The US Bureau of Labor Statistics is set to release the May 2026 CPI data today (June 10) at 8:30 AM ET, with forecasts indicating a headline inflation rate of 4.2% year-over-year, up from 3.8% in April.

The monthly increase is expected at +0.5%, slightly down from April’s +0.6%. This rise is attributed to three months of energy-driven price increases, bringing prices to a three-year high.

CPI DAY IS HERE. 6 PM IST. • Forecast: 4.2% • Previous: 3.8% This would be the highest US inflation print in over 3 years. Oil prices remain elevated following the Iran-related energy shock, and markets are starting to whisper two words again: RATE HIKES Tonight… pic.twitter.com/aRHVM1kw2V

— Wise Advice (@wiseadvicesumit) June 10, 2026

Core CPI, which excludes food and energy, is projected to be +0.3% month-over-month and 2.9% year-over-year, exceeding the Fed’s 2% target. As a result, there is about a 70% chance of a 25-basis-point rate hike by year-end, with a 38% likelihood of a move as soon as September.

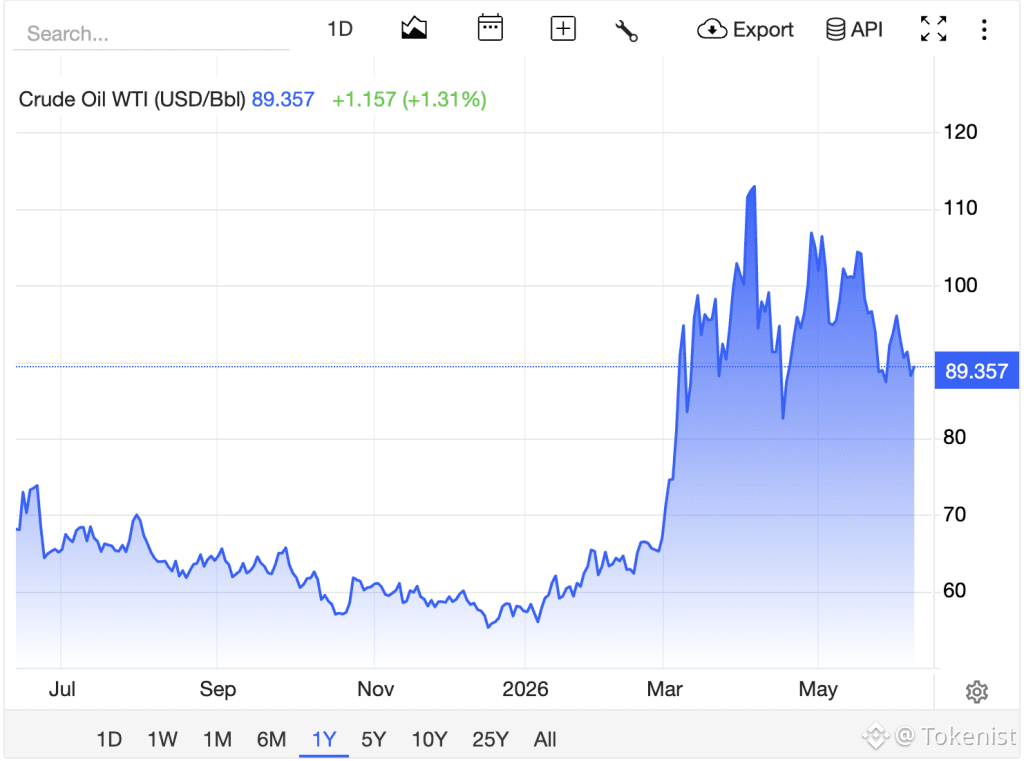

The headline CPI increase is largely due to a more than 50% rise in crude oil prices since the start of the Middle East conflict on February 28, 2026, further intensified by renewed hostilities on June 7.

The Oil-to-CPI Transmission Channel: How a 50% Crude Surge Pushes Headline Inflation to a 3-Year High

The world's largest oil tankers are being ordered at a record pace: There are currently 262 supertankers on order at shipyards worldwide, the highest number on record. This marks an over +1,000% surge from the levels seen just 2 years ago. Each of these vessels can carry up to… pic.twitter.com/wNXkXEQsOb

— The Kobeissi Letter (@KobeissiLetter) June 10, 2026

West Texas Intermediate crude prices have surged over 50% since the Middle East conflict began on February 28, raising concerns about supply disruptions through the Strait of Hormuz.

In April, energy prices jumped 3.8% month-over-month, contributing to over 40% of the overall CPI increase.

This trend continued into the May 2026 CPI report, where headline inflation at 4.2% was largely driven by energy costs, mirroring the situation in May 2023 during oil price escalations due to geopolitical tensions.

In contrast, core CPI, which rose 2.9% year-over-year, indicates more stable underlying price pressures, with the three-month annualized rate closer to 2%–2.5%.

However, if core readings exceed the expected monthly increase, particularly in shelter or airfares, it could complicate the Fed’s response to overall inflation.

Higher for Longer Calcified: What a 4.2% CPI Print Does to Federal Reserve Rate-Cut Expectations in 2026

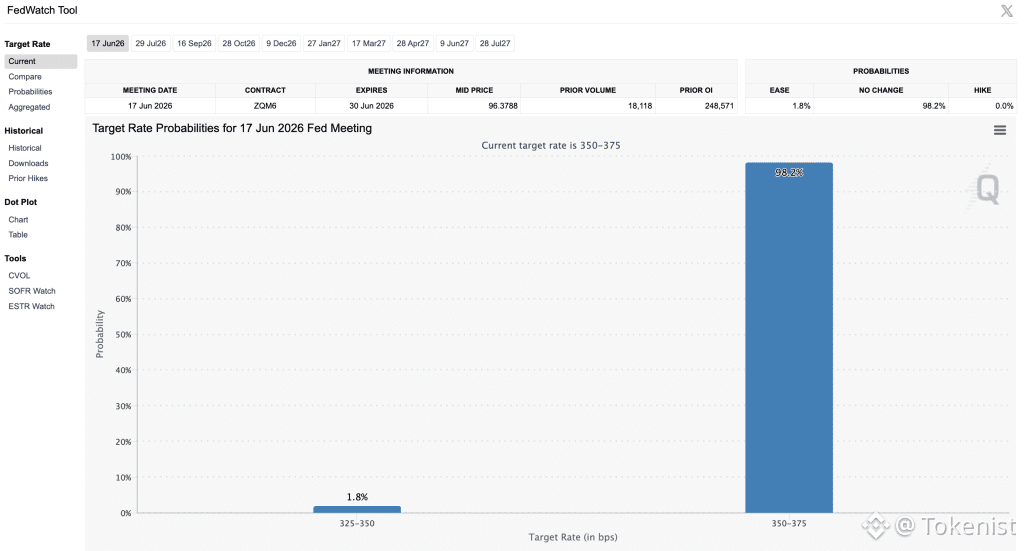

SOURCE: CMEGroup.com

SOURCE: CMEGroup.com

The Federal Reserve is currently leaning toward a more hawkish stance, with the CME FedWatch Tool indicating a 70% probability of at least one rate hike by year-end.

Markets have shifted away from a 2026 rate-cut narrative, with potential cuts pushed into late 2027 if inflation stays above 4%.

A May 2026 CPI reading at or above 4.2% confirms this trend, especially with strong labor market data, including May Nonfarm Payrolls rising by 172,000 against an expectation of 85,000.

The key variable to watch is the 10-year Treasury yield, which rose from 1.5% to over 4.2% in the previous cycle. A hot May CPI could push the yield toward or above 4.75%, likely affecting rate-sensitive assets.

JPMorgan notes that any Fed policy changes are unlikely before late 2026, with markets increasingly anticipating a rate hike rather than a cut, a scenario previously considered unlikely as of February 2026.

4.2% as the Dividing Line: What Each CPI Data Scenario Means for Rate Expectations and Equity Markets

SOURCE: TradingEconomics

SOURCE: TradingEconomics

In the bull case, if headline CPI is at or below 3.9% year-over-year and core is at or below 2.8% month-over-month, markets may reprice late-2026 rate cuts, sparking relief rallies in rate-sensitive equities like QQQ, IWM, and VNQ, while the 10-year Treasury yield retreats.

However, this scenario relies on a significant drop in services inflation and easing energy prices, making it low probability given high WTI levels.

In the base case, a headline CPI of 4.1%–4.3% year-over-year with core at 0.3% monthly and 2.9% annually will maintain the hawkish stance but not accelerate it.

The Fed is likely to stay on hold, leading to range-bound trading in the S&P 500 as investors weigh earnings against a higher-for-longer outlook. A 4.2% print would support this cautious approach.

In the bear case, if the headline CPI reaches 4.4% or higher and core exceeds 3.0%, rate-hike odds could exceed 70%, pushing the 10-year yield toward 5%.

This would compress valuations of long-duration growth stocks, strengthen the US dollar, and create additional pressure on interest-sensitive risk assets.

The author does not hold or have a position in any securities discussed in the article. All stock prices were quoted at the time of writing.

The post May CPI Data Expected to Hit 4.2% Rate Cuts Dead for 2026? appeared first on Tokenist.