Every cycle there are a few infra names that feel like pure narrative and a few that are actually shipping into the real world—$SIGN sits a lot closer to the second bucket from what I’ve seen so far. Over the last couple of years, governments have gone from “maybe blockchain one day” to actively exploring sovereign digital rails, and Sign has been positioning itself as the backbone for those national-scale systems rather than just another retail-facing DeFi toy.

Zooming out for a second: the big unlock in this cycle isn’t just higher TPS or cheaper swaps, it’s whether we can run money, identity, and capital programs on shared rails without handing the keys to a single cloud provider or foreign jurisdiction. The Sign Stack is literally designed around that idea—three pillars for a new money system (CBDCs and regulated stables), a new ID system (verifiable credentials tied to national identity), and a new capital system (programmable distribution of grants, subsidies, and benefits). If you care about “digital sovereignty” beyond slogans, that combo is basically the minimum viable state stack.

At the protocol layer, Sign leans on an omni-chain attestation network that lets issuers create verifiable on-chain credentials which can be reused across apps and even across chains. Instead of every bank, exchange, or government agency building its own closed KYC/identity silo, they can plug into Sign Protocol to issue and verify standardized attestations—things like “this user passed KYC here” or “this address is eligible for X program”—without constantly re-collecting raw data. On paper that sounds niche, but in practice it’s the boring plumbing you need before CBDCs, compliant DeFi, or large-scale social programs can run on-chain at all.

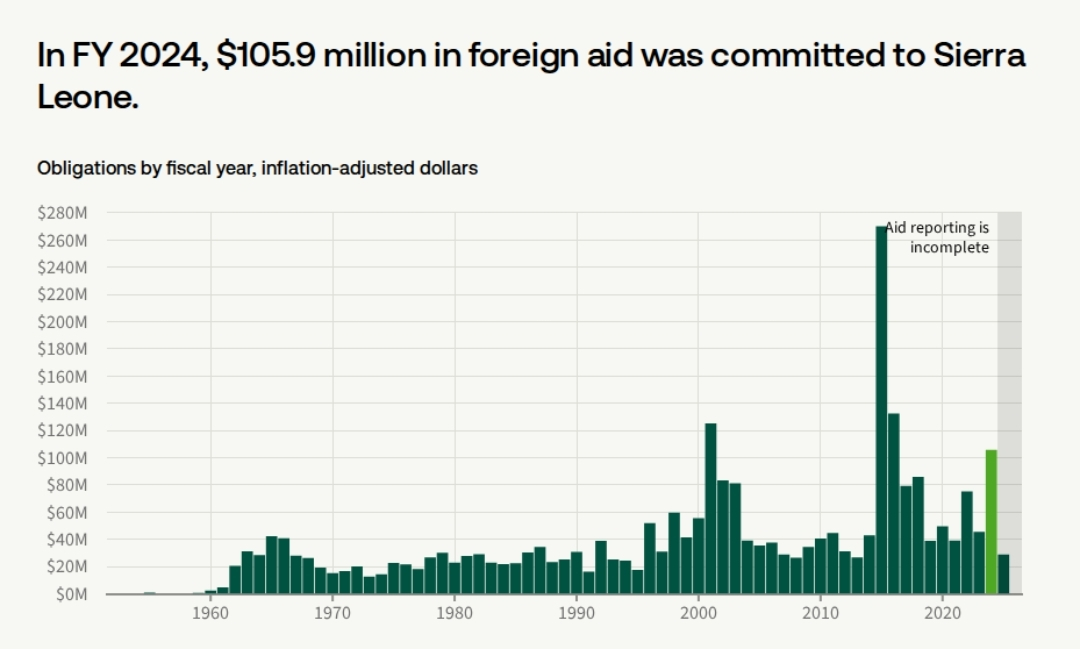

What makes me take it more seriously is the hard data behind the narrative. By 2024, Sign’s infra had already managed token distributions exceeding 4 billion dollars’ worth via its TokenTable product, acting as the vesting and airdrop backbone for multiple ecosystems. The team generated $15 million in revenue in 2024 and positioned Sign as one of the rare profitable Web3 infra providers, which is very different from the usual “TVL but no business model” story. On the client side, they’ve landed actual government work with countries like the UAE, Thailand, and Sierra Leone, which is exactly the kind of high-friction, long-sales-cycle business most crypto teams avoid.

On the adoption and activity side, the attestation network has already processed more than three million on-chain attestations and helped route token distributions worth multiple billions across different platforms. That tells me developers and institutions aren’t just reading the whitepaper—they’re actually using the rails to move value and credentials at scale. Add in the funding raised from serious backers (including a multi-region Sequoia presence) and a 12 million dollar token buyback funded from real revenues, and you get a picture of a project that understands both enterprise and token-market optics. For a governance and infra token, that “profit feeds buyback” loop is pretty rare in this space.

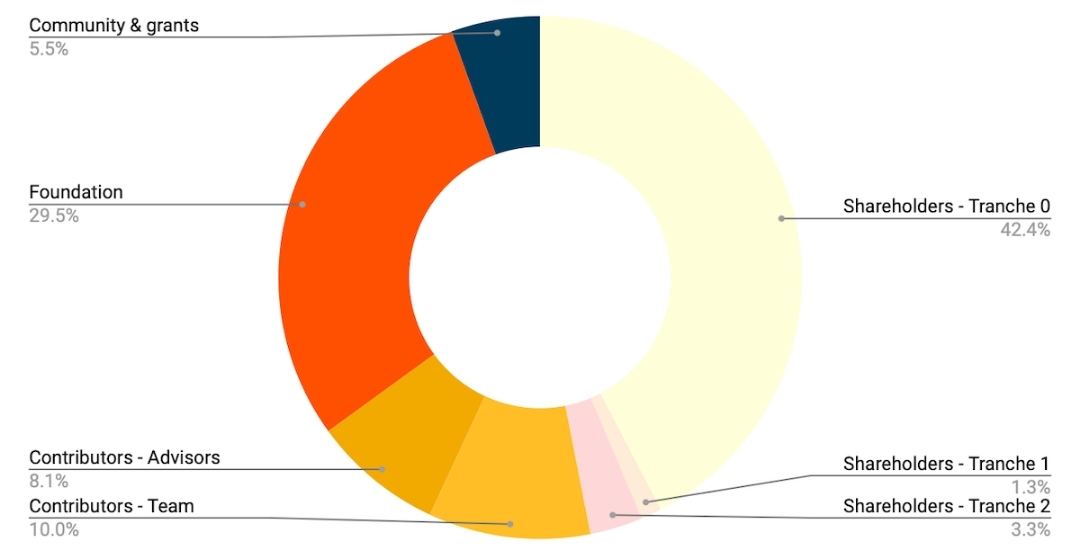

Token-wise, $SIGN sits at the center as a coordination asset: it’s used to pay protocol fees, incentivize attesters/validators, and govern upgrades across the ecosystem. The total supply is 10 billion tokens, with roughly 40 percent earmarked for community incentives and the rest split between early backers, team, partners, and the foundation, which is a pretty standard but still concentrated structure for an infra play. If the B2G side really scales—think CBDC rails and national ID hooks—that incentive pool becomes the fuel to keep developers, credential issuers, and verifiers aligned as more countries and enterprises plug in.

Now, the risks. Governments move slowly, and “sovereign infra” is one of the most political markets you can choose; a change in leadership or regulation can delay or kill deployments that looked certain on paper. The business model is also skewed heavily toward large institutional and government clients, which is amazing when it works but leaves tokenholders exposed to a small number of big relationships and long procurement cycles. On top of that, a 10 billion supply with significant allocations to insiders always raises the usual questions around emission schedules, unlock overhang, and whether buybacks or real usage can offset future selling pressure.

My base case right now: I treat $SIGN as one of the higher-conviction infra bets in the “digital sovereignty” lane, but not something I’d blindly chase on green candles without watching how real deployments and policy timelines evolve over the next 12–24 months. If governments actually roll out the planned digital money and ID systems on Sign’s rails, that’s a strong fundamental unlock; if those deals stall or move to competing stacks, the token can still trade like a nice story but the upside compresses fast. Personally I’m keeping it on my infra watchlist, tracking partner announcements and usage metrics (attestation counts, distribution volumes, government pilots) more than day-to-day price noise.

As always, this is just my read from the screen and the docs, not a guaranteed roadmap to profits, so size and time your own exposure if you decide to get involved with SIGN or any related infra plays.

Not financial advice. Do your own research.