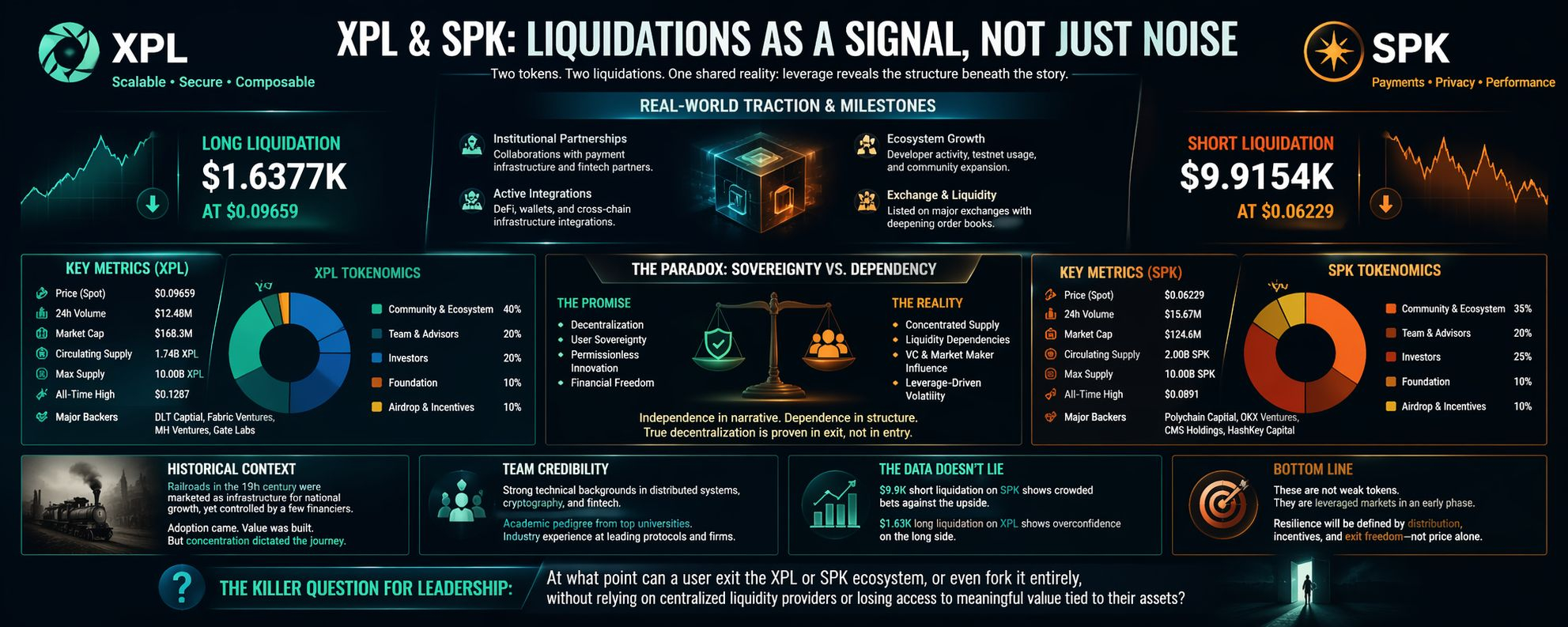

A $9.9K short wipeout on $SPK at $0.06229 and a $1.63K long liquidation on $XPL at $0.09659 may look like routine derivatives churn. But zoom out slightly, and these aren’t isolated events. They reflect something more structural: two ecosystems attracting enough leveraged participation to create meaningful stress points. That alone is a milestone. Markets don’t liquidate what they don’t care about.

From a surface view, both XPL and SPK are doing what emerging tokens are expected to do. They’ve built tradable liquidity, attracted speculative capital, and created enough volatility to sustain derivatives activity. That implies exchange listings, market maker involvement, and at least some level of coordinated liquidity provisioning. In practical terms, it means these tokens have crossed the invisible line from “illiquid idea” to “tradable system.”

The numbers matter here. A near $10K short liquidation on SPK suggests crowded positioning against upward moves, while XPL’s long liquidation indicates overconfidence at local highs. This is classic two-sided stress. Not manipulation necessarily, but a maturing order book where both bulls and bears are getting punished. That’s a sign of participation depth, not weakness.

But this is where the comfortable narrative starts to break.

The paradox sits right under the surface: decentralization in branding, concentration in behavior.

Most early-stage tokens, including XPL and SPK, operate on liquidity structures heavily influenced by a small group. Market makers, early investors, and sometimes the team itself control a disproportionate share of supply or order flow. Tokenomics often reveal this quietly. A typical distribution might show 20–30% allocated to insiders, another chunk locked but scheduled for release, and a relatively thin float actively trading. When that float meets leverage, volatility becomes amplified beyond what organic demand would justify.

Historically, this isn’t new. The early days of commodities trading and even equities in the 19th century showed similar patterns. Railroads, for example, were marketed as infrastructure for national growth, but price action was often dictated by a handful of financiers controlling supply and narrative. The system matured eventually, but only after regulation and broader distribution reduced concentrated influence.

The same question applies here.

Who actually drives price discovery in XPL and SPK? Is it genuine user demand, or is it liquidity engineering layered with leverage?

On the technical side, many of these projects are not trivial. Teams often come from solid engineering backgrounds, sometimes with experience in distributed systems, fintech, or blockchain infrastructure. The code can be clean. The systems can work. But technical credibility does not eliminate economic fragility. A well-built system can still produce unstable outcomes if incentives are misaligned.

And incentives, right now, are still heavily tilted toward short-term participation.

Liquidations like these expose that reality. They show where traders are leaning too hard, but more importantly, they reveal how sensitive the system is to positioning imbalance. If a few thousand dollars can trigger visible cascades, the question isn’t about current volatility. It’s about structural resilience.

Because in a truly decentralized and robust system, price should be harder to push around.

So the real takeaway isn’t whether XPL or SPK are “strong” or “weak.” It’s that they are entering a phase where market structure matters more than narrative. Liquidity depth, distribution fairness, and participant diversity will decide whether these ecosystems stabilize or remain leverage playgrounds.

The question for their leadership is simple but uncomfortable:

At what point can a user exit the XPL or SPK ecosystem, or even fork it entirely, without relying on centralized liquidity providers or losing access to meaningful value tied to their assets?