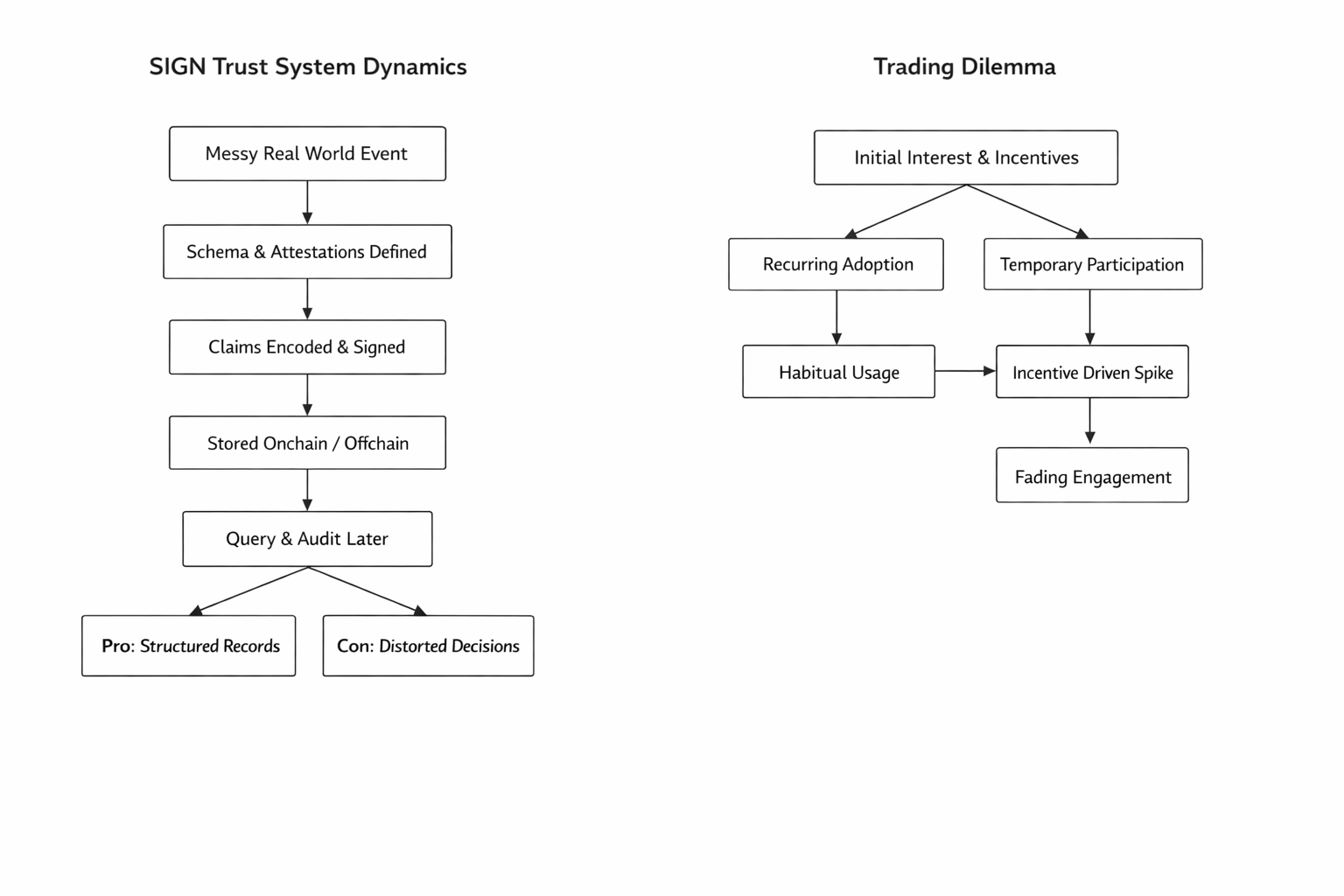

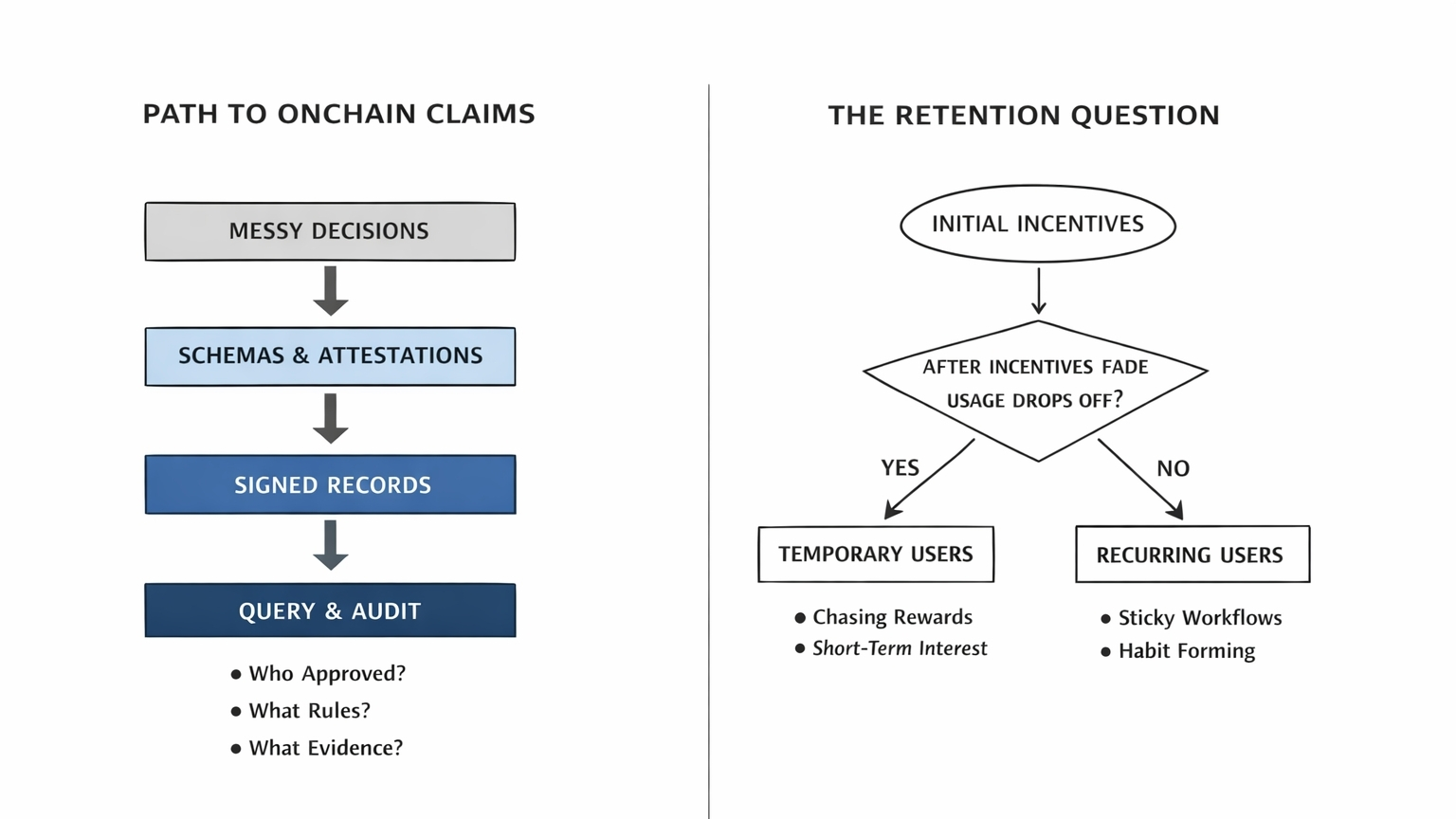

I remember looking at a clean onchain dashboard one night and getting irritated instead of impressed. Everything looked legible. Claims were structured, searchable, easy to verify later. Traders around me were treating that like proof the hard part was already done. But I kept thinking about what happens before the query. Before the audit. Before the neat evidence trail. With Sign, that is still the part I cannot stop staring at.  What makes this project interesting to me is also what makes it dangerous to read too quickly. Sign is built around schemas and attestations, which is a tidy way of saying it tries to turn messy claims into structured, signed records that can be stored onchain, offchain, or in a hybrid model, then queried later through SignScan’s REST and GraphQL APIs. The docs are pretty clear about the ambition here. This is meant to answer ugly real world questions like who approved something, under which authority, under what rules, and with what evidence. That is useful. Very useful. But here’s the tradeoff people underplay. The easier you make claims to query later, the more pressure there is to shape decisions earlier so they fit the system cleanly. That is where distortion can begin. As a trader, I do not care about that in an abstract governance seminar way. I care because it affects what kind of usage actually repeats. Today SIGN is trading around $0.0323 to $0.0327, with a market cap near $53 million, about 1.64 billion tokens circulating out of a 10 billion max supply, and roughly $32 million to $39 million in 24 hour volume depending on the tracker snapshot. Fully diluted valuation is about $328 million. That gap matters. The market is not pricing Sign like a dead microcap, but it is also not pricing the full future supply as if demand is already proven. Price is still roughly 75 percent below the all time high of $0.1311. So the market is telling you two things at once. There is interest, and there is doubt. That is usually where the best work starts. Now here’s the thing that keeps my thesis from turning into a comfortable bull post. Structured trust systems do not just record reality. They can quietly influence it. If a government program, capital distribution system, or compliance workflow knows it will later be judged by what can be queried, operators start optimizing for what is easy to encode. Edge cases get squeezed. Human judgment gets translated into schema fields. Exceptions become expensive. In Sign’s own design, schemas define the format, attestations follow them, and hooks can whitelist attesters, charge fees, or reject actions by reverting the whole transaction. That is efficient. It is also a form of pre-filtering reality. Think of it like accounting rules. They help you inspect the business later, but they also shape how people behave before quarter end. That is why the Retention Problem matters so much here. For Sign, retention is not just daily active wallets or a nice spike in search traffic. It is whether institutions, apps, and distribution programs keep coming back to the same trust rails because they actually reduce recurring friction. If usage does not repeat, then all this beautiful structure becomes rented attention with paperwork attached. The recent Orange Basic Income program is a good example of the tension. Sign launched a 100 million SIGN OBI program, with Season 1 running from March 20 to June 18, 2026, to reward self custody and staking behavior. I get the logic. Move supply off exchanges, encourage longer holding, reduce reflexive sell pressure. But incentives can manufacture participation faster than they manufacture habit. A user who stakes because rewards are attractive is not the same as a system operator who cannot leave because the workflow is genuinely useful. Traders need to know that difference. The realistic bull case is still there, and I do think it deserves numbers instead of hand waving. If Sign can turn even a small part of its evidence layer pitch into sticky operational demand, today’s roughly $53 million market cap and roughly $328 million FDV can still look early relative to what regulated identity, capital distribution, and verification infrastructure could justify. The current volume to market cap ratio is high enough to show active interest, not total apathy, and the project does have a product story traders can actually explain without making things up. Queryable attestations, hybrid storage, programmable hooks, and audit friendly records are not fake problems. They are real. If the market starts to believe those rails are becoming default infrastructure for repeat workflows, re-rating can happen fast from a base this small. But the bear case is stronger than a lot of people want to admit. Supply is the obvious one. Tokenomist shows the next SIGN unlock is scheduled for April 28, 2026, and the vesting schedule extends into 2030. That means any retention story has to fight dilution in real time. And the project’s own strengths can become a weakness if adoption stays narrow. A system built to make claims queryable across chains and storage layers can still fail to create durable user dependence. Clean architecture does not guarantee repeat economic behavior. I have seen traders confuse explainability with demand before. They are not the same thing. One helps you understand the machine. The other tells you whether anyone needs to keep using it. So what would change my mind either way? On the bullish side, I want to see repeated usage that survives after incentives cool off. Not one campaign. Not one listing rumor. Not one burst of volume. I want evidence that teams or institutions are building workflows they do not want to abandon because Sign makes compliance, eligibility, or distribution easier every single week. On the bearish side, I am watching for the opposite. More structured records, more announcements, more incentives, but no real habit loop underneath. That would tell me the project is getting better at documenting value than creating it. If you are trading SIGN here, do not just ask whether the claims can be queried later. Ask what behavior gets bent earlier so those claims look clean, and ask whether anyone keeps showing up when the reward schedule matters less than the workflow. That is the whole trade to me. Not whether Sign can explain decisions after the fact, but whether it can become part of decisions people cannot stop repeating.

What makes this project interesting to me is also what makes it dangerous to read too quickly. Sign is built around schemas and attestations, which is a tidy way of saying it tries to turn messy claims into structured, signed records that can be stored onchain, offchain, or in a hybrid model, then queried later through SignScan’s REST and GraphQL APIs. The docs are pretty clear about the ambition here. This is meant to answer ugly real world questions like who approved something, under which authority, under what rules, and with what evidence. That is useful. Very useful. But here’s the tradeoff people underplay. The easier you make claims to query later, the more pressure there is to shape decisions earlier so they fit the system cleanly. That is where distortion can begin. As a trader, I do not care about that in an abstract governance seminar way. I care because it affects what kind of usage actually repeats. Today SIGN is trading around $0.0323 to $0.0327, with a market cap near $53 million, about 1.64 billion tokens circulating out of a 10 billion max supply, and roughly $32 million to $39 million in 24 hour volume depending on the tracker snapshot. Fully diluted valuation is about $328 million. That gap matters. The market is not pricing Sign like a dead microcap, but it is also not pricing the full future supply as if demand is already proven. Price is still roughly 75 percent below the all time high of $0.1311. So the market is telling you two things at once. There is interest, and there is doubt. That is usually where the best work starts. Now here’s the thing that keeps my thesis from turning into a comfortable bull post. Structured trust systems do not just record reality. They can quietly influence it. If a government program, capital distribution system, or compliance workflow knows it will later be judged by what can be queried, operators start optimizing for what is easy to encode. Edge cases get squeezed. Human judgment gets translated into schema fields. Exceptions become expensive. In Sign’s own design, schemas define the format, attestations follow them, and hooks can whitelist attesters, charge fees, or reject actions by reverting the whole transaction. That is efficient. It is also a form of pre-filtering reality. Think of it like accounting rules. They help you inspect the business later, but they also shape how people behave before quarter end. That is why the Retention Problem matters so much here. For Sign, retention is not just daily active wallets or a nice spike in search traffic. It is whether institutions, apps, and distribution programs keep coming back to the same trust rails because they actually reduce recurring friction. If usage does not repeat, then all this beautiful structure becomes rented attention with paperwork attached. The recent Orange Basic Income program is a good example of the tension. Sign launched a 100 million SIGN OBI program, with Season 1 running from March 20 to June 18, 2026, to reward self custody and staking behavior. I get the logic. Move supply off exchanges, encourage longer holding, reduce reflexive sell pressure. But incentives can manufacture participation faster than they manufacture habit. A user who stakes because rewards are attractive is not the same as a system operator who cannot leave because the workflow is genuinely useful. Traders need to know that difference. The realistic bull case is still there, and I do think it deserves numbers instead of hand waving. If Sign can turn even a small part of its evidence layer pitch into sticky operational demand, today’s roughly $53 million market cap and roughly $328 million FDV can still look early relative to what regulated identity, capital distribution, and verification infrastructure could justify. The current volume to market cap ratio is high enough to show active interest, not total apathy, and the project does have a product story traders can actually explain without making things up. Queryable attestations, hybrid storage, programmable hooks, and audit friendly records are not fake problems. They are real. If the market starts to believe those rails are becoming default infrastructure for repeat workflows, re-rating can happen fast from a base this small. But the bear case is stronger than a lot of people want to admit. Supply is the obvious one. Tokenomist shows the next SIGN unlock is scheduled for April 28, 2026, and the vesting schedule extends into 2030. That means any retention story has to fight dilution in real time. And the project’s own strengths can become a weakness if adoption stays narrow. A system built to make claims queryable across chains and storage layers can still fail to create durable user dependence. Clean architecture does not guarantee repeat economic behavior. I have seen traders confuse explainability with demand before. They are not the same thing. One helps you understand the machine. The other tells you whether anyone needs to keep using it. So what would change my mind either way? On the bullish side, I want to see repeated usage that survives after incentives cool off. Not one campaign. Not one listing rumor. Not one burst of volume. I want evidence that teams or institutions are building workflows they do not want to abandon because Sign makes compliance, eligibility, or distribution easier every single week. On the bearish side, I am watching for the opposite. More structured records, more announcements, more incentives, but no real habit loop underneath. That would tell me the project is getting better at documenting value than creating it. If you are trading SIGN here, do not just ask whether the claims can be queried later. Ask what behavior gets bent earlier so those claims look clean, and ask whether anyone keeps showing up when the reward schedule matters less than the workflow. That is the whole trade to me. Not whether Sign can explain decisions after the fact, but whether it can become part of decisions people cannot stop repeating.

Artikel

What Sign Makes Easy to Query Later Can Start Distorting Decisions Much Earlier Than People Admit

Haftungsausschluss: Die hier bereitgestellten Informationen enthalten Meinungen Dritter und/oder gesponserte Inhalte und stellen keine Finanzberatung dar. Siehe AGB.