Hormuz: The Energy Valve of the Global Economy

In most geopolitical crises, the question that dominates headlines is whether a strategic shipping lane has been fully blocked. In the case of the Strait of Hormuz, however, that question is often the wrong one. What ultimately matters is not whether the strait is formally closed, but whether the market still feels confident operating through it.

In the global energy system, logistics operates heavily on confidence. Once that confidence breaks, trade can effectively halt on its own—even without any formal blockade. If war-risk insurance surges, shipping companies begin avoiding the route, and commodity traders become unwilling to bear transport risk, energy flows can stall within days. In other words, the system does not require an official closure of the strait to shut down; a collapse in logistics confidence is often enough.

This is why the Strait of Hormuz should not simply be viewed as a narrow maritime corridor. It functions as the energy valve of the global economy.

Hormuz in the Structure of the Global Energy System

The U.S. Energy Information Administration once summarized Hormuz with a straightforward description: “The Strait of Hormuz is the world’s most important oil transit chokepoint.” This is not a political slogan but rather a technical characterization of the global energy network.

An energy chokepoint typically exhibits three features: extremely large volumes of commodities passing through it, very limited alternative routes, and minimal system slack when disruptions occur. Hormuz fits all three conditions.

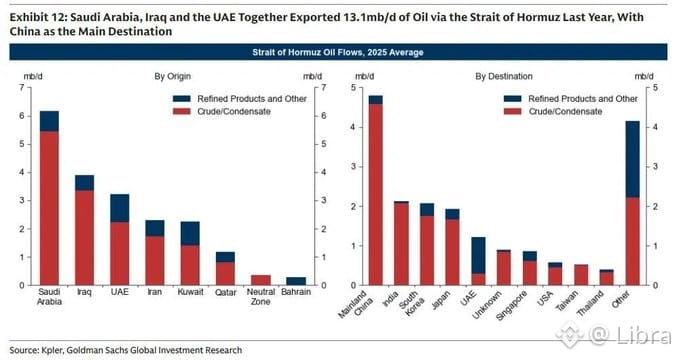

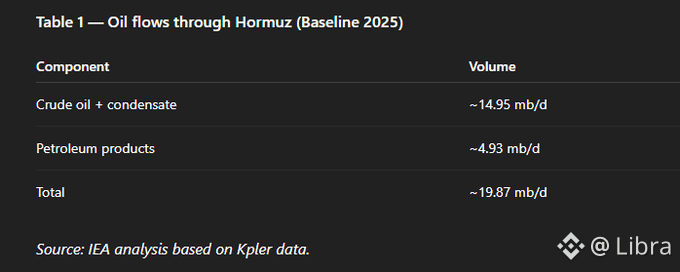

According to data compiled from the IEA, Kpler, and EIA, roughly 20 million barrels per day (mb/d) of crude oil and petroleum products passed through the strait in 2025. This represents approximately 25% of global seaborne oil trade. If we look only at crude oil, the concentration is even more striking: about 15 mb/d of crude oil transits Hormuz each day, equivalent to roughly 34% of global crude oil trade.

This distinction is important. Statements that “about one-third of seaborne oil passes through Hormuz” are technically correct only when referring specifically to crude oil trade. When both crude oil and refined products are included, the share falls closer to 25% of total seaborne oil flows.

These figures align closely with EIA estimates for 2024, which reported roughly 20 mb/d of petroleum liquids moving through the strait daily—equivalent to about 20% of total global petroleum liquids consumption. Beyond oil, Hormuz is also a critical corridor for natural gas. Roughly one-fifth of global LNG trade passes through the strait, much of it originating from Qatar’s Ras Laffan LNG complex, the largest LNG export hub in the world.

Energy Flows Through the Strait

The baseline flow structure of Hormuz highlights just how concentrated global energy logistics have become.

These figures illustrate a key structural reality: roughly a quarter of global seaborne oil trade depends on a single shipping corridor only a few kilometers wide.

The Geometry of a Chokepoint

The vulnerability of Hormuz does not stem solely from the scale of energy passing through it. It also arises from the geometry of the shipping route itself.

On a map, the strait appears relatively wide. At its narrowest point, it spans about 29 nautical miles (approximately 54 kilometers). However, for oil tankers, the cartographic width of the strait is largely irrelevant.

What matters instead is the operational shipping channel. In practice, maritime traffic moves through two primary lanes—one inbound and one outbound—each approximately two nautical miles wide (around 3.7 kilometers), separated by a buffer zone.

This creates what analysts often refer to as operational narrowness: the effective width through which ships can safely navigate. In practical terms, the entire energy output of the Persian Gulf must pass through a corridor only a few kilometers wide. That is what makes Hormuz a genuine strategic chokepoint: enormous energy volumes concentrated through an extremely constrained shipping passage.

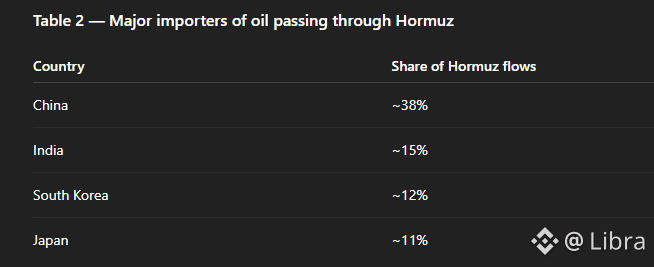

Who Depends on Hormuz the Most

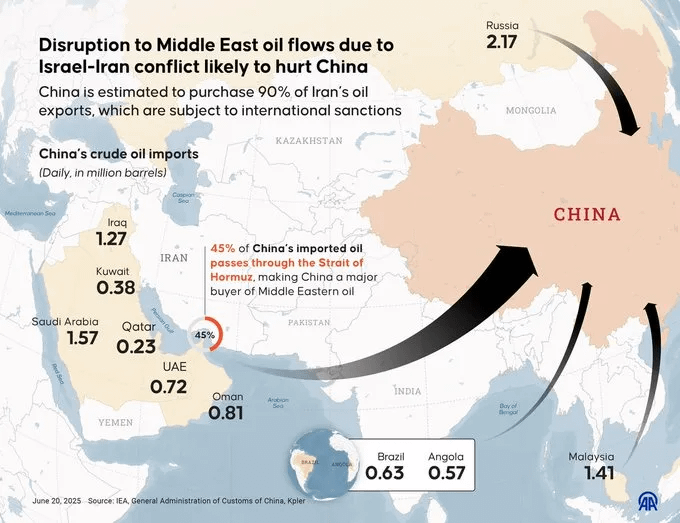

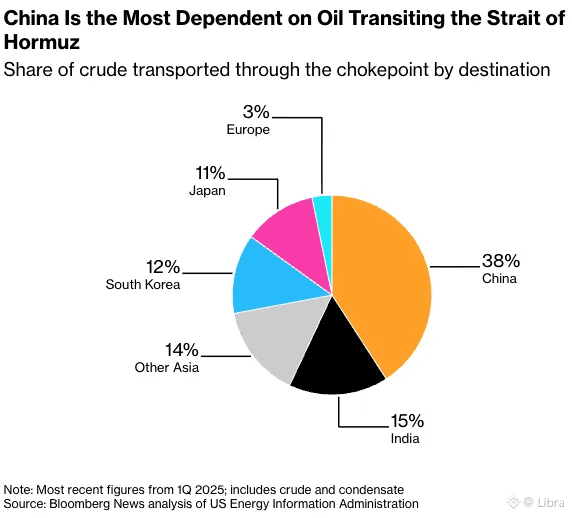

Not all regions depend on Hormuz equally. In fact, Asia absorbs the vast majority of energy flows passing through the strait.

Approximately 90% of oil shipments transiting Hormuz are destined for Asian markets.

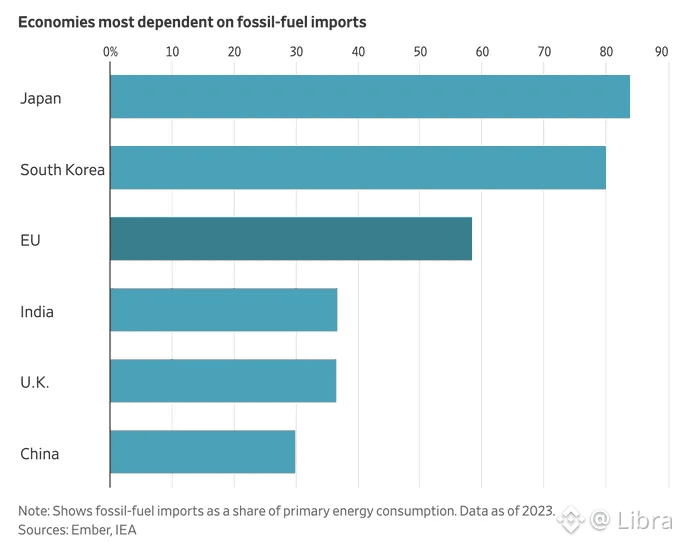

For countries such as Japan and South Korea, more than 60% of total oil imports travel through Hormuz, making their energy systems particularly sensitive to any disruption along this route.

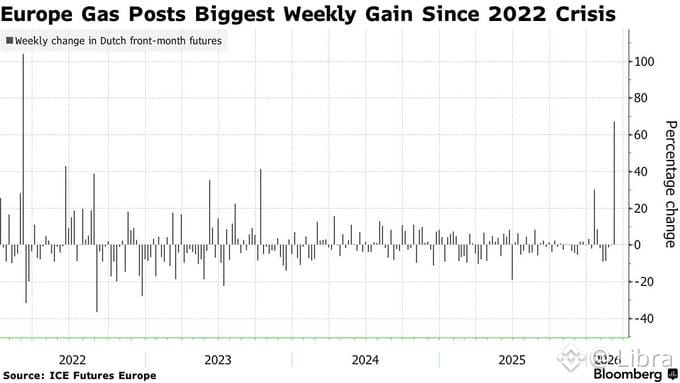

When War Stops Logistics

The fragility of this system became clear when tensions escalated in the Middle East in late February 2026. AIS shipping data compiled by Reuters and LSEG indicated that tanker traffic through Hormuz dropped close to zero within a matter of days.

Importantly, this collapse did not occur because the strait had been formally sealed. Instead, the breakdown occurred because logistics itself began to fail. As military risks rose, war-risk insurance premiums surged. Shipping companies began refusing to transit the area, and energy traders grew increasingly reluctant to assume transport risk.

The shock therefore propagated through the system in a predictable sequence:

military risk → insurance costs → shipping withdrawal → freight rate spikes → LNG disruptions → energy price increases.

This chain reaction illustrates how energy crises often begin not with physical shortages, but with disruptions to transportation and risk pricing.

LNG: The Most Fragile Link

While crude oil can sometimes be rerouted through alternative routes, LNG flows are far less flexible. Around 20% of global LNG trade passes through Hormuz, with the majority originating from Qatar.

Unlike crude oil, LNG transportation depends on specialized carriers, liquefaction plants, and regasification terminals. These infrastructural constraints make rerouting far more difficult. As a result, disruptions to Hormuz can translate rapidly into energy stress across Asian gas markets.

From Energy Prices to Inflation

The implications of a Hormuz disruption extend well beyond the oil market. Energy price shocks tend to propagate quickly through the broader economy.

Empirical macroeconomic models suggest that every $10 increase in oil prices can raise global inflation by roughly 0.1 to 0.4 percentage points. The mechanism is straightforward: higher energy costs increase transportation expenses, raise industrial production costs, and eventually feed into consumer prices.

This dynamic creates what economists call cost-push inflation, one of the most challenging forms of inflation for central banks to manage. If sustained long enough, such shocks can push economies into stagflation, a combination of slowing growth and persistently high inflation.

When the State Must Absorb Systemic Risk

In situations like these, logistics risk often exceeds what private markets can absorb. When critical energy transport routes become unstable, governments frequently step in to stabilize the system.

During the 2026 Hormuz crisis, the United States considered several extraordinary measures. Among them was a potential $20 billion reinsurance facility through the U.S. International Development Finance Corporation (DFC) aimed at supporting war-risk insurance for energy shipping. At the same time, Washington explored the possibility of deploying naval escorts for oil tankers to ensure the continued flow of energy through the region.

Such interventions represent a form of state absorption of systemic logistics risk. When a strategic energy corridor is threatened, governments may effectively backstop global trade flows.

Hormuz and the Future of Energy Security

Ultimately, Hormuz is more than a geopolitical flashpoint. It is a reminder of how fragile the infrastructure of global energy trade can be.

For decades, globalization operated under the assumption that major maritime trade routes would remain open and secure. Yet the global energy system depends on a handful of geographic chokepoints—Hormuz, Malacca, Bab el-Mandeb, and the Suez Canal.

Disruption at any one of these nodes can ripple through global logistics networks.

In response, many countries are now reassessing their energy strategies: diversifying supply sources, expanding strategic reserves, and developing alternative transport routes.

In this sense, the world may be gradually shifting away from a model of cost-optimized globalization toward one centered on supply chain security.

And within that emerging system, the Strait of Hormuz stands as a powerful reminder that geography remains a form of power in the global economy.

Whether Trump chooses to prolong or de-escalate the conflict in the Middle East will not only shape the geopolitical landscape, but also directly determine the stability of the Strait of Hormuz - the energy valve of the global economy and, in turn, the security of global oil supply.”