2026 Regulatory Compliance Report/Digital Asset Standards for UK & EU Entities

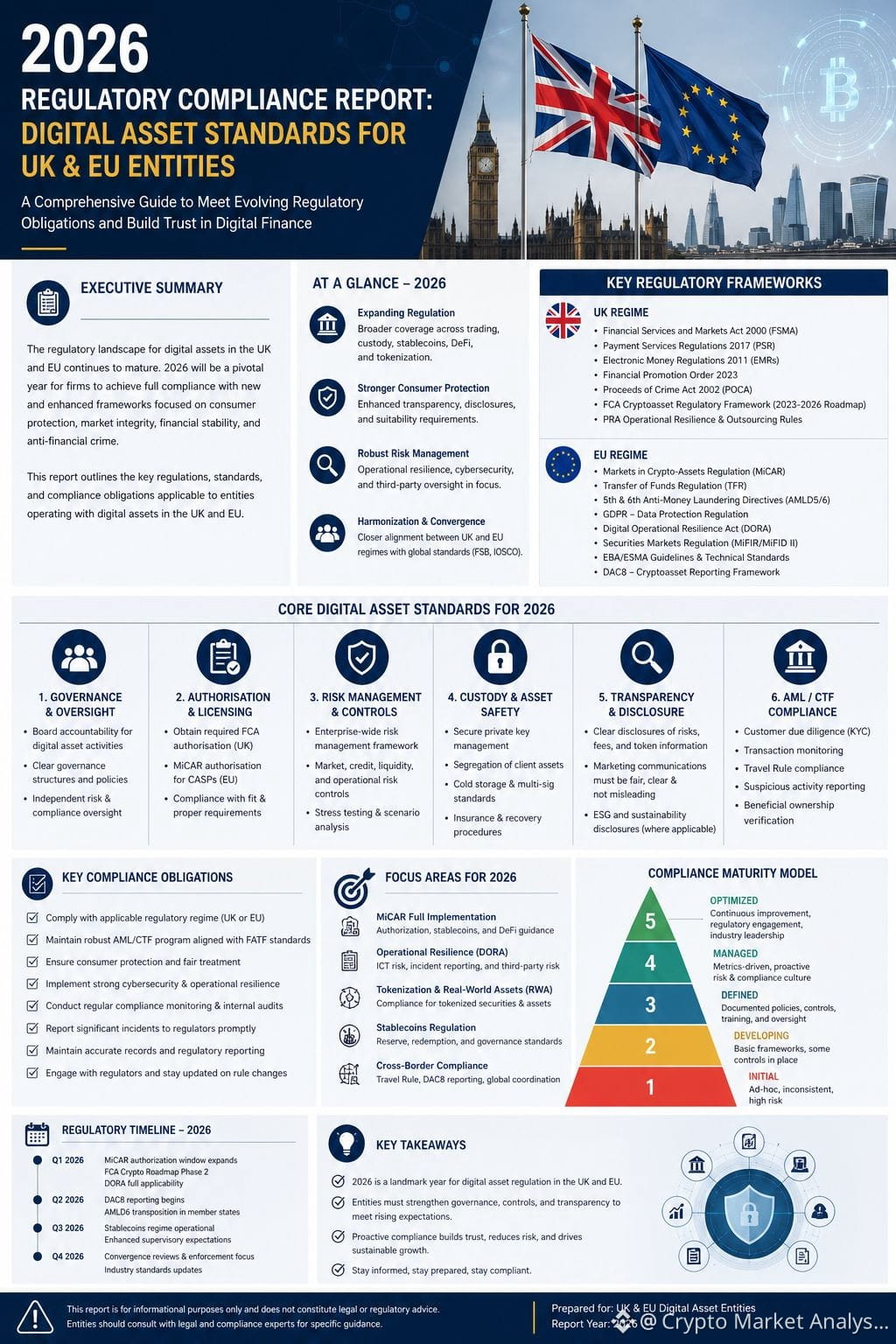

1. The Transformed Regulatory Landscape: MiCA Harmonization

As of 2026, the European digital asset sector has officially crossed the "Regulatory Rubicon." We have transitioned from a phase of speculative policy drafting into an era of aggressive enforcement across the European Economic Area (EEA). This shift represents a critical stage in market maturity; for institutional stakeholders, compliance is no longer a peripheral cost center but a primary driver of operational viability and market access. The fragmentation of the past has been replaced by a standardized financial environment that demands bank-grade transparency.

The Markets in Crypto-Assets (MiCA) regulation serves as the bedrock of this new landscape. By harmonizing rules across all 27 EU member states, MiCA has effectively eliminated the "Wild West" era of digital assets. This unified framework ensures that only authorized service providers can operate, providing the legal certainty necessary for global firms to scale while protecting the stability of the broader financial ecosystem.

Key Regulatory Pillars (2026)

Framework

Primary Compliance Mandate

MiCA (Markets in Crypto-Assets)

Establishes harmonized licensing and mandatory authorization for crypto-asset service providers (CASPs) across the EEA.

TFR (Transfer of Funds Regulation)

Enforces the "Travel Rule," requiring the removal of anonymity through comprehensive transaction monitoring.

DAC8 (Fiscal Transparency)

Mandates the collection of Tax Identification Numbers (TINs) and automated reporting to national tax authorities.

This transition toward EU-wide harmonization serves as the necessary precursor for the granular, zero-threshold tracking of every asset moving through the digital financial system.

2. The 'Zero Threshold' Policy and Transfer of Funds Regulation (TFR)

In the current landscape, the "Travel Rule" has become the cornerstone of Anti-Money Laundering (AML) efforts. Its strategic importance to the integrity of the crypto-financial system is absolute; by ensuring that digital assets are no longer anonymous, regulators have effectively integrated crypto-assets into the global financial oversight structure. The Transfer of Funds Regulation (TFR) is the mandatory mechanism for this transparency.

A critical component of this framework is the "Zero Threshold" policy. Under this mandate, traditional exemptions for small-value transfers have been abolished. Crypto-asset service providers must now collect, verify, and transmit detailed data on both the originator and the beneficiary for every transaction, regardless of size. This ensures that the chain of custody for digital value is as auditable as a traditional SWIFT transfer.

To avoid regulatory friction and potential seizure of funds, entities must maintain bank-grade accuracy for the following mandatory data points:

Originator Information: Full legal name, verified account details, and address or official personal document number.

Beneficiary Information: Full legal name and destination account/wallet address.

Transaction Context: Verified data identifying the nature and purpose of the transfer to justify the movement of capital.

The rigor required for transaction-level data sets a high standard for institutional transparency, which extends directly into the disclosure requirements for national tax authorities.

3. HMRC Tax Disclosure Rules and UK Compliance Mandates

The UK’s regulatory environment in 2026 is defined by a sophisticated transparency layer. As Jonathan Athow, HMRC’s General Director for Customer Strategy, has emphasized, these rules do not represent a "new tax." Instead, they function as a disclosure mechanism designed to fund public services—generating an estimated £315 million in revenue—through improved compliance. This framework allows HMRC to assist individuals in properly managing their tax affairs while identifying non-disclosure.

Starting in January 2026, mandatory disclosure requirements apply to all UK-based cryptocurrency holders. Service providers are now legally obligated to collect and report a user’s Tax Identification Number (TIN). This enables HMRC to cross-reference trading activity with individual tax filings automatically.

UK authorities have established severe repercussions for non-disclosure or incomplete reporting:

Financial Fines: Standard penalties for incomplete or inflated reports typically start at £300.

Criminal Liability: Severe cases of intentional non-disclosure or fraudulent reporting can result in larger financial penalties and imprisonment.

This level of personal fiscal transparency mirrors the rigorous corporate verification standards required to access institutional liquidity and high-volume payment rails.

4. Bank-Grade Merchant Verification: The KYB Architecture

The transition from standard Know Your Customer (KYC) to high-level Know Your Business (KYB) is the critical "defensive mechanism" for fintech gateways in 2026. For enterprises, this is a strategic pivot; integrating with regulated gateways like INXY can reduce processing fees by up to 70% compared to traditional card networks, but this cost efficiency is only accessible to verified entities.

Architecture of the KYB Process

The 2026 KYB workflow is designed to achieve three primary objectives:

Legal Existence: Verification that the entity is a real, legally registered business via registry extracts that must be no older than 3 months.

Control Disclosure: Unmasking the ownership structure to identify those who exercise actual power over the entity.

Risk Scoring: A comprehensive evaluation of the merchant’s industry, geographic location, and expected transaction profile.

A central pillar is the "25% Rule" for identifying Ultimate Beneficial Owners (UBOs). To prevent the use of shell companies, firms must trace ownership chains back to the natural persons who hold more than 25% of the shares or voting rights. Verification requires full legal names, dates of birth, and contact details for every individual meeting this threshold.

Mandatory Documentation for Merchant Approval

To secure a verified merchant account, the following must be provided:

[ ] Certificate of Incorporation: Official proof of registration from a government registry.

[ ] Articles of Association (AoA): Defining the entity’s leadership and operational structure.

[ ] Operating License: Required for regulated sectors (e.g., gaming, forex, fintech).

[ ] Registry Extracts: Current proof of status (must be issued within the last 3 months).

[ ] Notarized English Translations: Mandatory for any documents originally issued in a non-English language.

While documentation establishes identity, data governance ensures that the entity remains operationally resilient over the long term.

5. Operational Resilience: GDPR and DORA Alignment

In 2026, data protection is a strategic imperative. Compliance is now tethered to a dual-layer of protection: privacy (GDPR) and technical resilience (DORA). The Digital Operational Resilience Act (DORA) mandates that payment gateways demonstrate immunity to cyber threats. For the CCO, DORA compliance is about avoiding the massive "operational downtime" fines that can be triggered under MiCA enforcement.

Strategic gateways now utilize "Invisible Crypto" UX practices. By handling real-time conversion into stablecoins or EUR behind the scenes, gateways mitigate volatility risk and ensure liquidity while maintaining the technical resilience of the transaction. Furthermore, the "Purpose Limitation" principle under GDPR is strictly applied to KYB data; sensitive UBO information must be used exclusively for identification and activity justification, preventing unauthorized data exposure.

These layers of protection transform compliance from a hurdle into a profound competitive advantage for verified, operationally sound entities.

6. Assessment of FCA-Registered Entities and Market Access

For UK-based entities, market access is governed by the Financial Conduct Authority (FCA). It is essential to distinguish between FCA registration for AML purposes and full authorization. Critical Risk Note: FCA registration indicates AML supervision but does not guarantee Financial Services Compensation Scheme (FSCS) protection. Verification on the Financial Services Register remains a mandatory first step.

Top-Tier FCA-Registered Exchanges

The following entities have established the strongest regulatory footprints:

eToro (UK) Ltd: Fully registered with integrated e-money services for seamless fiat-to-crypto movement.

Coinbase: Secured VASP (Virtual Asset Service Provider) registration in February 2025, strengthening its UK compliance.

Kraken: Holds crypto-firm registration alongside FCA e-money approval for professional-grade liquidity.

Gemini: Listed on the FCA's crypto-asset register with a specific focus on institutional-grade custody.

Criteria for Selecting a Compliant Exchange

Liquidity: Deep order books to minimize slippage during large enterprise-level transactions.

Security Infrastructure: Mandatory 2FA, cold storage, and independent audits of reserves.

Local GBP Rails: Support for Faster Payments and SEPA to ensure the 70% fee reduction is realized through local settlement.

Conclusion

The 2026 landscape is one of clarity and accountability. While the compliance burden has increased, the resulting operational resilience is a powerful market differentiator. Obtaining a verified, bank-grade account is no longer just a requirement—it is the essential key to unlocking global markets and ensuring long-term viability in the digital economy.