When I first looked at the structure surrounding @MidnightNetwork , my instinct was to treat the token layer as another familiar pattern. A network appears, a native asset accompanies it, and the asset becomes the economic glue holding the system together. That assumption is so common in crypto that people rarely stop to question it. What struck me after spending more time thinking about NIGHT is that the question itself might be more interesting than the answer.

Many people approach this topic from a simple angle. If a network exists, the token must exist. The reasoning feels obvious. Yet the deeper issue is not whether a token can exist, but whether it must exist for the system to function properly. That difference matters because it reveals something about how infrastructure is actually built.

The common misconception around projects like Midnight network is that the token primarily exists as a speculative instrument. The surface narrative suggests that NIGHT is simply another tradable asset attached to a privacy-oriented blockchain. That view misses the structural logic underneath.

My thesis is simple. The $NIGHT token is less about price speculation and more about coordinating behavior across a network that must prove things without revealing everything. In other words, the token becomes a coordination tool rather than a product. Understanding that helps explain why it might be necessary.

On the surface, the Midnight system appears straightforward. Transactions settle on a ledger, users interact with contracts, and the token circulates through the system. Anyone observing the chain sees activity happening openly. That layer feels familiar to anyone who has used a public blockchain.

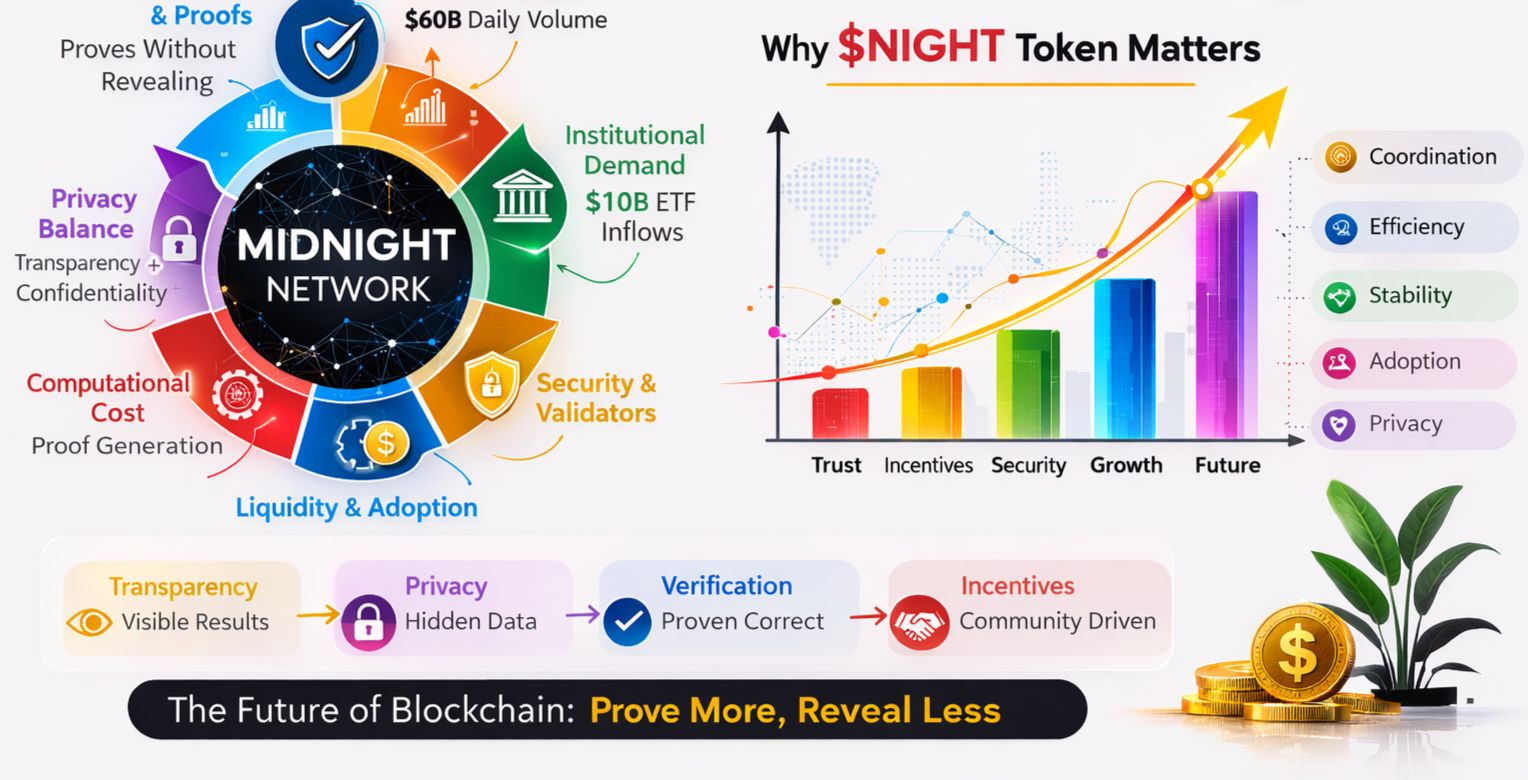

Underneath, however, the structure is different. The network relies on mathematical verification processes that allow a transaction to prove it followed the correct rules without revealing all internal information. In simple terms, the system confirms that something happened correctly without exposing every detail of how it happened.

That design enables a particular kind of coordination. Participants can verify outcomes without exposing sensitive information. Financial agreements, data exchanges, and automated processes can execute privately while the final proof remains visible to the network.

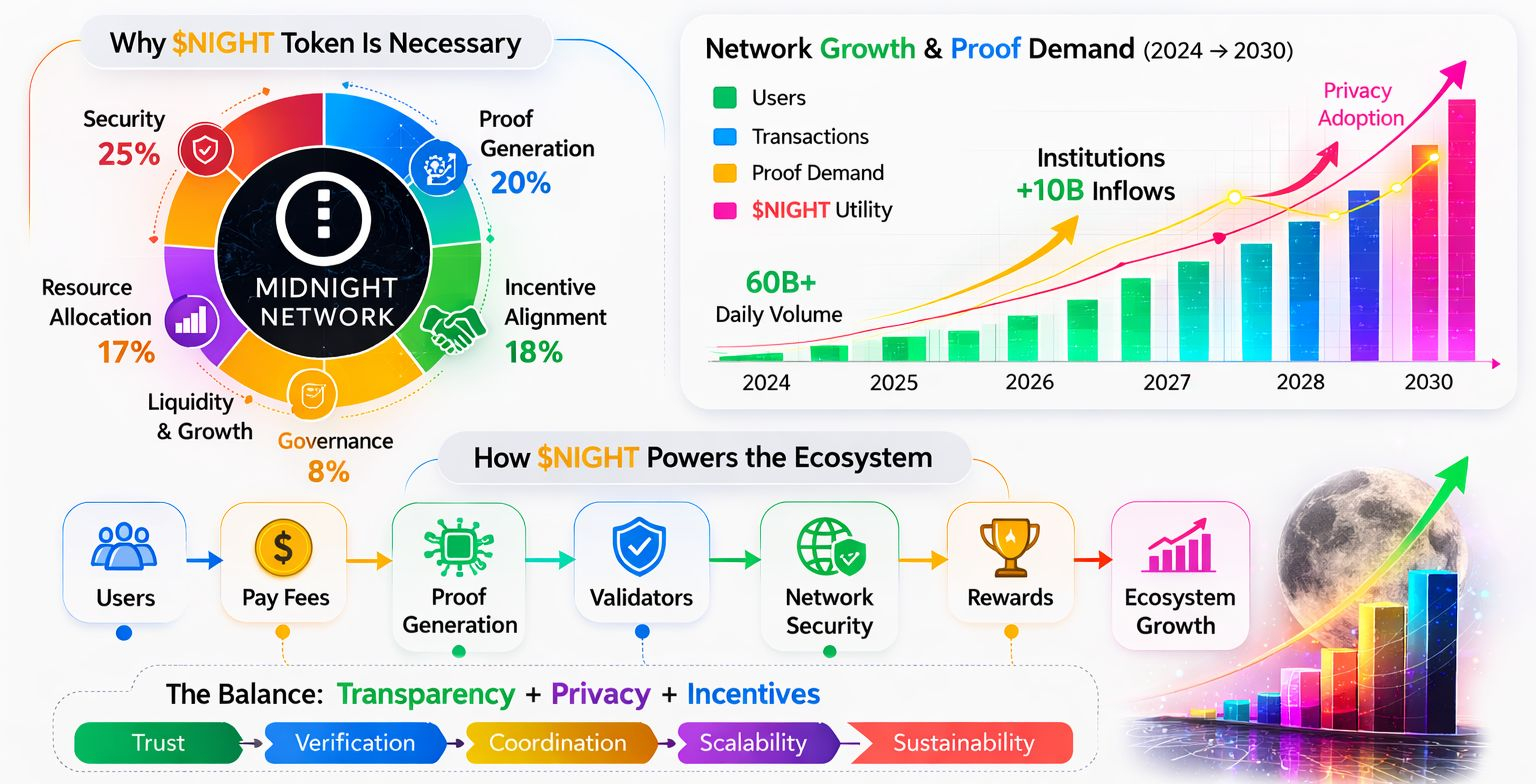

That balance creates a new kind of economic pressure. Someone must pay for the computational work required to generate those proofs. Someone must also secure the network so that those proofs remain trustworthy.

This is where NIGHT enters the structure.

On the surface, the token simply looks like a payment mechanism. Users spend it to interact with the system and validators receive it for maintaining the network. That explanation sounds ordinary because most blockchains operate this way.

Underneath, however, the token becomes a resource allocation system. It determines who contributes computational work, who verifies transactions, and how scarce network capacity gets distributed across users. Instead of a central operator deciding these questions, the token market coordinates them.

That coordination matters because the computational requirements involved in proof generation can be significant. Some modern verification systems require far more processing than ordinary transactions. If the cost of generating proofs rises too high, participation falls. If it falls too low, the network risks abuse.

The token becomes the mechanism balancing that tension.

Understanding that structure helps explain why this conversation is happening at a moment when the broader crypto market is changing. In recent months global crypto spot trading volume has frequently moved above sixty billion dollars per day across exchanges. That number matters because it signals the scale of financial activity now flowing through digital infrastructure.

When markets operate at that scale, participants begin demanding predictability. Traders want settlement systems that behave consistently during volatility. Institutions want systems where verification can be trusted without exposing confidential information.

That pressure creates space for privacy-focused networks to experiment with different coordination models.

Meanwhile institutional capital is entering the market through regulated investment vehicles. Bitcoin exchange traded funds in the United States have already attracted more than ten billion dollars in inflows. That figure signals something subtle. Traditional capital is slowly becoming comfortable interacting with blockchain infrastructure.

Yet institutional participants rarely operate inside fully transparent environments. In traditional finance, trade negotiations, risk strategies, and contract structures usually remain private until settlement occurs. Public blockchains inverted that pattern by exposing nearly everything.

Systems like Midnight network attempt to restore a different balance.

Surface transparency remains visible. Transactions settle, fees are paid, and the ledger stays auditable. Underneath, however, sensitive computation can remain private while still being proven correct.

That structure raises the central question again. If the system already functions through mathematical verification, why is a token needed at all?

One argument suggests that such networks could rely purely on fees paid in existing currencies. Under that model, participants would simply pay for computation and verification services without introducing a native asset.

That argument sounds reasonable at first glance. Yet it introduces a coordination problem. Without a native token, there is no built-in mechanism aligning the incentives of validators, developers, and users over long periods of time.

The token becomes a shared economic reference point. It ties the interests of those securing the system with those building applications on top of it.

There is also a liquidity dimension that often goes unnoticed. Crypto markets currently move billions of dollars across exchanges every day. Liquidity pools determine how easily assets can move between participants. A native token creates a measurable economic signal that markets can respond to.

Early signs suggest that liquidity signals influence how developers choose which ecosystems to build in. If a network lacks economic depth, builders often move toward environments where capital and users already exist.

That momentum creates another effect. Tokens provide a way for networks to distribute ownership across participants rather than concentrating it within a single organization. Whether that distribution ultimately works remains to be seen, but the structure changes how incentives evolve.

Of course the token model introduces risks.

Speculative markets can distort infrastructure incentives. When token prices become the primary focus, participants sometimes ignore the underlying system design entirely. Networks that were intended to coordinate computation can instead become vehicles for short-term trading behavior.

Regulation introduces another layer of uncertainty. Privacy-oriented systems often face scrutiny from policymakers concerned about illicit finance. Even when networks maintain auditability through mathematical verification, regulators may remain cautious.

That tension places additional pressure on how tokens like NIGHT are perceived.

Developers face a different concern. Integrating privacy-preserving computation into real applications requires new tools and design patterns. Builders often prefer ecosystems where documentation, liquidity, and developer communities already exist. Convincing them to experiment with new environments requires time.

Still, there is a broader structural trend forming underneath these debates.

For the past decade most blockchain innovation focused on throughput. Networks competed to process more transactions per second and reduce costs. That phase addressed one part of the infrastructure problem.

Now another issue is emerging. As blockchain systems begin supporting financial agreements, automated services, and AI-driven coordination tools, information management becomes just as important as computational speed.

Participants must decide not only how transactions execute but how much information those transactions reveal.

Privacy verification systems represent one attempt to answer that question.

Understanding that helps explain why the token layer exists at all. It provides the economic structure coordinating participants who must generate proofs, secure the network, and maintain predictable settlement under pressure.

Whether NIGHT ultimately proves necessary will depend on how the ecosystem evolves. Markets will test the design during periods of volatility, regulatory scrutiny, and developer experimentation.

If the system holds, the token may reveal something deeper about where blockchain infrastructure is heading.

Not toward complete transparency.

And not toward complete secrecy.

But toward a quieter balance where networks prove just enough for trust to exist while keeping the rest of the system beneath the surface.#night