risk and complexity.

Plasma One is different. It's not trying to make you a crypto trader. It's rebuilding what a checking account should be: money that's always liquid, always accessible, always earning, and always working for you instead of against you.

10%+ yield. 4% cash back. Zero fees. Global coverage. Instant transfers. All in one app.

That's not too good to be true. That's just what banking looks like when you remove the middlemen, cut the legacy infrastructure costs, and build on technology designed for the 21st century instead of the 19th.

Your bank has been paying you 0.39% and charging you fees for decades because you didn't have better options. Now you do.

The waitlist is open. The technology works. The yields are real. The only question is how long you want to keep leaving money on the table.