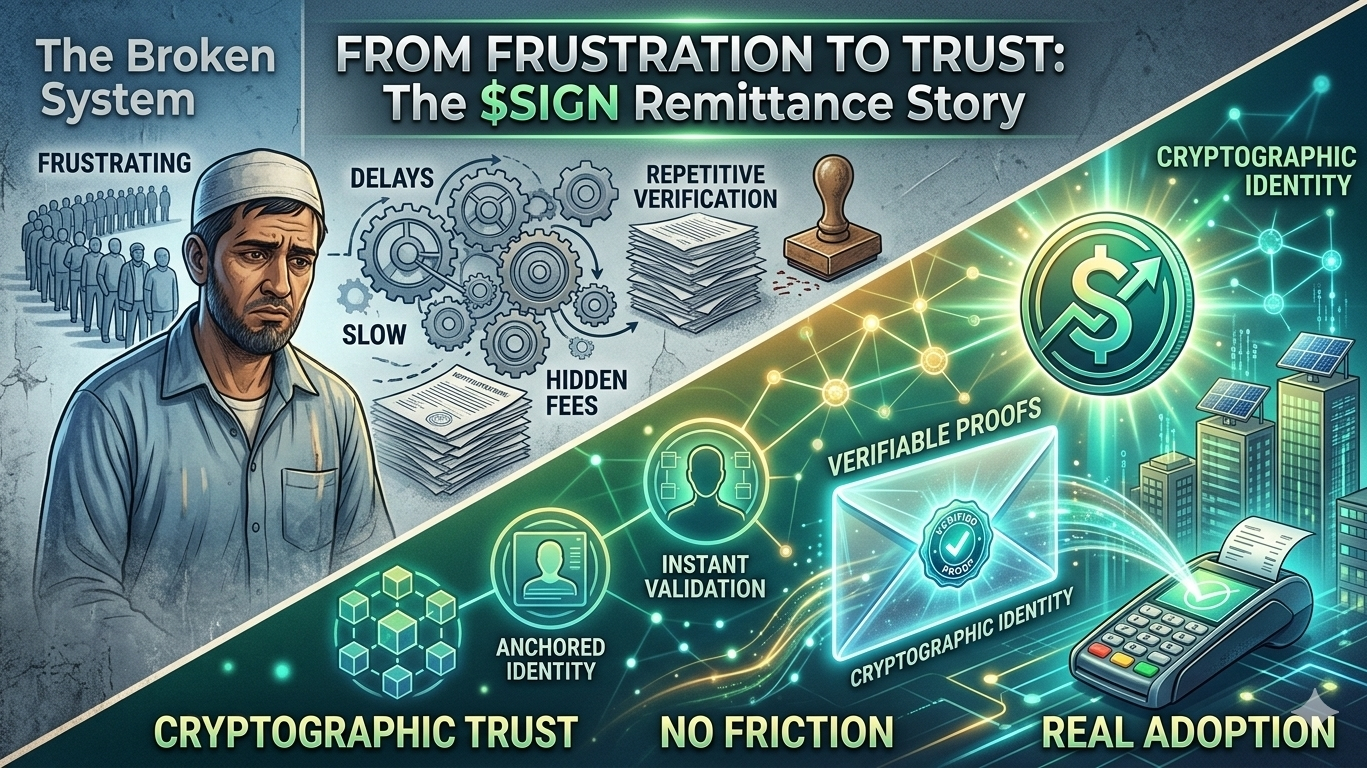

@SignOfficial l remember the first time I sent money back home while working abroad. It should have been simple, almost routine. Instead, it turned into a slow, frustrating process filled with delays, hidden fees, and constant verification steps that felt repetitive and unnecessary. At that time, I didn’t question the system much. I just assumed this was how cross-border payments worked — slow, complicated, and slightly unreliable. But after facing the same issues again and again, it stopped feeling normal. It started feeling broken. That shift in perspective changed how I look at financial systems today, especially blockchain projects. Now, I don’t care much about hype or headlines. I care about whether something actually fixes a real-world problem people deal with every day. That’s exactly why $SIGN caught my attention

What drew me in wasn’t noise or marketing — it was the core idea behind it. The question it raises feels simple but powerful: can we prove identity and transaction validity without all the friction that usually comes with it? In traditional remittance systems, the biggest issue isn’t always moving money — it’s proving everything around that transaction. Who you are, where the money came from, whether it’s legitimate — all of that slows things down. According to what I’ve seen, Sign approaches this differently by building a system where identity is cryptographically anchored, and transactions are backed by verifiable proofs that confirm everything is valid without exposing sensitive information. That idea alone feels like a shift. It’s less about revealing everything and more about proving just enough.

The easiest way I can explain it is this: imagine sending a sealed envelope with a verified stamp. The person receiving it doesn’t need to open it to trust that it’s real. That’s the kind of logic Sign seems to be applying to transactions. If this works the way it’s intended, it could allow financial institutions to validate transfers instantly without putting users through repeated verification loops or exposing personal data unnecessarily. The role of the token also fits into this structure — it helps keep validators honest and active. They are expected to maintain accuracy and uptime, and if they fail, there are consequences. That kind of incentive model matters because, in many cases, the real delay in remittances isn’t money itself — it’s the time spent verifying everything around it.

But here’s the part that matters most to me: none of this means anything if people don’t actually use it. A system can look perfect on paper and still fail in the real world. Right now, $SIGN is sitting in that early stage where things could go either way. It has some traction — trading activity, a growing number of holders, and enough liquidity to show it’s not just sitting idle. But it’s still early. That means the real story hasn’t been written yet. What I’m watching isn’t the price. It’s behavior. Are people coming back to use it again? Are institutions testing it in real environments? Is it becoming part of actual payment flows, or just another asset people trade and forget?

Because in the end, that’s where the difference shows. If workers and institutions don’t keep using it, then all those proofs and systems don’t really matter. They stay theoretical. But if adoption starts to build — even slowly — then something interesting happens. The network becomes stronger with every new user. Validation becomes faster, trust becomes easier, and the system starts to prove its value naturally. The challenge, though, is getting there. Integrating something like this into existing financial systems isn’t easy. It takes time, regulatory clarity, and real commitment from institutions that are often slow to change.

That’s why I’m paying attention to the signals that actually matter — consistent usage, successful pilot programs, and whether validators are doing their job without issues. If those pieces start falling into place, then coul move beyond being just another blockchain idea and become something people rely on. But if adoption stalls or usage doesn’t stick, then it risks becoming just another concept that sounded good but never fully delivered. For me, that’s the real lens: not hype, not short-term price moves, but whether it continues to be used when the excitement fades. Because in something as practical as remittances, value isn’t created by attention — it’s created by solving a problem people are tired of dealing with.

#SignDigitalSovereignInfra $SIGN