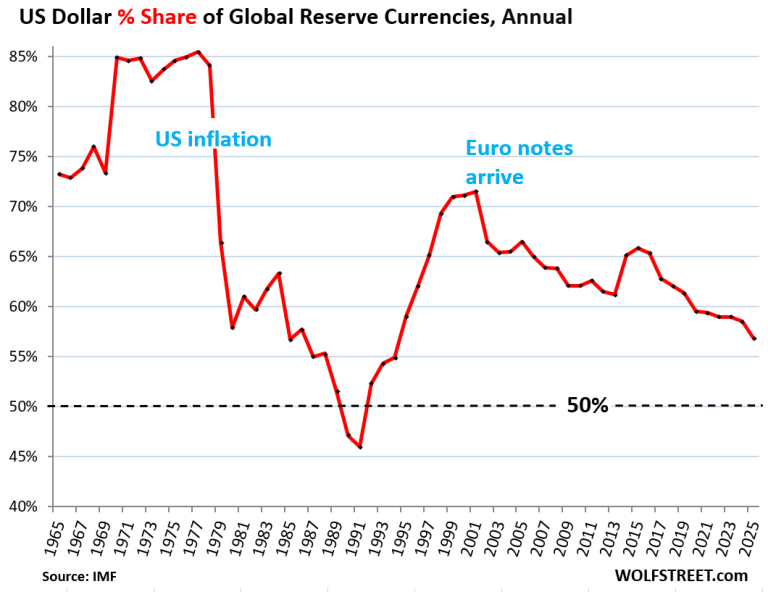

The dominance of the US dollar in global finance is facing a slow but persistent shift. According to the latest IMF data on the Currency Composition of Official Foreign Exchange Reserves (COFER), the US dollar’s share of global reserves has dropped to 56.8% as of Q4 2025—its lowest level since 1994.

Understanding the Shift

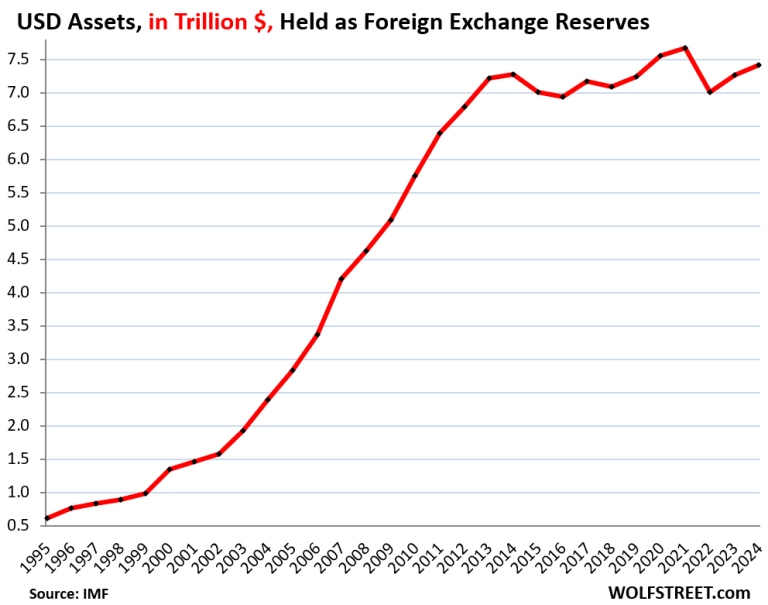

Contrary to sensationalist headlines, foreign central banks are not "dumping" US assets. In fact, USD-denominated holdings have remained relatively stable at approximately $7.46 trillion. The decline in the dollar’s percentage share is actually driven by diversification. Central banks are aggressively loading up on:

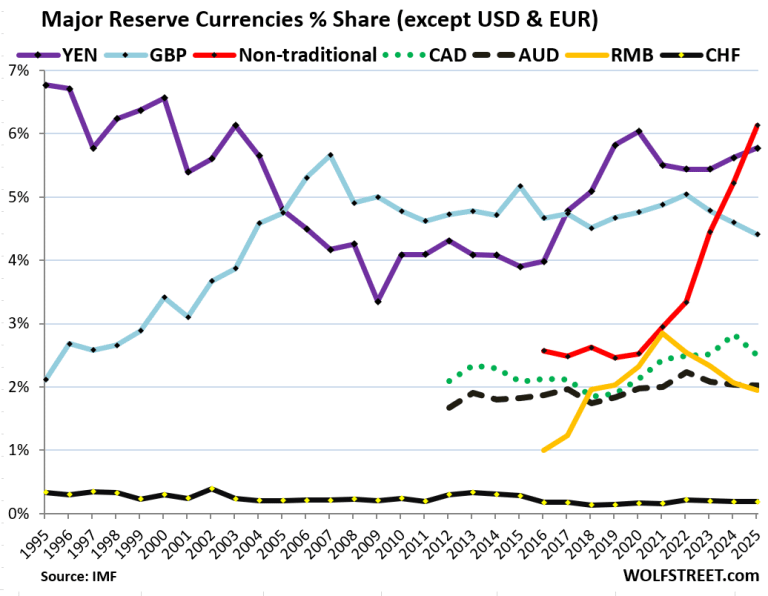

Non-Traditional Currencies: A basket of dozens of smaller currencies (excluding the majors like the Euro or Yen) now accounts for 6.1% of reserves, surpassing the Japanese Yen.

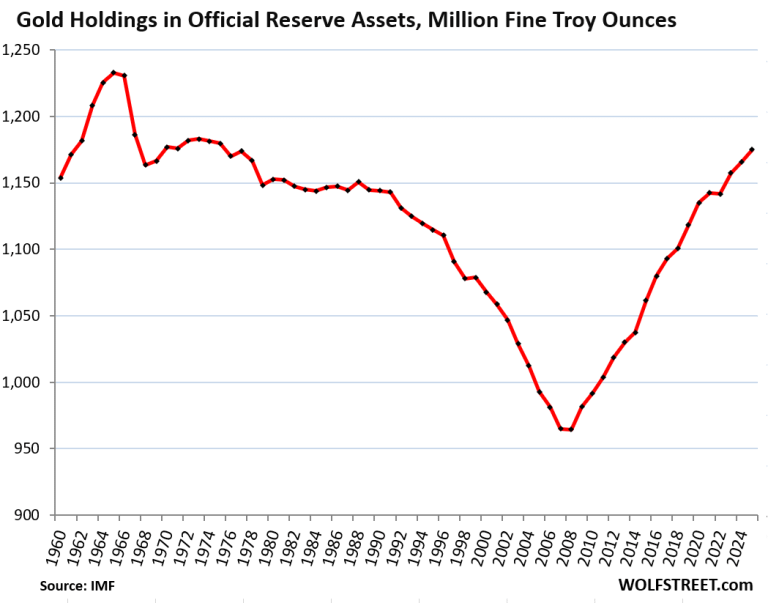

Gold: After decades of selling, central banks have pivoted back to gold as a primary "non-currency" diversification tool, with official holdings reaching levels not seen since 1977.

Why the "Twin Deficits" Matter

The US has long relied on foreign central banks to purchase Treasuries and agency securities, effectively funding the nation's trade deficit and federal budget deficit. As the global appetite for USD-denominated assets flattens while other currencies grow, the sustainability of these "twin deficits" comes into focus.

The Broadened Horizon

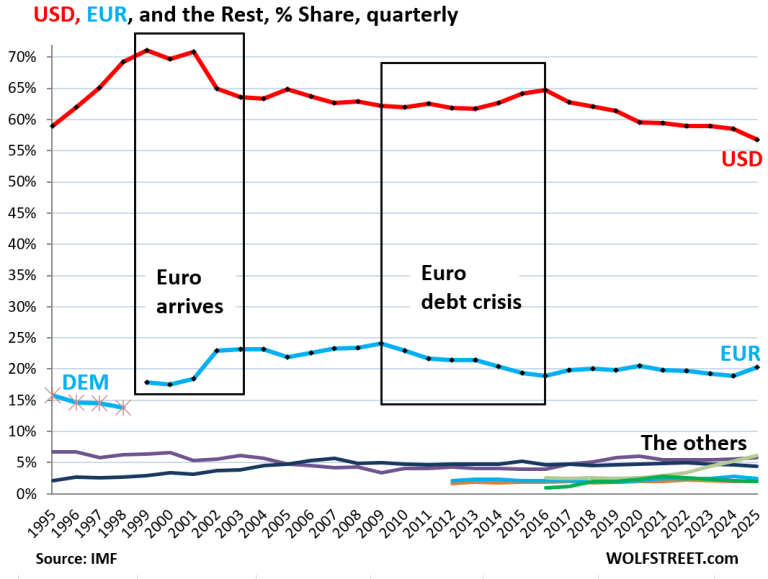

While the Euro remains the second-largest reserve currency at roughly 20%, the real story lies in the "zigzag" downward trend of the dollar toward the 50% threshold. This structural shift suggests a move toward a more fragmented, multipolar financial system where traditional "top dog" currencies must compete with a wider array of assets and commodities.

#GlobalEconomy #ForexReserves #USDTrends #CentralBanks # #EconomicAnalysis