The thing nobody wants to admit about “modern finance” is that a lot of it still runs like a filing cabinet with an API bolted to the front.

You can dress it up with slick dashboards, QR payments, tokenization decks, central bank pilot programs and all the usual conference-stage optimism but underneath that theater you still have the same old machinery: delayed settlement, fragmented ledgers, manual exception handling, compliance teams reconciling contradictory records across five systems and public money programs that somehow still manage to lose time, visibility and trust at every step. Then we act surprised when people start talking about digital money as if the real problem is wallet design.

It isn’t.

The real problem is that the financial system still lacks clean, enforceable, auditable coordination between money, policy, identity and settlement. That’s the actual bottleneck. Not another app. Not another token. Not another chain promising to save the world at 30,000 TPS.

That’s why S.I.G.N. is more interesting than most of the stuff orbiting the “future of money” conversation.

And I say that as someone who has watched a lot of “foundational” systems die the slow death they deserved. I’ve seen enough government tech, legal workflow software and supposedly transformative infrastructure to know that most of it collapses the moment it meets procurement, auditors, supervisors, treasury operators or the first ugly edge case no one wanted to model. So I’m not easily impressed by protocol branding or glossy architecture diagrams.

But I do pay attention when something appears to be aimed at the real headache.

Because if you strip away the crypto noise, what S.I.G.N. seems to be pointing toward is not a coin-first story. It looks more like a coordination rail for sovereign digital finance. A system designed to handle the uncomfortable reality that a nation’s money infrastructure has to do contradictory things at once: protect privacy without creating blind spots, allow oversight without turning every citizen into a compliance object, support state control without becoming a dead-end silo and connect to public networks without handing monetary policy to whoever runs the loudest validator set.

That’s a serious design problem. And it’s the right one.

A lot of digital money discussions still start from the wrong premise, which is that all money should behave the same way if the underlying tech is good enough. That’s nonsense. A wholesale bank settlement is not the same thing as a welfare disbursement. A treasury reserve movement is not the same thing as a merchant payment. A cross-border remittance is not the same thing as a state payroll batch. These are different flows with different legal exposure, different audit requirements, different privacy expectations and different political consequences when they fail.

Trying to force all of that onto one transparency model is lazy. Trying to force all of it into a sealed sovereign box is just as bad.

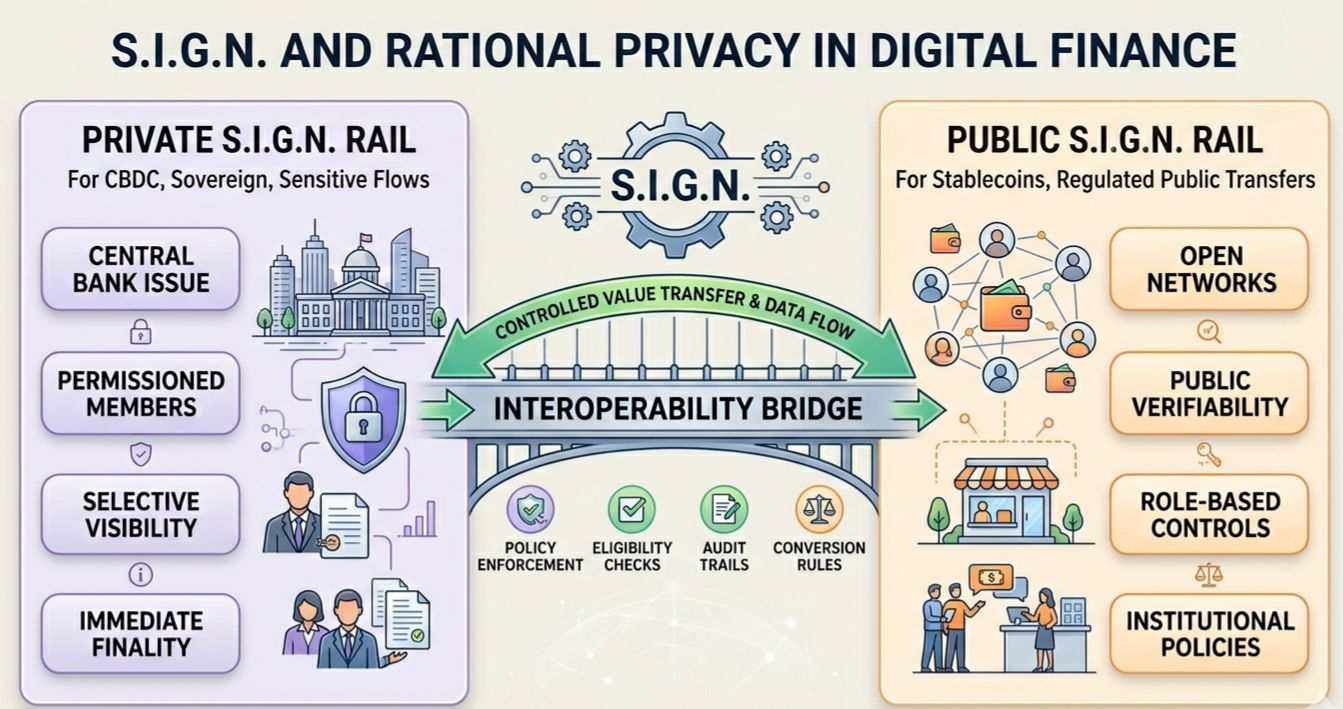

The grown-up answer is a dual-rail system.

One rail for privacy-sensitive, permissioned, state-supervised monetary activity, what most people would recognize as the serious CBDC path. Another for transparent, regulated, public-facing value transfer, the stablecoin path or at least the public settlement layer that can talk to broader digital markets and services. Not because it sounds elegant in a whitepaper but because that’s how the world actually works. Different money needs different rules.

That’s not duplication. That’s competence.

And this is where S.I.G.N., in its strongest form, starts to look useful. Not flashy. Useful.

On the public side, the design space is fairly obvious. A government or regulated consortium could run a sovereign Layer 2 if it wants more control over sequencing, governance, fee behavior, validator participation and operating policy while still anchoring to a larger public base. That’s attractive for one simple reason: it lets a state stay connected without becoming dependent. It can preserve public verifiability, ecosystem access and some degree of open composability while still controlling the environment enough to avoid building a national payment rail on top of someone else’s ideological experiment.

That matters more than people think.

Anyone who has worked around public institutions knows they do not want to wake up one morning and discover their monetary plumbing is now hostage to an offshore governance dispute, a meme-driven validator cartel or a protocol “community” that thinks national settlement risk is just an interesting Twitter thread.

States want assurances. Operators want control. Auditors want records. Supervisors want intervention rights. And no finance ministry on earth wants to explain to parliament that a core payment function broke because of “decentralized governance dynamics.”

So yes, the public rail can be useful. Very useful. But only if it is policy-aware and institutionally survivable.

The other path is more pragmatic: deploy the logic directly on an existing Layer 1 and accept the tradeoffs. Faster to launch. Easier to integrate. Better wallet compatibility. Lower initial operational burden. Also more dependency, more inherited risk and less control over the substrate. That may still be the right call in some contexts. Governments and regulated operators do not always need their own chain. Sometimes they just need controlled issuance, strong permissions, sane governance and a public record that can be verified without a three-week reconciliation exercise.

That’s the key distinction people keep missing: public does not have to mean lawless.

A well-designed public rail can still have whitelisting, role-based controls, institutional approval paths, upgrade governance and hard operational limits. It can be transparent without being stupid. It can support compliance without becoming unusable. That balance is harder than crypto people like to admit, but it’s possible.

Then there’s the private side, which is where the architecture either becomes credible or falls apart.

A real CBDC environment cannot just be “a stablecoin, but official.” That’s fantasy. If a central bank is going to issue digital sovereign money that people and institutions are expected to rely on, the system has to survive legal scrutiny, supervisory review, operational stress, identity constraints, privacy demands and the very boring but very real fact that government systems are full of exceptions, overrides and lawful intervention requirements.

This is where the conversation gets less sexy and much more important.

A private blockchain stack, something in the orbit of a Hyperledger Fabric-style model or at least that philosophy, makes sense because it treats digital money like infrastructure instead of ideology. Controlled membership. Defined trust boundaries. Selective visibility. Governance by named institutions. Settlement finality that doesn’t require probabilistic interpretation or spiritual faith in “economic security.” That’s the kind of thing actual operators can sign off on.

And yes, it sounds boring. Good.

Boring is what survives.

If you’ve ever seen how public funds actually move through a state system, you know the real pain isn’t “lack of innovation.” It’s that nobody has one clean, shared, enforceable version of truth. A payment gets approved in one system, held in another, flagged in a third, manually reconciled in a fourth, and then six months later someone is trying to reconstruct who authorized what and under which policy rule because an auditor found an exception buried in a batch file.

That’s not a technology problem in the abstract. That’s a systems design failure.

A serious CBDC stack fixes that by treating policy and traceability as first-class components of the rail. Not as an afterthought. Not as “we’ll build the compliance layer later.” Right there in the plumbing.

That means structured identity. Controlled issuance. Immediate finality once a transfer is committed. Clean token handling. Reliable peer-to-peer transaction negotiation. Governance over who runs nodes, who can intervene, who can review, who can see what and under what legal conditions. In plain English: a system built to survive contact with treasury operators, not just protocol tourists.

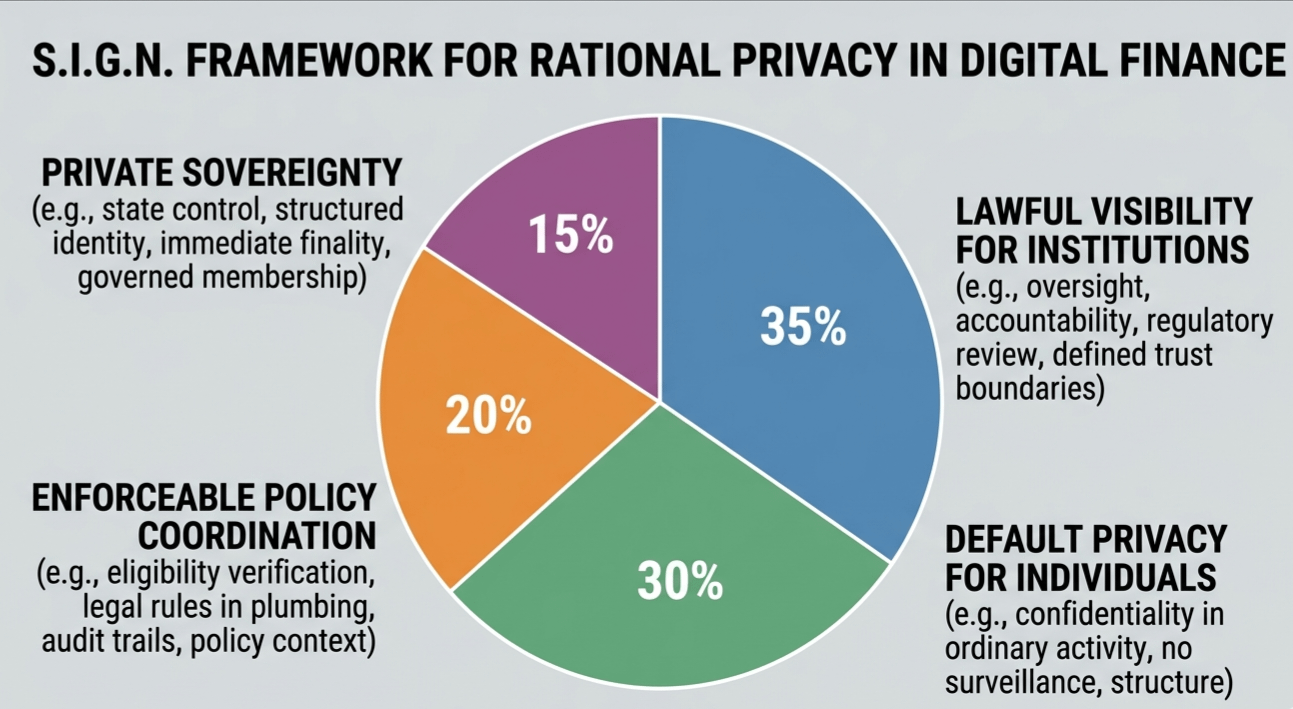

And that brings me to the part I think matters most: rational privacy.

This is where most digital money conversations still become unserious. One side wants total transparency, as if every citizen transaction should become a public monument to compliance. The other side wants absolute opacity, as if a sovereign monetary system can function with no lawful oversight, no review rights and no supervisory visibility. Both positions are childish.

A functional system needs privacy by default for ordinary activity and lawful visibility where institutional accountability requires it. That’s the right balance. Not surveillance theater. Not darkness. Structure.

That’s why a design with separate operational domains or namespaces is actually smart. One environment for wholesale CBDC activity. Another for retail-facing CBDC. Another for supervisory and regulatory functions. Maybe more, depending on the jurisdiction and use case. The point is not to make the architecture look sophisticated. The point is to reflect reality.

Because reality is messy.

An interbank liquidity transfer should not behave like a citizen benefit payment. A state procurement settlement should not expose the same metadata as a grocery purchase. A regulator should be able to perform lawful review without blowing open the entire privacy model for everyone else. Different classes of money movement need different permissions, different visibility and different evidence trails.

That’s not overengineering. That’s what happens when adults are in the room.

And then we get to the bridge layer, which is where this stops being an isolated CBDC thought experiment and starts becoming economically relevant.

If S.I.G.N. can actually help connect private sovereign money environments with regulated public stablecoin rails, that’s where the utility compounds.

Because no matter how much central banks might like to imagine otherwise, money is not going to live on one pristine, nationally contained system forever. Governments will need to move value between internal controlled environments and broader public networks. Institutions will need to settle across trust boundaries. Citizens and merchants will operate across both worlds whether policymakers like it or not.

So the bridge matters. A lot.

But not the way crypto usually does bridges, which is to say recklessly.

A serious bridge between CBDC rails and public regulated stablecoin rails cannot be some “lock, mint, trust us” mechanism wrapped in governance cosplay. It has to enforce eligibility checks, policy logic, conversion constraints, rate controls, approval rules, emergency pause authority and full evidence logging tied to who approved the transfer, which rules were active and why the movement was lawful in the first place.

That last part is where most systems still fail.

They record that a transfer happened. Fine. But they don’t preserve the policy context that made it permissible. For governments and regulated institutions, that’s not enough. They don’t just need transaction history. They need decision history. They need to know what rule fired, what authority approved, what threshold applied, what exception path was triggered and whether the process complied with the legal frame it was supposed to operate under.

That is not a minor feature. That’s the difference between infrastructure and theater.

And once you think about it that way, the practical use cases become a lot more concrete.

Government-to-person disbursement is the obvious one. Benefits, pensions, emergency relief, subsidy programs, targeted support. Right now, in many jurisdictions, those flows are still a bureaucratic obstacle course. Identity checks are fragmented. Eligibility review is inconsistent. Settlement paths are clunky. Leakage happens. Delays happen. Appeals happen. Then everyone pretends this is just the unavoidable cost of public administration.

It isn’t.

A clean digital money stack could verify eligibility, assign the correct rail, issue the disbursement, settle it and preserve a full audit trail without making the process even more punitive for the person receiving the funds. That’s not some futuristic use case. That’s just competent state infrastructure.

And it matters because the state could choose the mode based on the policy objective. Privacy-sensitive citizen support? Use the private CBDC path. Public accountability for a specific class of disbursement or grant flow? Use a more transparent regulated public rail. The system should not force one answer for every program. It should let policymakers express intent in the actual transaction design.

That’s real utility.

Merchant acceptance is another area where people consistently underestimate the challenge. Everyone loves to talk about “payments adoption” until they encounter the actual things merchants care about: settlement certainty, refund logic, reconciliation, dispute handling, device compatibility, fee behavior, customer support and what happens when the internet is slow and the cashier has a line out the door.

This is why so many crypto payment products still feel unserious. They solve transfer mechanics and ignore operational reality.

But operational reality is the product.

If sovereign digital money is ever going to matter outside policy circles and fintech decks, it has to work in the places where people actually buy things. That means sane merchant tooling, sane acquirer integration, sane PSP workflows and a system that does not make every checkout interaction feel like a legal experiment.

And then there’s cross-border movement, which remains one of the most embarrassing failures in modern financial infrastructure.

The internet can move a video call across continents in real time, but moving money between jurisdictions still often feels like mailing a notarized fax through three correspondent banks and hoping nobody asks too many questions on day four. Fees are bad. Delays are bad. Traceability is inconsistent. Reporting is fragmented. Settlement is too often built on trust chains that belong to another era.

So yes, a system that can connect private sovereign rails, public regulated rails, structured policy controls and modern messaging standards starts to become very interesting here.

Not because it magically solves geopolitics or capital controls or FX compliance. It doesn’t. Nothing does. But because it creates better plumbing. Cleaner state transitions. Better traceability. Better control over how systems talk to each other. Less ritualized nonsense.

That’s the opportunity. Not “number go up.” Not “mass adoption.” Better plumbing.

Which brings me back to Sign Coin itself.

The strongest case for Sign is not that it becomes the consumer-facing token everyone holds in a hot wallet while influencers post thread emojis about the future of civilization. That’s the weak thesis. The forgettable one. The one that dies the minute attention moves elsewhere.

The stronger case is that Sign becomes part of the coordination layer underneath sovereign-compatible digital finance, the part that helps systems issue, route, verify, govern and bridge digital value across different trust environments without losing the policy, identity and audit context that makes the whole thing legally and institutionally usable.

That is a much harder role to earn. But it’s also a much more defensible one.

Speculative assets come and go. Infrastructure that removes friction from ugly institutional workflows tends to stick. Especially if it solves a problem that everyone has and nobody enjoys talking about.

And the problem here is obvious if you’ve spent any time around public systems: how do you move digital value in a way that preserves privacy where it should, visibility where it must, policy where it matters and usability where people actually live?

That’s the real question.

If S.I.G.N. is genuinely aimed at that question, then it’s playing in a category that most crypto projects never get close to. Not because it sounds more sophisticated. Because it sounds more useful.

It’s not crypto.

It’s infrastructure.

And that’s exactly why it’s worth watching.

@SignOfficial #SignDigitalSovereignInfra $SIGN