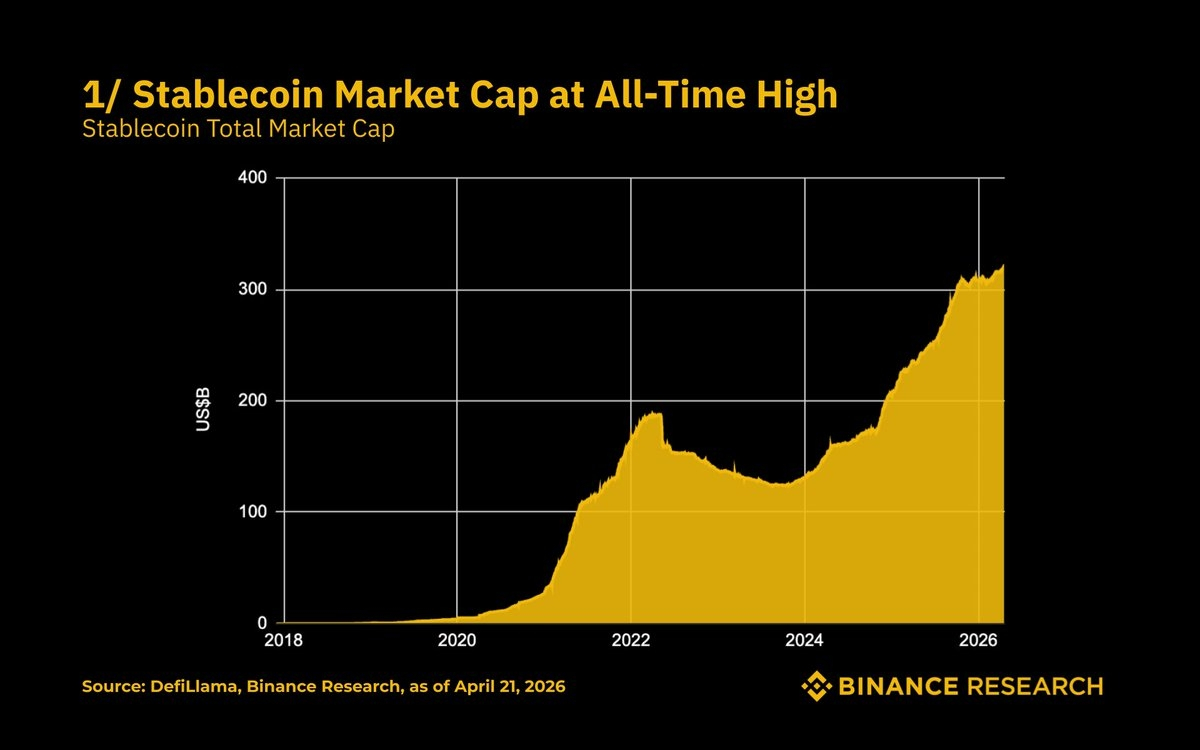

The slope is the signal, not the headline number.

Under $5B in 2020, roughly $185B at the 2022 peak, ~$320B now. The part I keep staring at is that the trend hasn't broken since early 2024. No dramatic V-recovery, just a steady grind higher through drawdowns, rate cycles, and sentiment chop. Supply used to be procyclical, pumping with leverage and contracting when the casino shut down. It's now behaving like actual money. That decoupling from speculation is the most bullish macro setup for crypto infrastructure I've seen in years, and I don't think it's priced in anywhere on the chart.

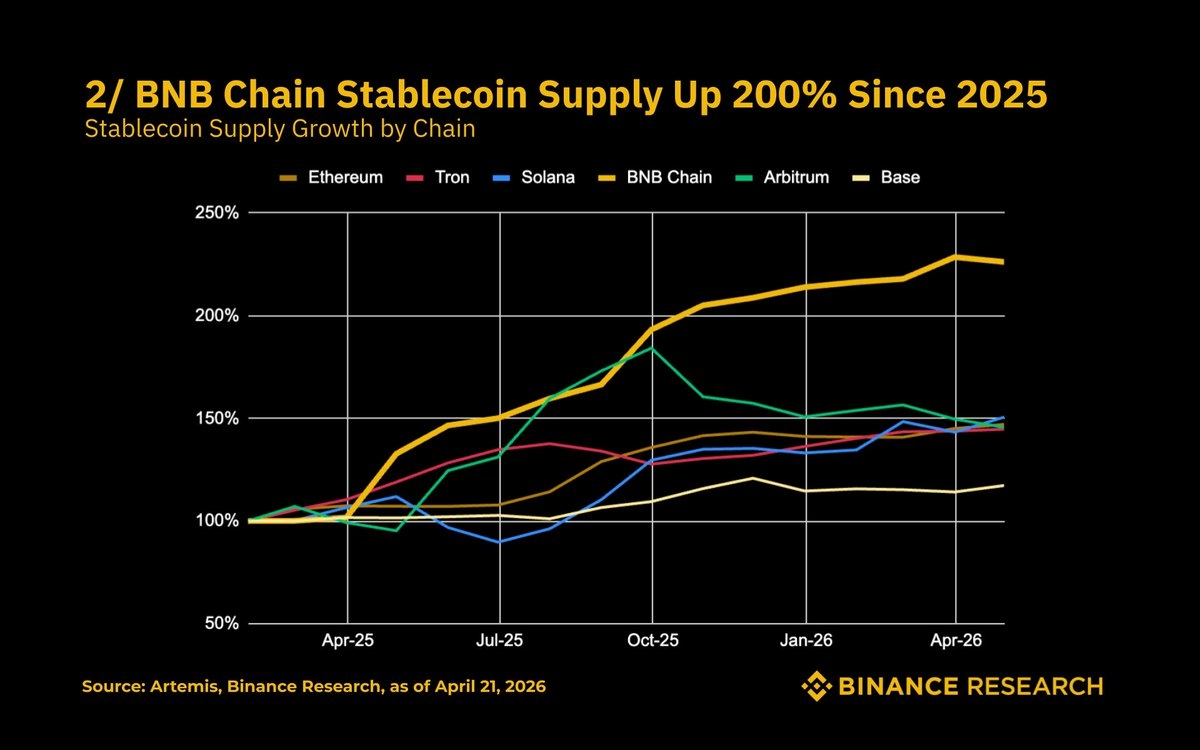

2. BNB Chain is quietly running away with supply growth.

Up over 200% since early 2025, the steepest curve among the majors by a clear margin. Ethereum, Tron, and Solana are clustered together at 140 to 150%. Base is the laggard at 115%. And this isn't a small-base flattery effect. BNB Chain entered 2025 already sitting near the top of the nominal supply rankings. Adding another 200% on top of that baseline is real liquidity migration, not a statistical artifact. Worth asking where that flow is coming from and why now.

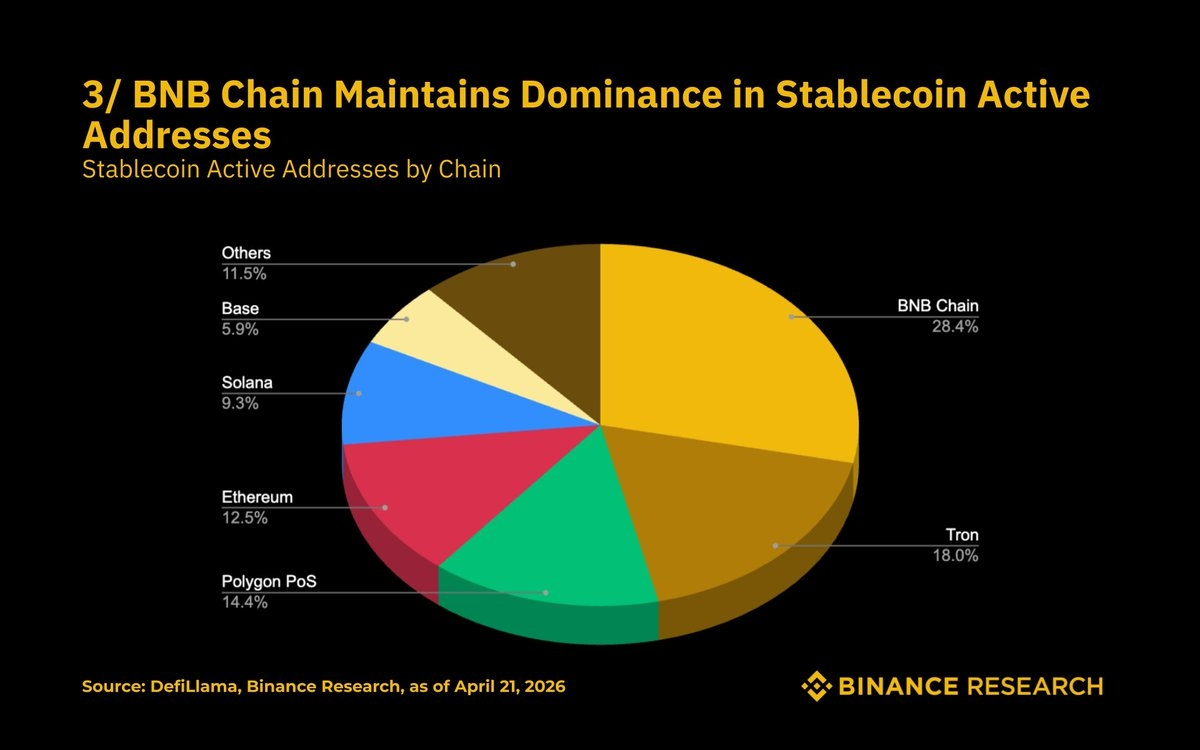

3. Active addresses confirm it, and that's the part that matters.

BNB Chain holds 28.4% of stablecoin active addresses. Tron 18%, Polygon 14.4%, Ethereum 12.5%, Solana 9.3%, Base 5.9%. Supply can be gamed by a handful of whales. Address counts can't, or at least not cheaply. The chain with the most users actually moving digital dollars right now isn't Ethereum and isn't Solana. The gap to the next competitor is ten full percentage points. Crypto discourse hasn't caught up to this yet, and when the narrative eventually closes on the data, the repricing tends to happen in a compressed window.

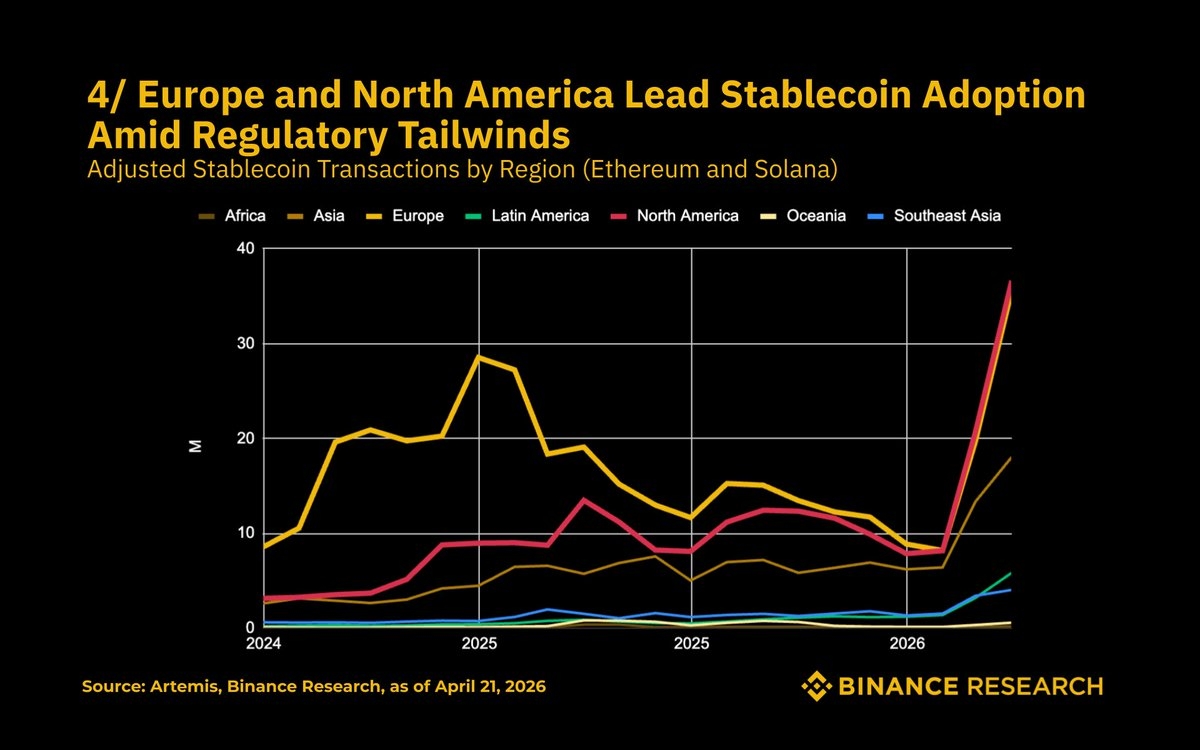

4. Geography is flipping in a way that deserves attention.

North American adjusted volume on Ethereum and Solana went near vertical in 2026, now running level with Europe after being well behind for years. What this tells me is there are basically two parallel stablecoin markets running at the same time. Emerging-market, retail-heavy, small-ticket flow on BNB Chain, Tron, and Polygon. North American, institutional, large-ticket settlement flow on Ethereum and Solana. Both are compounding, both are eating dollar volume from legacy rails, and they need completely different investment frameworks.

North American adjusted volume on Ethereum and Solana went near vertical in 2026, now running level with Europe after being well behind for years. What this tells me is there are basically two parallel stablecoin markets running at the same time. Emerging-market, retail-heavy, small-ticket flow on BNB Chain, Tron, and Polygon. North American, institutional, large-ticket settlement flow on Ethereum and Solana. Both are compounding, both are eating dollar volume from legacy rails, and they need completely different investment frameworks.

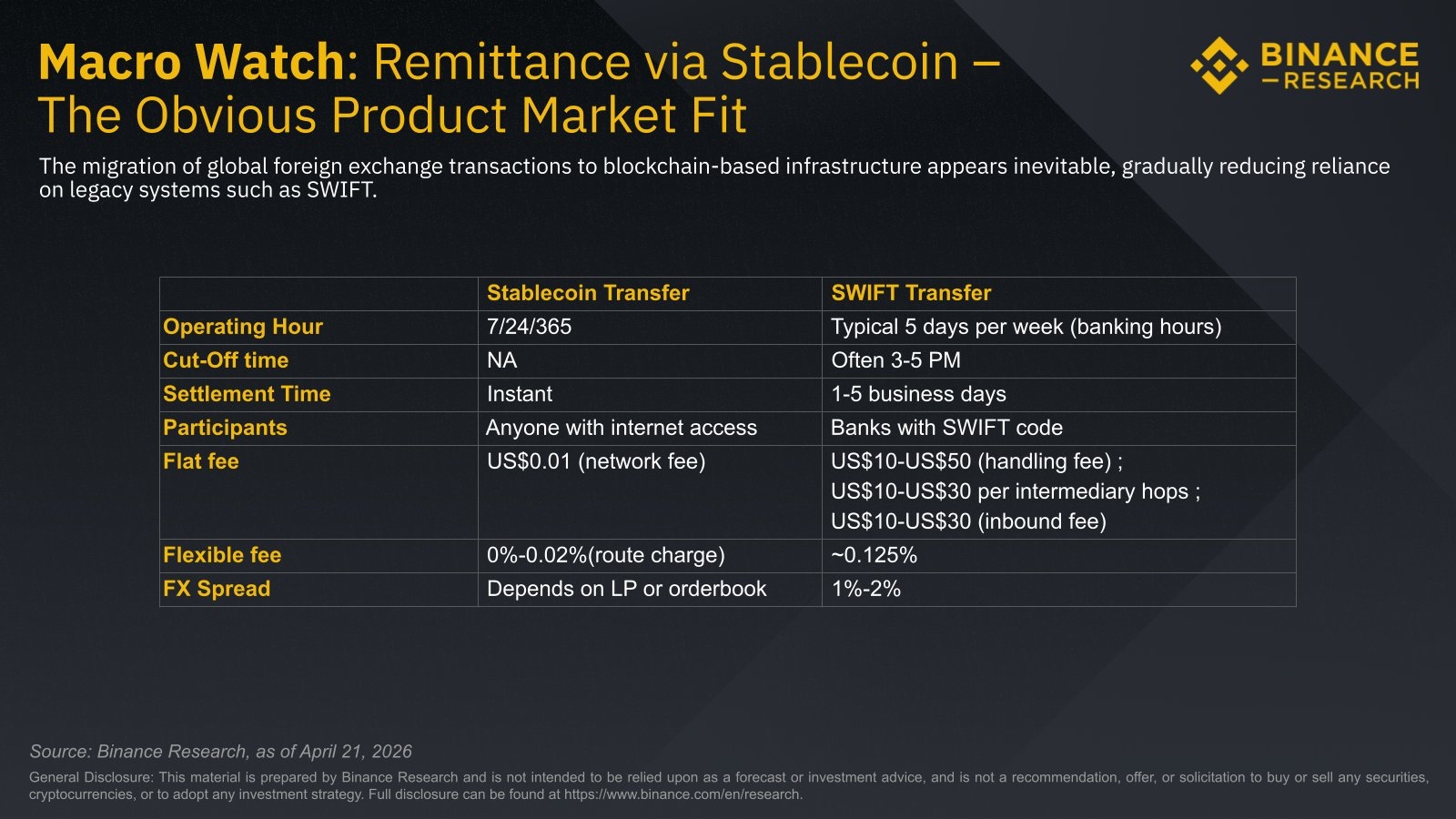

5. Remittance is the PMF nobody wants to admit is the main event.

Global remittance sits north of $800B a year with average fees still running 6 to 7%. Stablecoins do the same job for basis points of cost. That's not incremental improvement, that's a generational cost collapse on the sending side. And the split in the on-chain data makes total sense once you see remittance as the dominant retail use case underneath it all. Users go where fees are low and rails are familiar. Institutions go where liquidity is deep and compliance is clean. Everything else is flavor on top.

Final Opinion....

$320B sounds big until you remember US M2 alone is north of $22 trillion. We're still in the early innings here and the chart doesn't look like it wants to break down.