Every few months, the crypto market finds a new narrative. Some tokens rise purely on noise, hype, and speculative momentum, while others gradually move toward a place where their real value is proven through utility, infrastructure, and adoption. Sign Protocol currently appears to be one of those projects that deserves a more serious question: is this just another market story, or is it actually building a place for itself inside state-level and institutional digital systems?

At its core, Sign Protocol’s idea is fairly simple: make trust programmable through blockchain-based attestations. In other words, an identity, credential, record, or transaction-related claim can be cryptographically verified without relying every time on a centralized middleman. According to Sign’s MiCA whitepaper, the SIGN token plays a utility role within this ecosystem, while the protocol itself aims to build a digital trust layer through verification services and decentralized attestations.

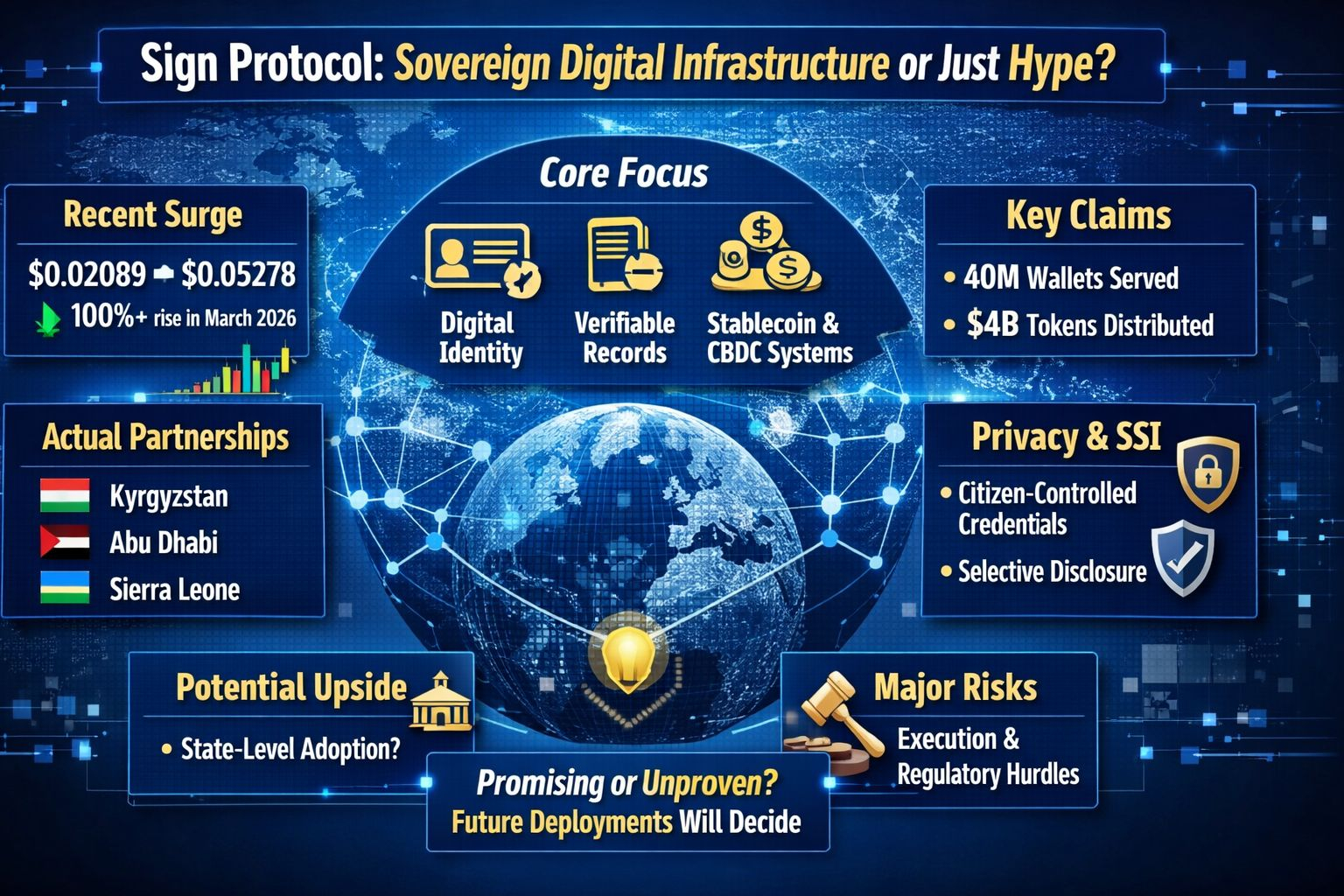

However, one important correction is necessary based on updated data. Earlier, a claim circulated that Sign had distributed “4 billion attestations,” but that does not appear to be accurate. According to the official MiCA whitepaper, in 2024 Sign processed more than 6 million attestations, while more than $4 billion worth of tokens were distributed to over 40 million wallets. So the “4 billion” figure refers to token distribution value, not the number of attestations. That distinction matters, because the wrong metric can easily inflate the perceived scale of a project.

Interest around Sign intensified in March 2026 when a March 7 report from Chainwire stated that $SIGN moved from roughly $0.02089 to $0.05278 within a week, despite weakness in the broader market. The same report suggested that the market was not just pricing the token itself, but also Sign Global’s broader vision of national-scale digital infrastructure, resilient records, and state-linked financial rails. Price action alone is never proof of adoption, but it does show that the market has started to take the narrative seriously.

Another important clarification should be made here. Earlier claims strongly referenced Germany’s national banks and partnerships in Switzerland, but in the current verified material there is no strong primary confirmation for those points. By contrast, the names that clearly surfaced were the National Bank of the Kyrgyz Republic, Blockchain Centre Abu Dhabi, and Sierra Leone’s Ministry of Communication, Technology and Innovation. A snippet from Sign’s website also highlights the Kyrgyz partnership in connection with the “Digital SOM” initiative, while the Chainwire report presents these partnerships as major developments from the last six months. At this point, the more accurate position is that Sign’s verified sovereign-facing partnerships are more clearly tied to Kyrgyzstan, Abu Dhabi, and Sierra Leone, rather than Germany or Switzerland.

The Sierra Leone case is especially worth watching, because it is not just being used as a branding example. It illustrates a real identity infrastructure problem. According to Sign’s sovereign infrastructure whitepaper, identity gaps there are so deep that although 73% of citizens have identity numbers, only 5% possess identity cards, and this contributes to 66% financial exclusion. The whitepaper also states that 60% of farmers remain excluded from phone-number-linked digital agricultural services because the foundational identity layer is weak. Sign’s argument is that unless identity infrastructure becomes reliable, digital payments, subsidy delivery, and public services cannot scale effectively.

That is why Sign is no longer positioning itself as just an “attestation protocol,” but rather as a broader digital trust and identity infrastructure layer. According to the whitepaper, this model combines Self-Sovereign Identity (SSI) principles, Verifiable Credentials, and on-chain attestations so that citizens can maintain greater control over their own data while institutions still get verification and compliance. In this framing, blockchain is not merely acting as a ledger; it is functioning as a trust substrate that provides portability, tamper resistance, and auditability.

The same document also discusses stablecoin- and CBDC-compatible public benefit systems. According to the whitepaper, their TokenTable platform is designed to help governments manage benefits, subsidies, and digital asset distribution in a programmable way, with an architecture intended to support either stablecoin rails or CBDC rails depending on the use case. The paper also outlines a phased migration model that starts with public blockchain stablecoin deployment, then moves into CBDC pilots, then bridge integration, and finally a full sovereign digital currency ecosystem. That does not mean all of these deployments are already live, but it does show that Sign’s strategic ambition is clearly aimed at state-grade financial rails.

From a privacy perspective, Sign’s pitch is also notable. The whitepaper emphasizes citizen-controlled credentials, selective disclosure, and privacy-preserving structures. The stated goal is to allow institutions to perform auditing and verification without forcing a fully centralized surveillance model. In theory, this is a strong proposition, because one of the biggest questions in modern digital governance is how to balance compliance with privacy. If a system can genuinely provide verification without unnecessary exposure of personal data, that would be a meaningful step forward for public infrastructure.

Even with all of this, skepticism remains fully justified. Sovereign-level adoption in crypto has always been messy. At the pilot stage, many things look impressive, but real execution can slow down under bureaucracy, procurement cycles, policy changes, and regulatory interpretation. In state systems, technology does not succeed merely by being innovative; it must also fit legally, win administrative buy-in, interoperate with existing systems, and survive institutional inertia. The same reality applies to Sign: the narrative is strong, the use case is serious, but the final proof will only come through large-scale production deployments and sustained usage.

From an investment perspective, Sign currently looks like a high-upside, high-friction setup. The upside is clear: if digital identity, programmable disbursements, and sovereign record systems genuinely gain traction, this could become more than just a token story — it could become an infrastructure thesis. The friction is equally real: there is a long distance between verified partnerships and actual nationwide adoption. For investors, the real task is not to react only to price candles, but to monitor whether announced relationships turn into pilots, production systems, transaction volume, and repeatable state-level use cases.

In the end, the story is simple. There is definitely hype around Sign Protocol, but there are also visible signs of substance. Official data shows that it has processed millions of attestations and facilitated billions of dollars in token distributions to tens of millions of wallets. At the same time, its public materials connect it to a larger vision involving digital identity, sovereign records, public-benefit distribution, and CBDC-adjacent infrastructure. It would be too early to call it fully proven, but it would also be inaccurate to dismiss it as an empty narrative. The most balanced way to understand Sign right now is this: a promising sovereign-infrastructure bet whose real credibility will be determined by future deployment milestones.