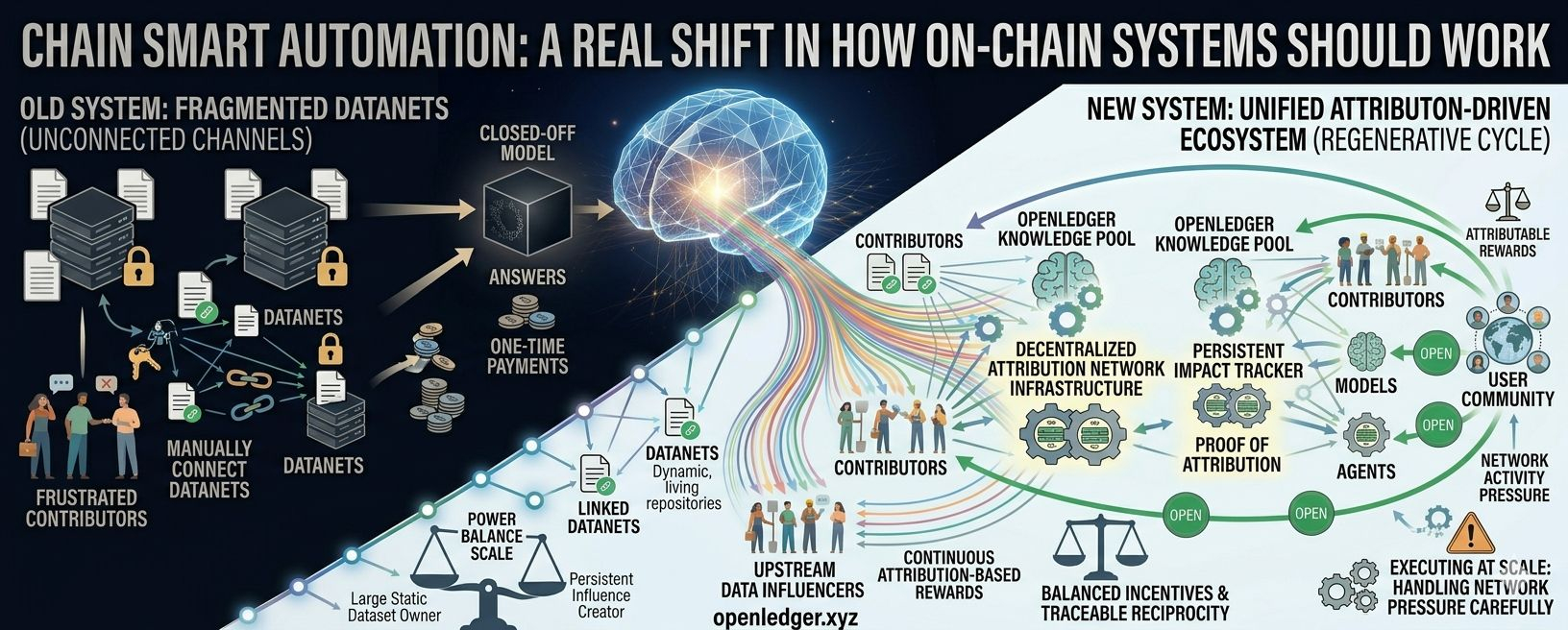

After spending a fair amount of time testing on-chain automation and AI-based trading tools, I have started to look at the whole space differently. Most products look impressive at first glance, but when you actually use them, they usually force you to choose between two bad options: either you give up too much control for the sake of convenience, or you keep control but end up with a system that is too complex for normal users. I have personally felt both sides of that problem, and that is why Chapter 10 of the @OpenLedger whitepaper stood out to me. Instead of staying at the level of abstract concepts, this chapter gets into something much more practical: how smart execution can actually work on-chain in a way that feels usable, secure, and scalable.

What interests me most is that this chapter is not just talking about features in isolation. The Octoclaw distributed execution system, the on-chain trading agent, the EVM cross-chain bridge, and the ERC-4626 asset layer are all connected into one structure. That matters, because a lot of people still judge automation tools as if they were only trading utilities. I think that misses the bigger picture. The real issue in on-chain automation is not simply whether a tool can place trades faster. The real question is whether users can keep ownership, maintain transparency, and still run strategies without depending on a centralized middle layer. In the current market, most automation setups still rely on custody-heavy models. Users hand over access, trading logic runs on off-chain servers, and the user often has very little visibility once the process starts. That is exactly the kind of setup that makes people nervous, especially after seeing how hard it can be to trace problems when something goes wrong.

From that angle, Octoclaw feels much more serious than the usual tooling. Its design makes a clear distinction between ownership and execution. Users remain in control of their keys and assets, while distributed nodes focus on watching the market, carrying out strategies, and catching risk signals. The important part is that execution is not hidden in the background. Every major step is recorded on-chain, which means the process is visible instead of being locked inside a private server. To me, that is the real strength of the architecture. It is not just about reducing manual work. It is about building a system where automation does not require trust to be sacrificed.

Still, I do not think it would be honest to describe the model as perfect. The same distributed structure that gives it strength also creates pressure. Since many nodes need to stay synchronized with live on-chain data, the system generates a lot of interaction overhead. That may not sound serious at first, but once the user base grows and strategies begin firing more frequently, delays in synchronization or congestion in instruction queues could become a real issue. In high-speed trading, even a small delay can change the outcome. So while the architecture is promising, it will need continued optimization if it wants to handle heavier real-world usage.

The trading agent side of the system is another point where the chapter goes beyond surface-level automation. A lot of people hear “agent” and immediately think of copy trading or simple quant replication. That is too narrow. The stronger idea here is modular design. Instead of forcing users into a fixed strategy template, the platform breaks the process into separate parts like market filtering, position management, take-profit and stop-loss logic, and cross-chain balancing. That gives regular users more flexibility without requiring them to write code from scratch. For many people in the crypto space who want to build steady compounding strategies but do not have technical skills, that kind of structure is genuinely useful. At the same time, modular freedom is not automatically safe. If users combine pieces without understanding how they interact, they can easily create contradictory logic or unstable execution behavior. So the system lowers the barrier to entry, but it does not remove the need for judgment.

I also spent time thinking through the ERC-4626 integration together with the cross-chain bridge design. This is where the chapter starts to feel less like a trading product and more like a full asset-management layer. It allows assets to move across chains, compound automatically, and rebalance in a more intelligent way, with $OPEN serving as part of the settlement process across use cases. That saves users from repeating manual cross-chain transfers and repetitive compounding steps, which is a real improvement in everyday asset management. But cross-chain systems always come with structural risk. Different chains confirm blocks at different speeds, and contract environments are not always perfectly aligned. Under stressful market conditions, delays can still happen, and liquidation logic can lag behind. That is not a flaw unique to OpenLedger; it is simply one of the realities of cross-chain infrastructure.

Overall, what I take from Chapter 10 is that OpenLedger is trying to solve the actual pain points in on-chain automation instead of just wrapping old ideas in a new narrative. The focus is clearly on the balance between control, safety, and usability. Yes, there are still real challenges: concurrency limits, onboarding friction, and cross-chain risk will all need more work. But the direction feels meaningful. Compared with many projects that mostly rely on hype, this chapter feels like an attempt to build the kind of infrastructure the market actually needs.