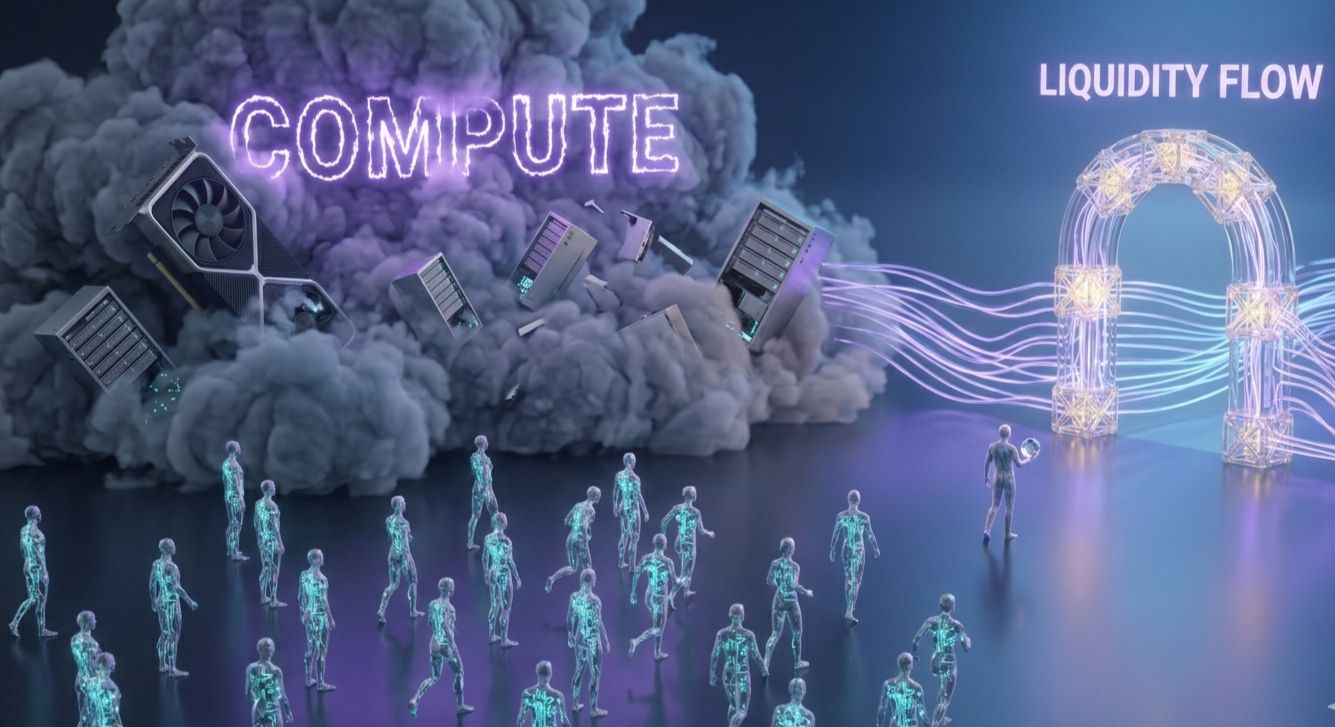

Markets rarely understand new technologies on first contact. They compress complexity into whatever metric feels easiest to compare. In one cycle, it was transactions per second. In another, it was total value locked. With artificial intelligence now intersecting crypto, the simplification has shifted again toward compute. Faster inference, larger models, cheaper GPUs. The assumption is almost mechanical: if AI is expensive, then the winning infrastructure will be the one that makes it cheaper.

But cost is not always the true bottleneck. Sometimes the deeper constraint lies in how economic activity is coordinated once the technology exists. Not how fast a model runs, but how value moves between those who produce data, those who refine it into models, and those who deploy it through agents. In that sense, the hidden layer isn’t compute it’s liquidity flow.

This is where projects like OpenLedger begin to look different, though the market may not yet be framing them that way.

What the market thinks OpenLedger is remains relatively straightforward: an “AI blockchain,” another attempt to merge decentralized infrastructure with machine intelligence. In this framing, it competes implicitly with other chains on performance how efficiently it can support AI workloads, how cheaply it can facilitate inference, how scalable its architecture might become.

But that interpretation risks missing the more interesting possibility. OpenLedger may not primarily be an AI execution layer. It may be attempting to function as a liquidity layer for intelligence itself.

To understand this, it helps to step outside crypto for a moment. In traditional finance, markets don’t just exist to hold assets; they exist to route capital. Liquidity determines whether an asset is useful, whether it can be priced continuously, whether it can attract participation. Without liquidity, even valuable things remain economically inert.

Now apply that lens to AI. Data, models, and agents are all productive assets, but they are fragmented. Data is siloed, models are proprietary, and agents operate within narrow domains. There is no unified marketplace where these components can be continuously priced, exchanged, and recombined. As a result, much of the potential value remains locked not because the technology is insufficient, but because the economic pathways are incomplete.

OpenLedger, at least conceptually, appears to be addressing this gap. Not by building the best model or the fastest inference engine, but by enabling flows between participants. Data contributors can be compensated, model builders can access inputs without exclusive ownership, and agents can execute tasks while routing value back through the system. The emphasis shifts from production to circulation.

If that framing holds, then the token attached to such a system is unlikely to be a simple “utility token” in the usual sense. It may instead function as a unit of coordination a mechanism for pricing interactions across a network where trust is minimal and attribution is complex. The token could be less about paying for compute and more about legitimizing economic relationships between actors who would otherwise have no shared accounting layer.

This is where enterprise considerations begin to matter. For real-world adoption, questions of auditability, compliance, and accountability become unavoidable. Who is responsible when an AI agent produces a harmful output? How is data provenance verified? How are payments distributed in a way that can be inspected and trusted? A system that merely facilitates transactions is insufficient; it must also provide a credible record of how those transactions occurred.

Yet this is precisely where friction emerges. Coordinating liquidity across heterogeneous AI components is not trivial. Data is messy, incentives are misaligned, and participants often prefer closed systems where they can capture more value. Developers may resist integrating into a shared layer if it introduces overhead or dilutes control. Even if the infrastructure exists, behavior does not automatically follow.

There is also the question of token demand. If the network successfully routes value, does that translate into sustained demand for the token itself, or does velocity undermine accumulation? Markets have repeatedly overestimated the direct linkage between usage and price, especially in systems where tokens primarily facilitate flow rather than store value.

All of this suggests that OpenLedger, if it succeeds, may not fit neatly into existing categories. It would not simply be an AI chain, nor a marketplace, nor a traditional financial layer. It would resemble something closer to an economic substrate for intelligence an attempt to make AI components behave like liquid assets within a shared system.

Whether that vision materializes remains uncertain. But the more interesting question is not whether OpenLedger can run AI efficiently. It is whether it can make intelligence economically interoperable.

And if it can, the market may eventually realize it was never about compute in the first place.

Sometimes the hardest infrastructure to see is the one that moves value, not data.