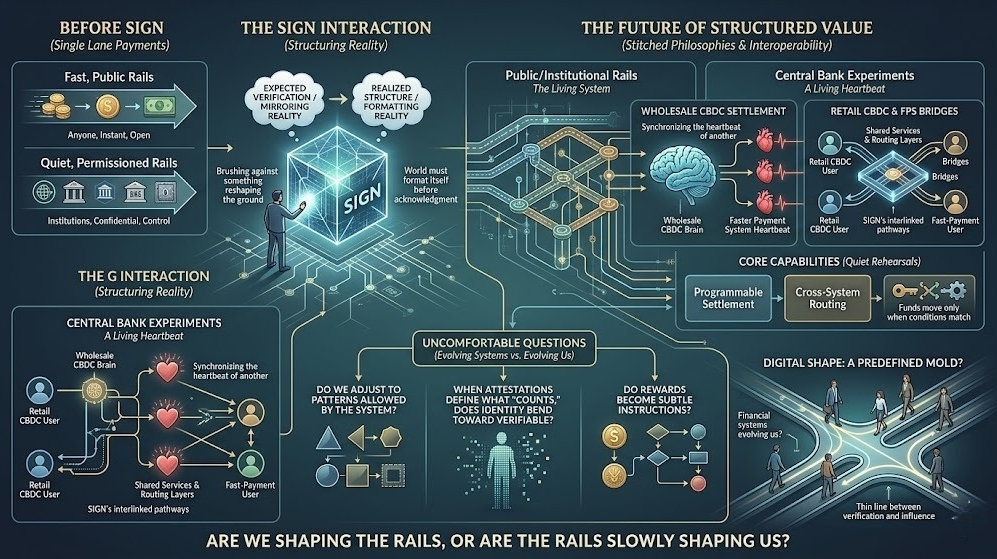

When I think back to the moment I first interacted with SIGN, it didn’t feel like discovering a new tool. It felt like brushing against something that was quietly reshaping the ground beneath my feet. I had gone in expecting verification, something simple, something reflective. But the deeper I moved, the more I realized SIGN wasn’t mirroring reality at all — it was structuring it. Almost like the world had to format itself before being acknowledged.

What struck me most was how money behaved inside this architecture. Before SIGN, I saw payments as a single lane. After SIGN, I began to see multiple, layered rails — the fast, open public ones where anyone can move value instantly, and the quieter, permissioned ones built for institutions that need confidentiality and control. Watching both interact felt like witnessing two different philosophies stitched into one living system.

And then I learned something that deepened this feeling even more: central banks across the world are running experiments of their own, trying to understand how these new rails could connect with their national payment systems. Some are testing how a wholesale CBDC could settle the obligations of faster payment systems — almost like using one brain to synchronize the heartbeat of another. Others are exploring bridges where retail CBDC users and fast-payment users can send value to each other seamlessly, using shared services and routing layers that feel strangely similar to SIGN’s own interlinked pathways.

That was the moment I realized these experiments weren’t just technical trials. They were quiet rehearsals for a future where systems like SIGN might sit at the center of national and global value flows — not replacing institutions, but teaching them how to speak the same structured language. Programmable settlement. Cross-system routing. Funds that move only when conditions on both sides match. It is intricate, almost delicate, but it works. At least in controlled environments. And that’s enough to hint at how powerful it could become.

Somewhere between these public and private rails, these wholesale and retail bridges, I started asking myself uncomfortable questions. If value moves only through the patterns allowed by a system, do we eventually adjust ourselves to those patterns? When attestations start defining what counts, does identity slowly bend toward what is verifiable? Even rewards begin to feel less like incentives and more like subtle instructions.

And when I look at CBDCs connecting through FPS bridges, and SIGN helping shape structured claims and programmable truth, the line between verification and influence becomes thinner than ever. It makes me wonder whether financial systems are evolving… or whether they are quietly evolving us.

Sometimes I feel we’re not just building digital money or digital trust. We’re building digital shape. A predefined mold that everything — even humans — might slowly learn to fit.

So here is the question I keep returning to, and I leave it with you now:

As our payment systems, identities, and truths become increasingly structured and interoperable… are we shaping the rails, or are the rails slowly shaping us?

@SignOfficial #SignDigitalSovereignInfra $SIGN