Looking at it as economic infrastructure, not just another Web3 story

Personal shift yeah, I used to fall for narratives too

I’ll be honest.

For a long time I judged crypto projects the same way everyone else does by the story.

Identity. Ownership. Sovereignty. Freedom.

All the big words that sound good in threads and conferences.

And look, those ideas matter. I’m not saying they don’t.

But after watching a few cycles, a few crashes, a few “next big things” turn into ghost towns… you start noticing a pattern.

Narratives don’t survive on their own.

A wallet isn’t infrastructure.

A token isn’t utility.

And identity by itself doesn’t build an economy.

What actually lasts are the boring layers.

The stuff that sits between people, apps, institutions, payments, rules, permissions — all the messy real-world things nobody wants to talk about.

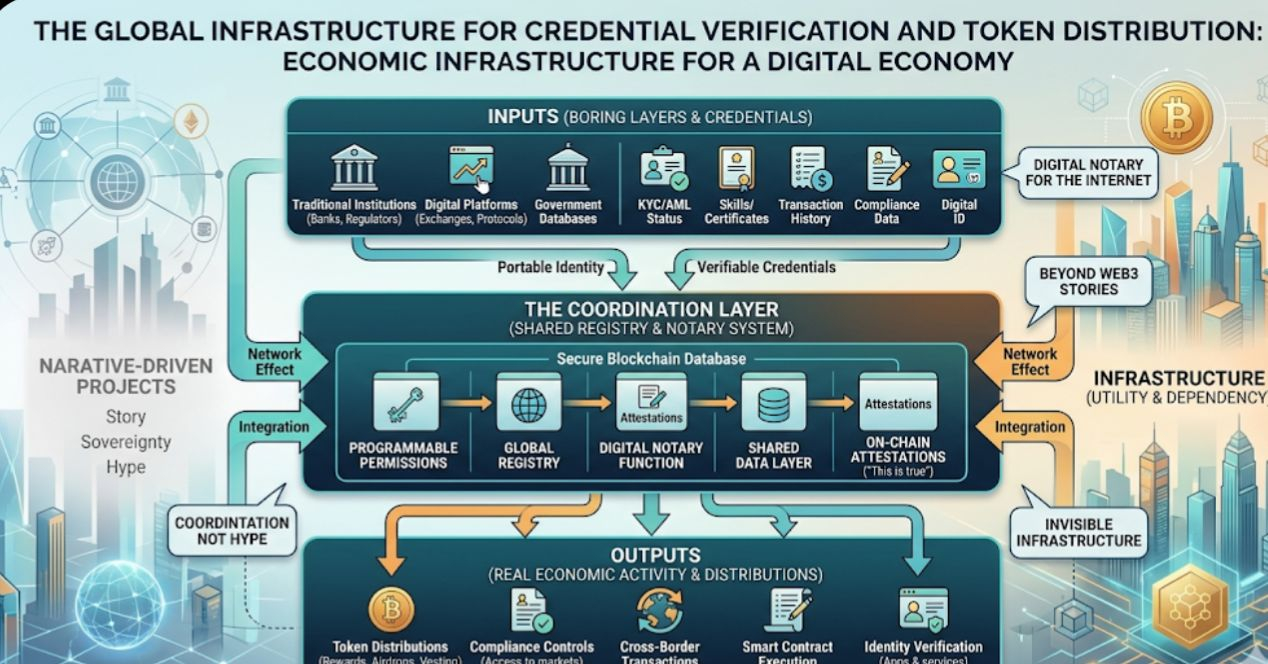

That’s why this whole idea of global credential verification and token distribution infrastructure caught my attention.

Not because it sounds cool.

Because it sounds necessary.

And those are very different things.

Identity is nice. Infrastructure pays the bills.

Most identity projects stop at ownership.

You own your data.

You control your wallet.

You prove who you are.

Okay. Great.

Now what?

Here’s the thing people don’t talk about enough identity only matters when it connects to action.

Transactions.

Agreements.

Compliance.

Access.

Payments.

Permissions.

That’s where this model gets interesting.

Instead of treating identity like a badge, it treats credentials like inputs to real economic activity.

The easiest way to think about it?

It’s a digital notary layer for the internet.

Not flashy.

Not viral.

Useful.

You issue a credential once.

The network verifies it.

Apps read it.

Contracts use it.

Payments depend on it.

That’s infrastructure.

Not a narrative.

Why this matters more in the Middle East, South Asia, and similar regions

People in the West sometimes miss this completely.

The problem in a lot of regions isn’t lack of tech.

It’s lack of coordination.

Different countries.

Different regulators.

Different banks.

Different databases that don’t talk to each other.

Every cross-border action turns into paperwork.

You want to move money? Verify.

You want to sign something? Verify.

You want access? Verify again.

Traditional systems fix this with intermediaries.

Digital systems need something else.

They need:

portable identity

verifiable credentials

shared registries

programmable permissions

Without that, tokenization stays a demo.

Without that, digital finance stays fragmented.

So when I look at something like this, I don’t see a dApp.

I see a coordination layer.

And those are rare.

The core idea basically a programmable notary system

At the center of this whole model sits one simple thing:

Attestations.

Which sounds technical, but it’s really not.

An attestation is just a statement on-chain that says

“this is true.”

Think notarized document, but digital.

And reusable.

And readable by smart contracts.

Who can issue them?

Institutions.

Protocols.

Organizations.

Verified users.

Who uses them?

Apps.

Contracts.

Exchanges.

DAOs.

Compliance systems.

Here’s where the network effect kicks in.

One attestation doesn’t matter.

Ten don’t matter.

It matters when everyone starts reading the same registry.

If that happens → it becomes infrastructure.

If that doesn’t happen → it turns into a static database nobody needs.

I’ve seen this before.

This part decides everything.

Where this fits in the current market cycle

Every cycle has its thing.

One cycle was all about L1s.

Then liquidity.

Then restaking.

Then capital routing.

You’ve got projects focused on moving money faster.

Others focused on creating yield.

Others focused on execution.

This sits in a different category.

Coordination.

It doesn’t move capital.

It makes capital movement possible.

That means slower hype.

Longer build time.

Harder adoption.

But if it works?

It becomes invisible infrastructure.

And invisible infrastructure usually captures more value than the flashy stuff.

People don’t like hearing that.

Still true.

The real test what happens when rewards stop

This is where things get tricky.

Everyone looks good during incentives.

Users farm.

Developers test.

Activity spikes.

Dashboards look amazing.

Then rewards stop.

And suddenly… silence.

So the real questions are simple.

Are credentials still being issued without rewards?

Are real institutions involved or just crypto projects?

Are developers building this into apps, or just experimenting?

Do users need it, or are they just getting paid to click?

If usage dies when incentives die, it’s not infrastructure.

It’s marketing.

If usage stays, then you’ve got something real.

That’s the difference.

Risks yeah, there are a lot

Let’s not pretend this part is easy.

This kind of system fails more often than it works.

Possible problems?

Low adoption → registry nobody reads

Too complex → devs ignore it

No institutional trust → no real credentials

Only reward farming → zero retention

Too many competing standards → fragmentation

Infrastructure only works when everyone agrees on the same layer.

That’s the hardest problem in crypto.

Not building tech.

Getting people to depend on it.

What I watch instead of price

Honestly, price tells you nothing here.

Behavior tells you everything.

Good signs:

steady usage, not spikes

real partnerships, not just announcements

developers integrating, not just testing

credentials required, not optional

repeat issuers, not one-time campaigns

apps that break if the registry disappears

Bad signs:

only airdrop activity

only testnet users

only hype on X

no banks, no regulators, no real entities

no apps that actually need it

Infrastructure proves itself one way.

Dependency.

When other systems stop working without it…

That’s when it has value.

Until then?

It’s still a theory.

@SignOfficial #SignDigitalSovereignInfra $SIGN