I’ll be honest, when I first came across Sign’s CBDC architecture, I thought I had it figured out within minutes. It looked like the usual story: central banks upgrading infrastructure, commercial banks running nodes, faster settlements, cleaner rails. You know, the kind of thing that sounds important but feels distant from everyday life. I almost moved on.

But something kept pulling me back. Maybe it was the way the system was described, or maybe I just had that feeling that I was missing the point. So I read it again, slower this time. And yeah, that’s when it clicked for me—this isn’t just a banking upgrade. It’s trying to redraw the entire structure of how money reaches people.

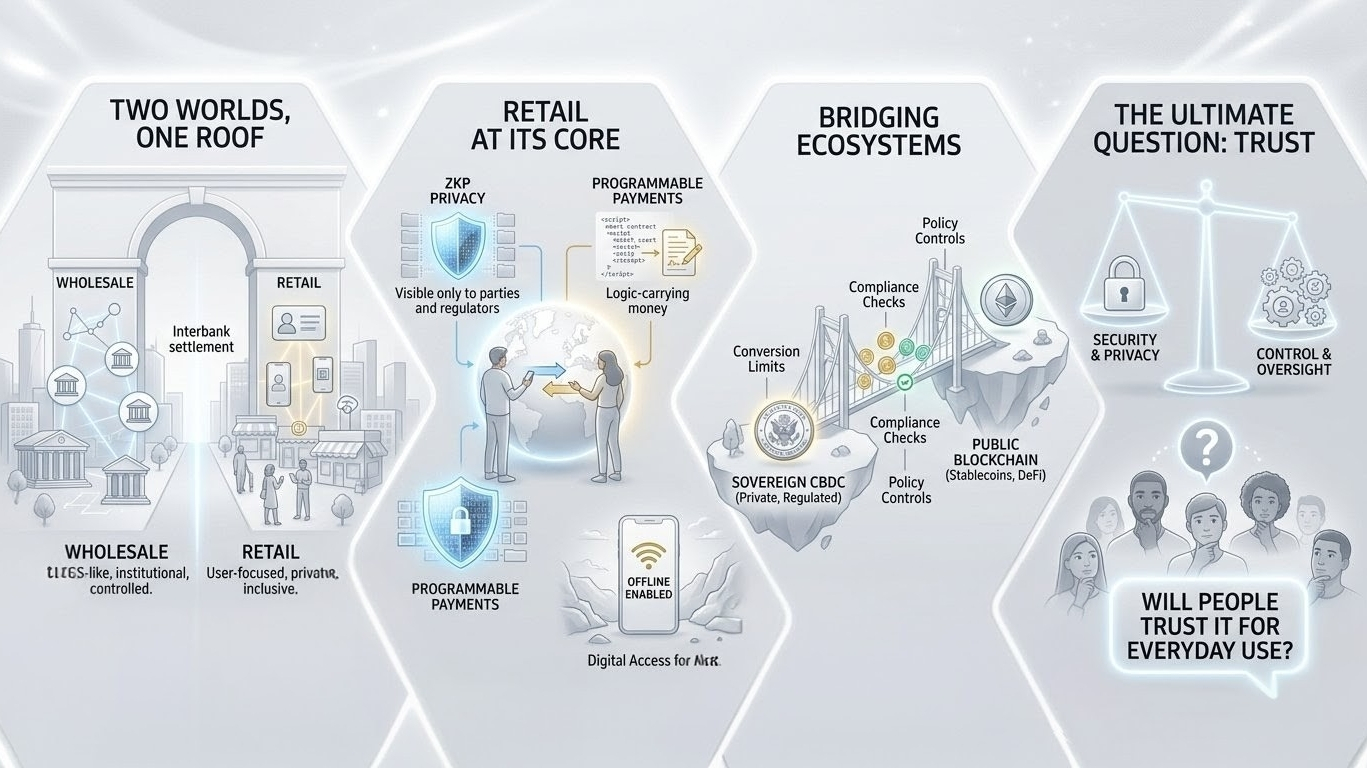

At first glance, the wholesale side feels familiar. Central banks control the ordering layer, commercial banks validate transactions, and the whole thing resembles a more modern version of interbank settlement systems. Nothing too radical there. If you’ve followed financial infrastructure, it almost feels expected. Cleaner, faster, more controlled.

But then I noticed something that completely shifted how I was thinking about it: the separation between wholesale and retail namespaces.

That one detail changed everything for me.

Instead of treating everyday users as some downstream layer that eventually plugs into the system, Sign builds them in from the start. There’s a wholesale environment for banks doing their thing, and then there’s a retail environment designed specifically for people and businesses. Not as an afterthought. Not as an extension. As a core part of the architecture.

And the retail side? It’s not just “smaller payments,” which is what I initially assumed.

It’s actually a completely different experience.

They’re talking about zero-knowledge proofs for privacy, which basically means transaction details aren’t just sitting there exposed for anyone with access to the system. Only the sender, receiver, and the right regulators can see what’s going on. That’s a big deal, especially in a world where people are increasingly skeptical about financial surveillance.

Then there’s programmability. Payments that can carry logic. Money that can behave differently depending on rules or conditions. I used to think this was just a buzzword, but the more I think about it, the more I realize how powerful—and potentially risky—it could be.

And yeah, the offline capability stood out to me too. That’s one of those features that sounds minor until you think about where it matters most. Regions with poor connectivity, underserved populations, places where traditional banking hasn’t fully reached. Suddenly, this isn’t just about innovation—it’s about access.

That’s when I realized something important: this system isn’t just trying to make banks better at talking to each other. It’s trying to make sovereign money actually reach people in a completely different way.

And that’s a much bigger ambition.

What really got me thinking, though, is how the architecture keeps everything under one roof. You’ve got this single national infrastructure supporting two very different worlds. On one side, you have something that looks like RTGS—transparent, controlled, institutional. On the other, you have a user-focused layer built around privacy, usability, and inclusion.

Same system. Different rules. Different visibility. Different assumptions.

That’s not a small design choice. That’s a philosophical one.

Because if you think about how people actually experience money, it’s not through settlement systems or bank reserves. It’s through daily interactions. Can I send money easily? Is it private? Does it work when I need it? Am I being watched? Can I even access it in the first place?

Those are the real questions. And for once, it feels like a system is at least محاولة—trying—to answer them directly.

But then there’s another layer that made me pause.

The bridge to public blockchain environments.

This part is fascinating and honestly a bit unsettling at the same time. The idea that you can move between a private, sovereign-controlled CBDC system and a public-chain stablecoin ecosystem… that opens up a lot of possibilities. It connects two worlds that have mostly been separate: regulated national money and open digital assets.

On paper, it sounds like the best of both sides. Stability and control on one end, openness and flexibility on the other. But in reality? That’s where things start to get complicated.

Because now you’re dealing with conversion limits, compliance checks, policy controls—all layered on top of user movement between systems. And I can’t help but wonder how smooth that actually feels in practice. Does it empower users, or does it quietly add friction and oversight?

That’s where my hesitation comes in.

The architecture is clean. Almost too clean.

Everything fits together nicely: privacy, programmability, inclusion, control, interoperability. But real systems don’t live in whitepapers. They live in messy environments full of trade-offs, political pressures, technical limitations, and human behavior.

Can you really offer strong privacy while maintaining regulatory oversight? Can offline functionality scale without introducing risk? Can you include everyone without making the system too complex to manage? And what happens when governments start leaning harder into the control side of programmable money?

I keep going back and forth on it.

Part of me thinks this is exactly where things are heading. That money, like everything else, is becoming structured, layered, and deeply integrated into digital systems. And if that’s the case, then something like this makes sense. It’s not just evolution—it’s inevitable.

But another part of me wonders if this is one of those ideas that works beautifully in theory and struggles the moment it touches reality.

Because at the end of the day, this isn’t just about technology. It’s about trust.

And that’s the question I keep coming back to: if a system can do everything—protect privacy, enforce rules, operate offline, connect to public chains—who ultimately decides how it’s used, and will people actually trust it enough to let it become their everyday money?