Featuring insights from Coinstruct, Cicada MM & Backpack.

In the modern digital assets industry, classic token distribution models are rapidly becoming obsolete. Mechanisms focused on real value and long-term sustainability are replacing the standards of previous years.

Coinstruct founder Maxim Krasnov identifies three fundamental shifts in tokenomics architecture, clearly illustrated by launches from 2024-2026.

High Float vs Artificial Scarcity

One of the clearest departures from the standard playbook in recent launches is the deliberate choice of high initial float: releasing a significant portion of total supply into circulation at TGE instead of drip-feeding it over many years.

This approach counters the dynamics that damaged launches from 2022-2024: low-float tokens with inflated FDV figures looked attractive on day one, then spent the next 18 months in structural decline as VC and team unlocks hit a thin market.

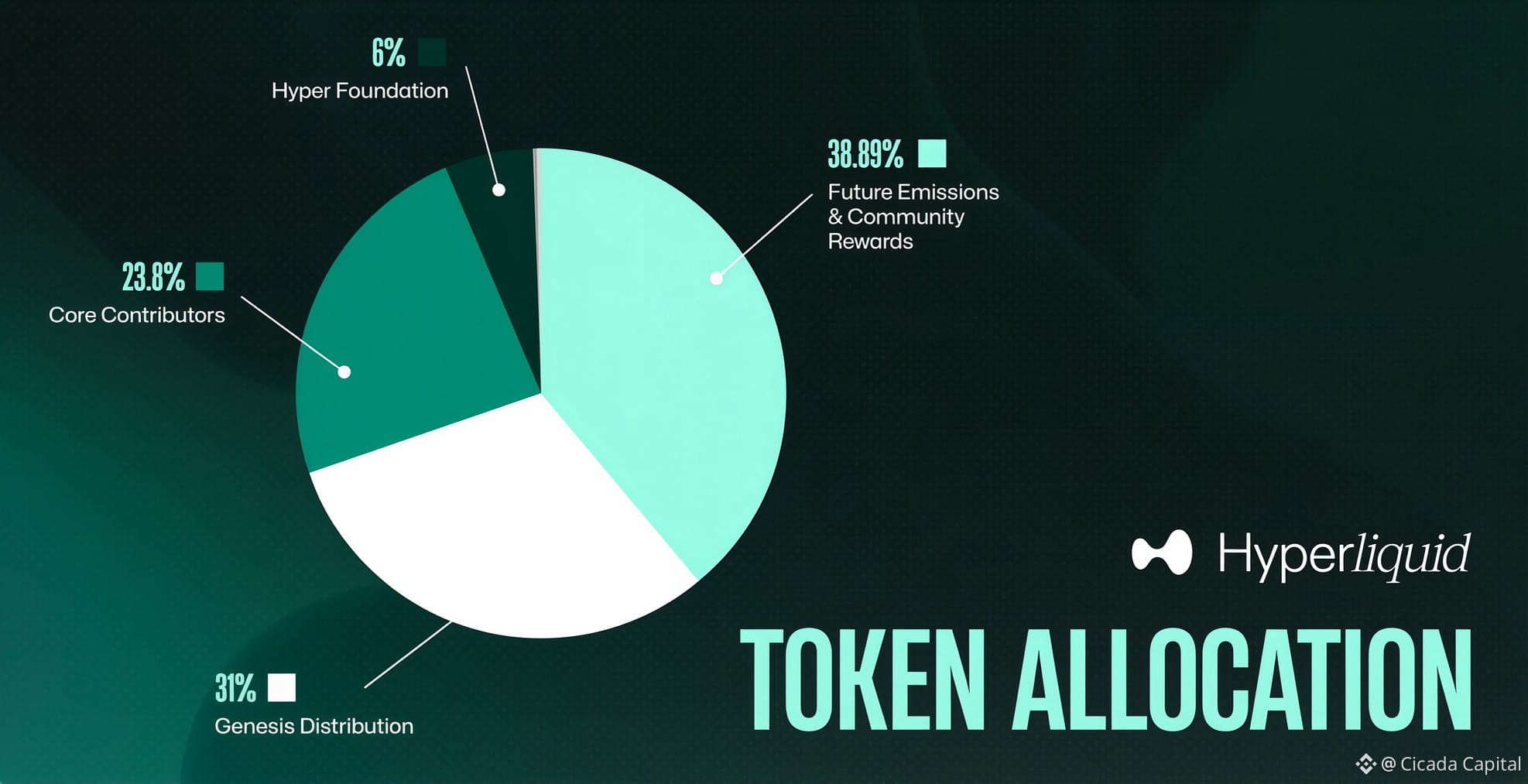

Hyperliquid | $HYPE : The project stands apart from the trend of low-float, VC-backed tokens. With no private entities holding pre-allocated tokens, anyone interested in acquiring HYPE beyond the airdrop must buy directly on the market. This resulted in genuine price discovery from day one, with real buyers against real sellers, rather than an artificial market propped up by restricted supply.Hyperliquid completed its Genesis event in November 2024, distributing 31% of total supply to eligible users: with no allocations for private investors, VC, centralized exchanges, or market makers.

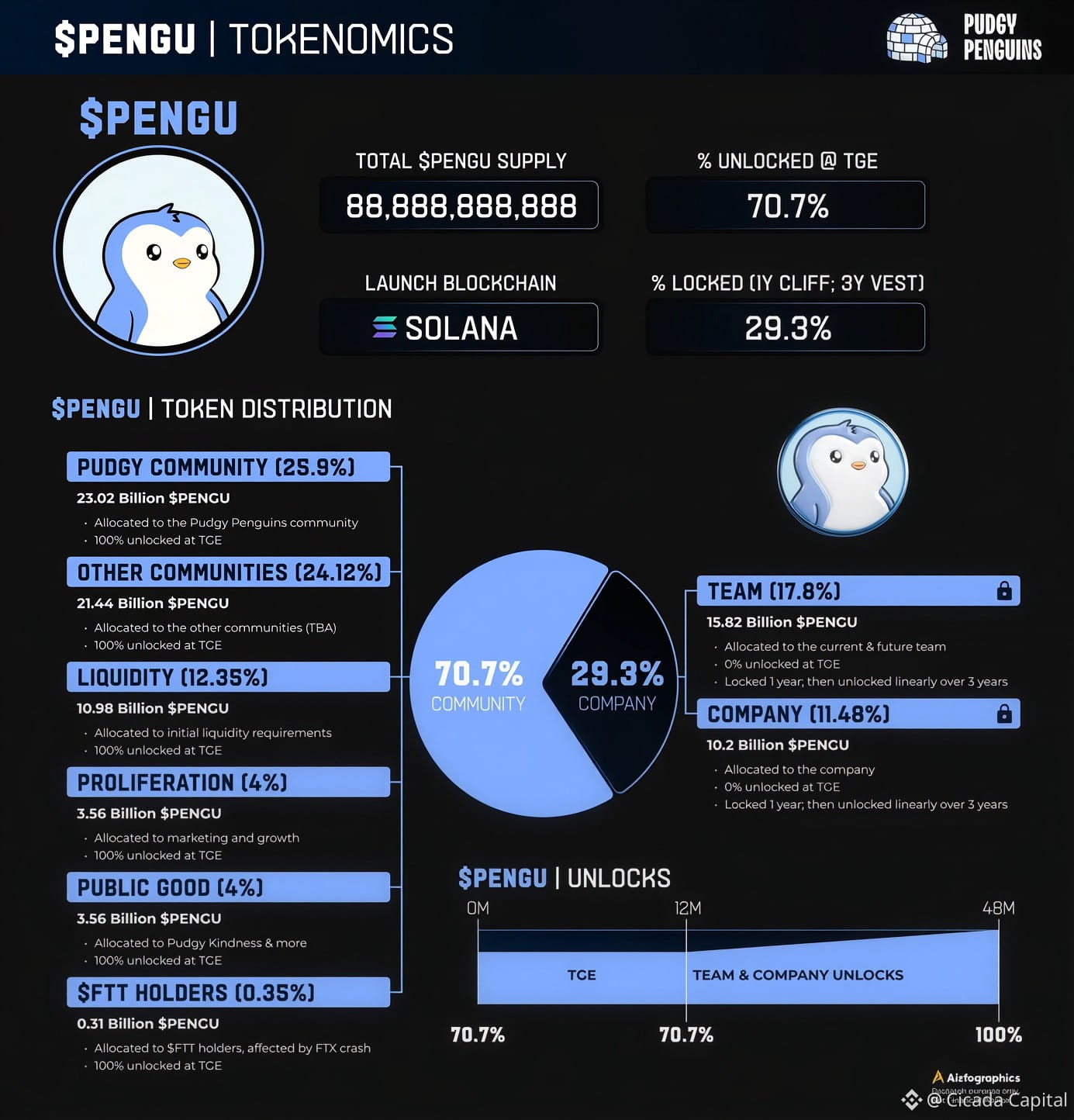

Hyperliquid | Tokenomics Pudgy Penguins | $PENGU : The project applied a similar approach. The entire supply was minted on Solana at TGE, with 25.9% directed to the Pudgy Penguins community and another 24.12% to external communities. In total, approximately half of the supply ended up in community hands at launch.

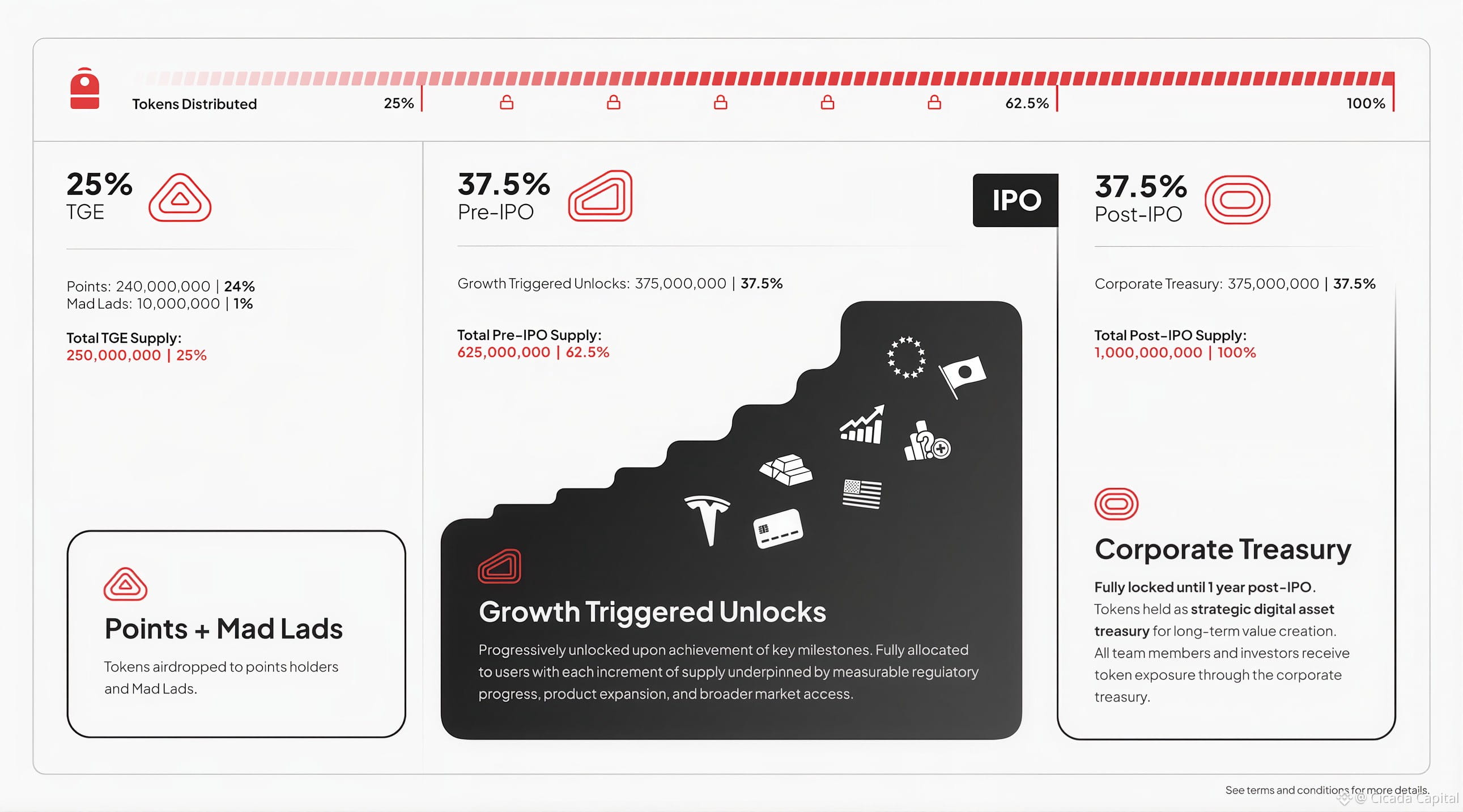

Pudgy Penguins | Tokenomics Backpack | BP: The March 23, 2026 launch pushed this logic furthest of all. The tokenomics were deliberately structured to prevent the pattern of insiders dumping on retail. No founder, executive, team member, or venture investor received a direct token allocation. All TGE tokens went to users: 240 million to points program participants and 10 million to Mad Lads NFT holders. Backpack's initial circulating supply of 25% is significantly higher than typical exchange token launches, which often fall in the 7% to 15% range.

Backpack | Tokenomics

The underlying logic across all three cases is the same: high float compresses the gap between market cap and FDV at launch, eliminates the overhang of known future sell pressure and forces price to reflect actual demand. It signals to the market that the team is not relying on token lockups to manufacture alignment, but on building a product worth holding.

Calendar-Based Vesting Problem

The standard vesting schedule in crypto is time-based - a 12-month cliff followed by linear monthly releases over 24 to 36 months. This structure was borrowed from equity compensation models. The problem is that time-based vesting rewards inertia.

Tokens unlock regardless of whether the project has shipped updates, whether TVL has grown, or whether the team has delivered on its commitments. The schedule runs no matter what.

KPI-Based Unlocks as Alternative

Milestone or KPI-based unlocks change this logic - a portion of total supply is not released until measurable progress is demonstrated.

Backpack is the latest example with clearly documented mechanics. An additional 37.5% of total supply, 375 million pre-IPO tokens, becomes available upon reaching key milestones which, according to CEO Armani Ferrante, include opening in a new region or launching a new product. Token supply expands only as Backpack hits measurable growth milestones, with all new tokens directed to users.

Projects can restrict ecosystem allocations to reaching a target TVL, a user count threshold, or a certain number of active integrations. Infrastructure protocols can tie token releases to verifiable on-chain metrics: transaction volume, uptime, or developer activity. The mechanism is flexible; what it requires from a team is the willingness to define success upfront and be held accountable for it.

An honest limitation here is governance complexity. KPI-based unlocks require clear, manipulation-resistant metrics and a reliable verification process, otherwise they become soft commitments dressed up as hard constraints. Used well, however, milestone-based unlocks turn the vesting schedule from a countdown clock into an accountability mechanism.

Connecting the Token to Capital

The token becomes something more than a governance right or a voting pass. The market has recognized that such mechanics were a promise of decentralization that was never intended to be fulfilled. Projects now understand that a token must represent real value for holders through practical utility within the project or projected cash flows, coming indirectly.

An excellent example is the token-to-equity conversion implemented in the Backpack tokenomics. By locking BP for one year, holders gain the right to a 20% equity stake in Backpack as a company.

Quote from Backpack’s documentation:

Users who stake BP for a minimum of one year can convert their tokens into Backpack company equity at a fixed ratio, representing up to 20% of the company at the time of announcement, shared among all eligible stakers.

It is likely that more projects with sustainable businesses will begin offering such an option to token holders. This is beneficial because token holders would actually get exposure to the underlying business.

Vision from the Backpack Team

We reached out to Alessio Brichese, Global Growth Lead of Backpack, to get an insider’s view on their pioneering model.

As a project that has fundamentally challenged the status quo of exchange tokenomics, their team emphasizes that the shift toward accountability is a conscious choice to protect the ecosystem’s integrity.

Backpack’s vision on alignment and transparency:

Backpack is proud to be among the first in the industry to pursue a path of full alignment: bringing users, team, and investors into the same boat, with equal access to upside if the company succeeds.

Too often, token price has failed to reflect real company performance, leaving token holders unrewarded despite the platform’s growth. Backpack’s equity conversion model changes that: users can own a direct stake in the business and exchanges are among the most profitable businesses in financial markets.

Our tokenomics were designed entirely in-house, without relying on external market makers for token allocation or other arrangements that historically have not served community interests.

We wish the best to all projects launching in this cycle especially those who built through the bear market and have chosen to reward their real supporters: the community. Fair supply distribution and transparent, protective incentives for token holders are the standard we believe this industry should hold itself to.

This commentary underscores a pivotal shift: when a team designs its own incentives rather than outsourcing them to third parties, the resulting structure tends to favor long-term holders over short-term market manipulation.

Maxim Moris's Vision, CEO of Cicada

Maxim Moris, CEO of Cicada Market Making, drawing on hands-on experience with more than 1000 tokens, adds to Krasnov's material with a hard-edged perspective from the market-making side.

Simple tokenomics no longer works:

Two to three years ago it was possible to put together a 10-row spreadsheet: 15% to the team, 20% to investors, the rest to the ecosystem and it passed. The market was different, investors were less informed, competition for listings was lower.

That no longer works. Exchanges and VCs scrutinize tokenomics. Retail does too, through the question: will there be a dump after TGE? 89% of tokens decline after a CEX listing. These are statistics we collect every day.

Tokenomics without a business model is a scheme:

It is frustrating when projects arrive with beautiful tokenomics where everything is balanced, but when asked how the project makes money, there is silence. Or when asked: why do you need a token? Silence again.

The market in 2025 to 2026 has raised the bar. Only those who clearly explain their business model and the organic role of their token can raise capital.

The $BNB case: a direct link between business and token:

The best example is BNB. Binance built in the mechanism from the start: each quarter, a percentage of exchange revenue is used to buy back and burn tokens. The business pays for its token with real money. The better the exchange performs, the greater the pressure on supply reduction.

This is not APY from thin air, it is real cash flow converted into value through deflation. If this cannot be explained in two sentences, the tokenomics are not ready.

Standard vesting is a conflict of interest:

The model of a 6-month cliff with 18 to 24 months of linear vesting came from traditional venture capital, where there was no public market in the early years. In crypto, the token trades from day one. The team and investors know the unlock date and so does the market.

Selling pressure begins in advance. This is a structural dump programmed into the document. A built-in adversary is created within the tokenomics itself. Offering standard timelines without KPI conditions today means fewer chances of success.

Public rounds as a proof of concept:

Before VCs commit capital, a project must prove its viability and demand within the industry. This should happen through a public round without a refund policy. For example, raising $100k on a launchpad.

This serves as a validation for funds that the community trusts the founders and is willing to invest their own money. It is crucial that such a round takes place on a platform without a refund mechanism, ensuring genuine commitment rather than speculative participation.

A combined model is needed:

Sound tokenomics today is a hybrid: part time-based unlock, part KPI-based. For the team the logic is straightforward: want tokens, hit the KPIs. The bonus is paid for results, not simply for staying. The team should not hold an unlimited number of tokens available for exit without confirmed progress.

For investors the logic is different. They took on risk at an early stage and deserve the opportunity to exit at a profit as price rises. A portion of tokens can unlock at price triggers. Price rises by X%, the next tranche opens. This is a fair deal: the investor took the risk, the market grew, the investor earned.

Summary, investors, exchanges, and communities have become smarter. 2021-era tokenomics in 2026 is a red flag. Projects must design tokenomics as part of the business, not as a marketing document for raising money.

While most do not understand this yet, the same mistakes keep appearing. The 89% of tokens down after listing is the result of incorrectly designed incentives.

Conclusion

The three elements described above form a transition from an economy of hope to an economy of accountability. Teams consciously place themselves in conditions where project success is inseparably linked to their own benefit, rather than being guaranteed by time. High float and KPIs signal a bet on product quality rather than technical tricks.

Such tokenomics becomes a filter that screens out projects oriented toward a quick exit at the expense of retail investors. Long-term sustainability is valued over temporary pumps. The token becomes a sophisticated financial asset with technological utility or hard economic backing comparable to traditional business equity.