Finance Without Frontiers: How Binance and Stablecoins Are Quietly Becoming the Bank Account for 1.3 Billion Unbanked Adults

Finance has always had borders. Banks, licenses, infrastructure, paperwork, and geography decided who gets access and who doesn’t. But the most important shift happening today is not about trading or speculation, it is about access. A parallel financial system is forming quietly, and for more than a billion people, it is the first time they can actually participate in money the way the rest of the world assumes is normal.

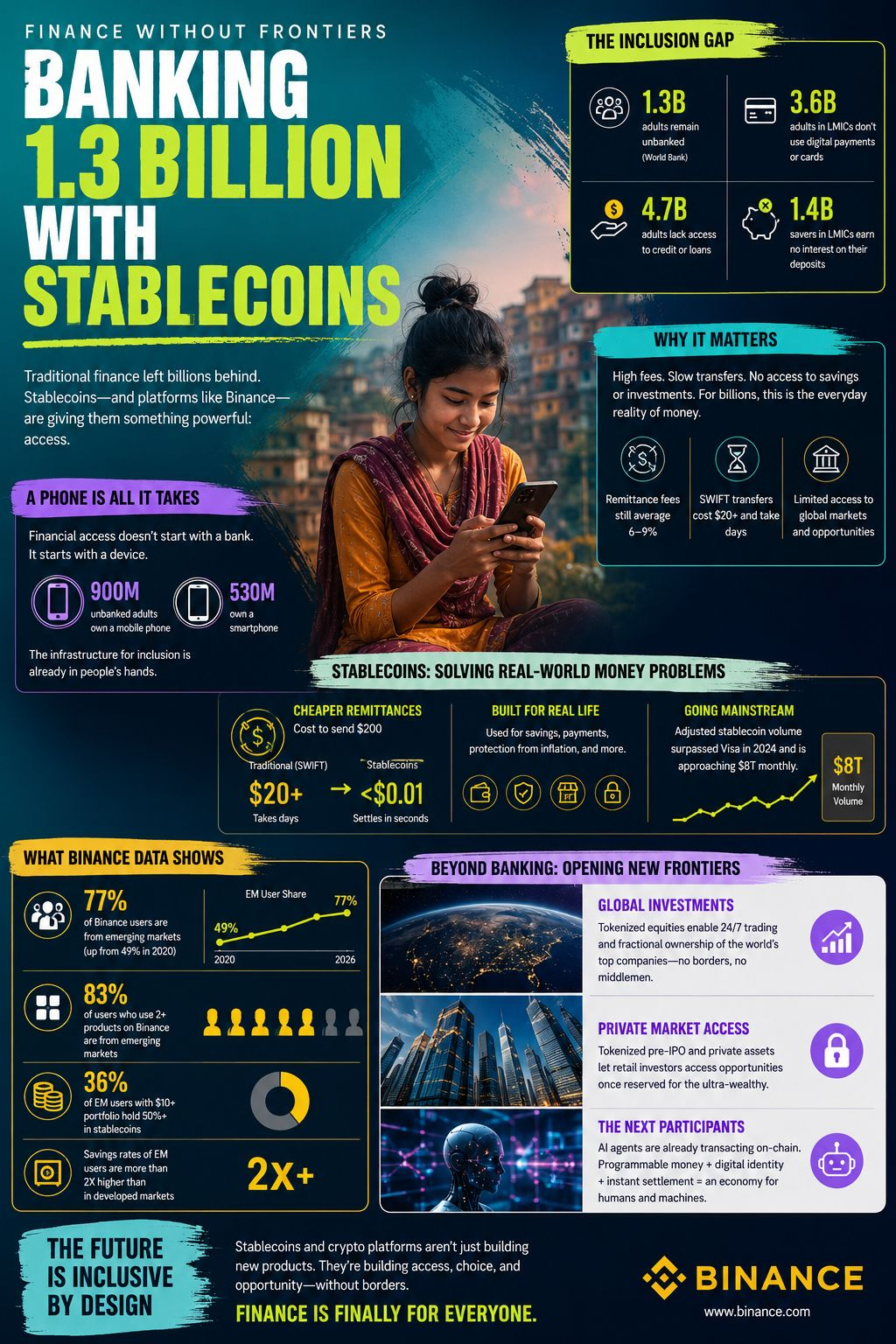

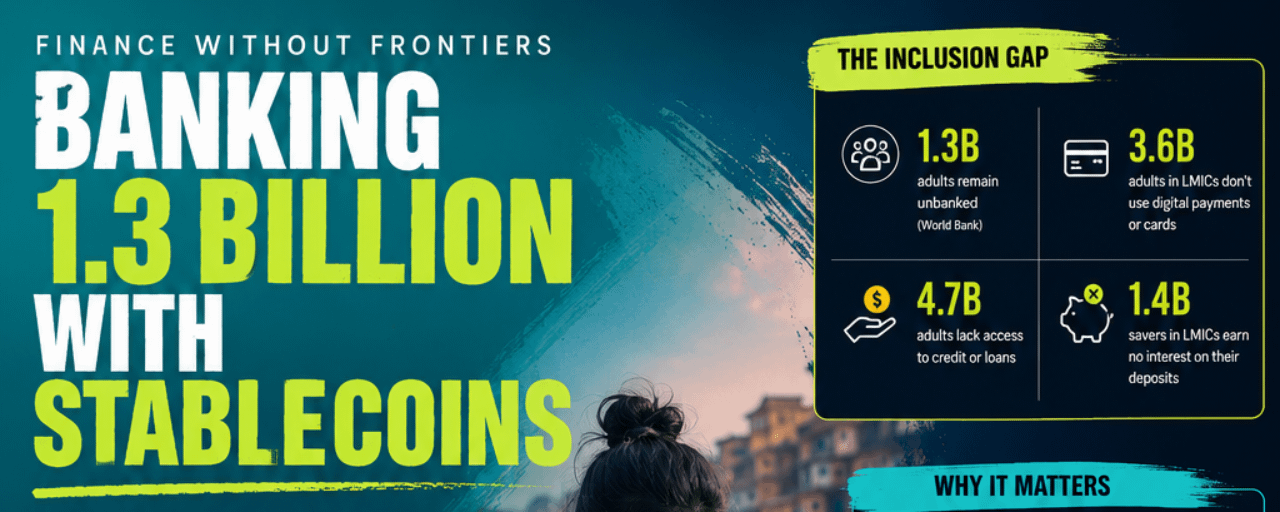

According to the World Bank, around 1.3 billion adults remain unbanked, while billions more are underbanked, lacking credit, savings yield, or reliable digital payment access. In many of these regions, traditional banking didn’t fail suddenly; it simply never scaled. What is emerging now is not a replacement of banks in developed economies, but a substitution in places where banks never fully arrived.

And at the center of this shift is something deceptively simple: a smartphone and a stablecoin.

The Real Story Isn’t Crypto Adoption, It’s Financial Substitution

Crypto is often framed as an investment trend. But Binance Research data tells a different story. Roughly 77% of Binance users are now based in emerging markets, rising sharply from 49% in 2020. That is not a trading pattern, it is a demographic migration of financial activity.

In many low- and middle-income countries, the problem is not the absence of money, but the absence of infrastructure. Credit systems are thin or non-existent. Cross-border transfers are expensive. Savings accounts often yield nothing. And for nearly 3.6 billion adults, digital payments or cards are still not part of daily life.

So users adapt. Instead of waiting for traditional banking expansion, they adopt tools that already work globally. Stablecoins become a store of value. Exchanges become savings platforms. Wallets become payment rails. What emerges is a “shadow banking layer,” not by design, but by necessity.

The result is subtle but profound: crypto is not replacing banking where banking is strong, it is substituting for banking where banking is absent.

A Banking System Built on a Phone, Not a Branch

One of the most overlooked details in financial inclusion data is hardware access. Around 900 million unbanked adults already own a mobile phone, and more than 500 million have smartphones.

That single fact changes everything.

Historically, financial inclusion required physical infrastructure: branches, agents, paperwork, compliance offices. Now it requires only a device already in people’s pockets. This is why mobile money in Kenya, for example, lifted households out of extreme poverty, and why digital financial tools are scaling faster than traditional banking expansion ever did.

On-chain systems take this further. Instead of a domestic mobile-money provider, users access global financial rails directly. There is no “local bank rollout timeline.” There is only connectivity.

This shifts the bottleneck entirely. The constraint is no longer distribution, it is user experience, trust, and regulatory clarity.

Stablecoins: The Invisible Infrastructure of Global Money Movement

If there is one layer driving this transformation, it is stablecoins.

Cross-border payments through traditional systems like SWIFT can cost upwards of $20 and take days to settle. That structure alone makes small remittances economically inefficient, the poorer the sender, the higher the effective fee burden.

Stablecoins collapse that model. Transfers can cost fractions of a cent and settle almost instantly. In practical terms, this is not just “cheaper payments.” It is the removal of friction from global money movement.

The impact is already measurable. Stablecoin transaction volumes have scaled to levels comparable with major global payment networks, and in some datasets, even surpass legacy processors like Visa in adjusted volume metrics.

For users in emerging economies, this matters in very direct ways:

Money sent home arrives in minutes, not days Savings can be held without local currency risk Small transfers become economically viable again

It is not innovation for its own sake, it is cost elimination at scale.

Savings Behavior Reveals the Deeper Shift

One of the clearest signals of real adoption is not trading volume, but savings behavior.

In emerging markets, users are significantly more likely to hold stablecoins as a portion of their portfolio. Binance data shows that a growing share of users keep stablecoins as their primary savings instrument, with adoption rising sharply since 2020.

This is not speculative positioning. It reflects something more fundamental: stablecoins function as a dollar-denominated savings account in places where traditional savings accounts either do not exist or do not preserve value.

Even more telling is behavioral clustering. Users in emerging markets are more likely to use multiple financial products simultaneously, saving, transacting, and investing, all within a single platform. In developed markets, crypto often remains siloed as a trading instrument. In emerging markets, it becomes a financial stack.

Capital Markets Are Expanding Beyond Geography

The inclusion gap is not limited to banking. It extends into investing.

Globally, access to equity markets is still highly concentrated. Only a fraction of adults hold brokerage accounts, and access to major markets like the U.S. remains geographically restricted despite their dominance in global capitalization.

This creates a structural disconnect: the world’s largest companies generate value globally, but ownership access is locally constrained.

Tokenization changes this dynamic by enabling fractional ownership and 24/7 market access. While still early, tokenized assets and pre-IPO instruments are creating pathways for retail users to access markets that were previously reserved for institutional or accredited investors.

The deeper implication is not just accessibility, it is timing. In traditional markets, much of the value appreciation happens before IPO. By the time retail investors gain access, a significant portion of growth has already occurred. Tokenized pre-market instruments attempt to bridge that timing gap.

The Rise of “Financial Operating Systems” in Emerging Markets

A striking pattern in Binance user behavior is the shift from single-use to multi-use financial engagement. Users are not just trading, they are saving, transacting, and allocating capital across products.

This suggests something closer to a financial operating system than an exchange.

In emerging markets especially, where banking services are fragmented or incomplete, platforms that combine savings, payments, and investment functions naturally become central financial hubs. The exchange is not competing with banks on one product, it is replacing multiple disconnected services at once.

The result is a consolidation of financial behavior into one interface, driven not by preference, but by efficiency.

Conclusion: Inclusion Is No Longer About Access, It’s About Infrastructure Choice

The global financial inclusion gap is often described as a social challenge. But the emerging data reframes it as an infrastructure transition.

Traditional banking expanded through physical networks and regulatory systems built over decades. On-chain finance is expanding through mobile penetration and permissionless infrastructure that scales instantly across borders.

The important shift is not that crypto is “banking the unbanked” in a marketing sense. It is that financial activity is reorganizing around systems that are cheaper, faster, and globally accessible by default.

In that sense, stablecoins are not the end product, they are the entry layer. Behind them is a broader transformation where financial services are no longer defined by geography, but by connectivity.

And for 1.3 billion unbanked adults, that difference is not theoretical. It is the first time finance actually works in practice.

#FinanceWithoutFrontiers #StablecoinRevolution #FinancialInclusion"