@OpenLedger $OPEN #OpenLedger The promise sounds straightforward: turn your data, your models, your AI agents into liquid assets. Put them on a blockchain, create a market, unlock value that's currently trapped or underutilized. It's the kind of pitch that makes intuitive sense until you start thinking about what actually happens when someone tries to buy what you're selling.

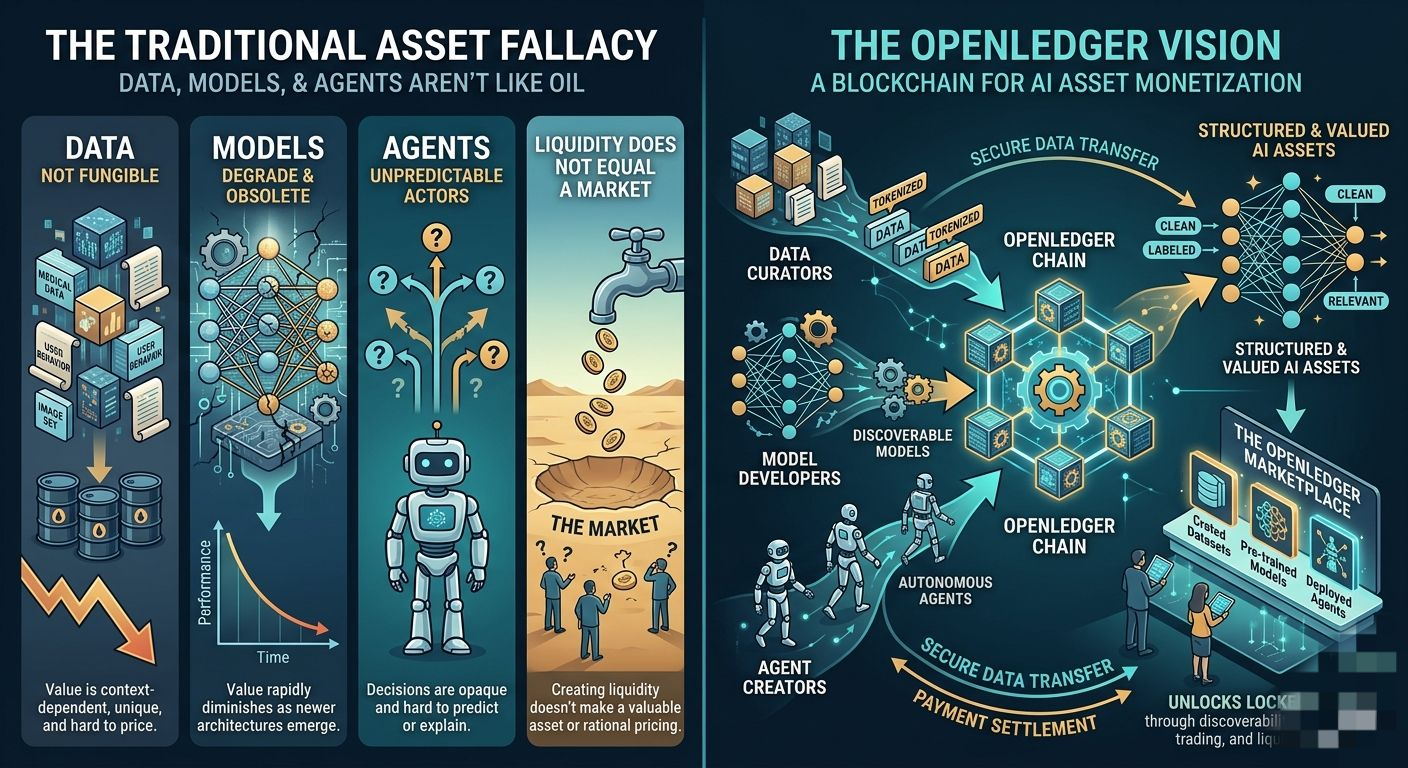

The AI industry has spent years talking about data as the new oil, models as valuable intellectual property, and agents as autonomous economic actors. The problem is that none of these things behave like traditional assets. Data isn't fungible. Models degrade. Agents make decisions you can't always predict or explain. And creating liquidity for something doesn't automatically mean that thing has a market, or that the market will price it rationally, or that anyone can actually use what they've purchased.

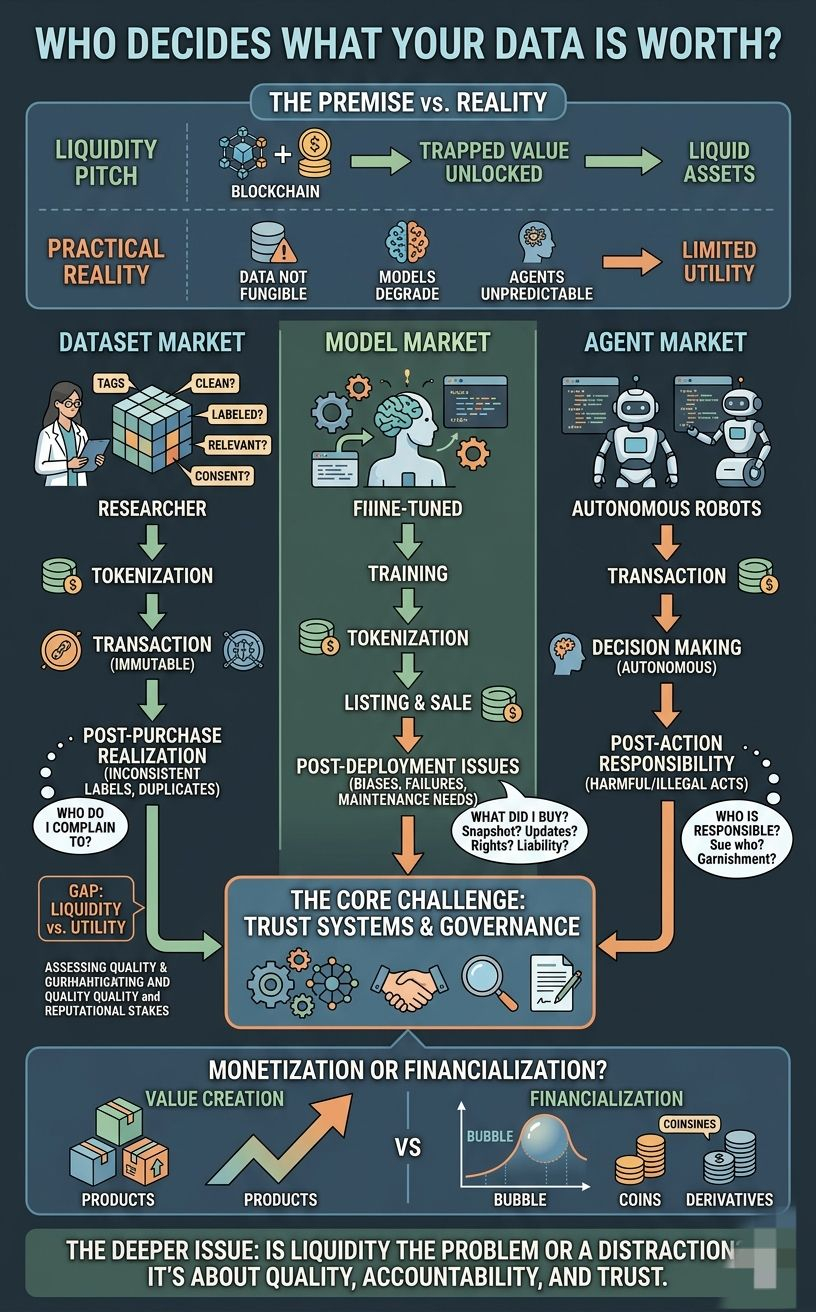

OpenLedger presents itself as infrastructure for this vision—a blockchain designed specifically for AI, meant to help people monetize data, models, and agents by making them tradable, discoverable, and liquid. The assumption is that there's value locked up in these assets and that the main problem is the lack of a proper marketplace.

But let's walk through what that marketplace might actually look like.

Imagine you're a researcher who's spent months curating a dataset. It's good data—clean, labeled, relevant to a specific domain. You want to monetize it. OpenLedger, in theory, lets you tokenize that dataset, list it, and wait for buyers. Someone purchases access. The transaction happens on-chain. Liquidity unlocked.

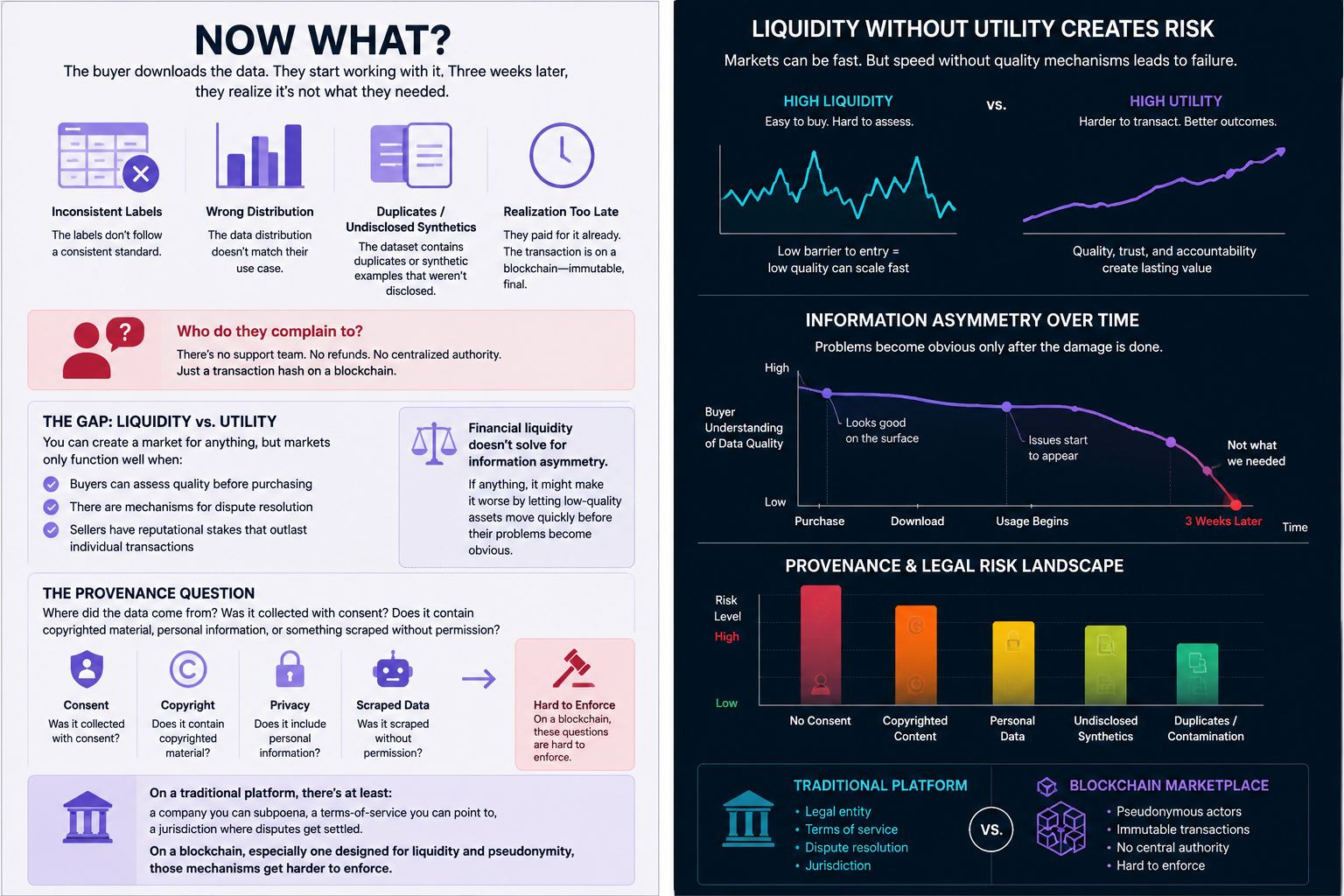

Now what?

The buyer downloads the data. They start working with it. Three weeks later, they realize it's not what they needed. Maybe the labels are inconsistent. Maybe the distribution doesn't match their use case. Maybe it's contaminated with duplicate entries or synthetic examples that weren't disclosed. They paid for it already. The transaction is on a blockchain—immutable, final.

Who do they complain to?

This is the gap between liquidity and utility. You can create a market for anything, but markets only function well when buyers can assess quality before purchasing, when there are mechanisms for dispute resolution, when sellers have reputational stakes that outlast individual transactions. Financial liquidity doesn't solve for information asymmetry. If anything, it might make it worse by letting low-quality assets move quickly before their problems become obvious.

Then there's the question of provenance. Where did the data come from? Was it collected with consent? Does it contain copyrighted material, personal information, or something scraped without permission? On a traditional platform, there's at least a company you can subpoena, a terms-of-service you can point to, a jurisdiction where disputes get settled. On a blockchain, especially one designed for liquidity and pseudonymity, those mechanisms get harder to enforce.

You could build them back in—verification layers, identity requirements, escrow systems, dispute resolution protocols. But now you're recreating the infrastructure of a traditional marketplace, just with extra steps and on-chain overhead.

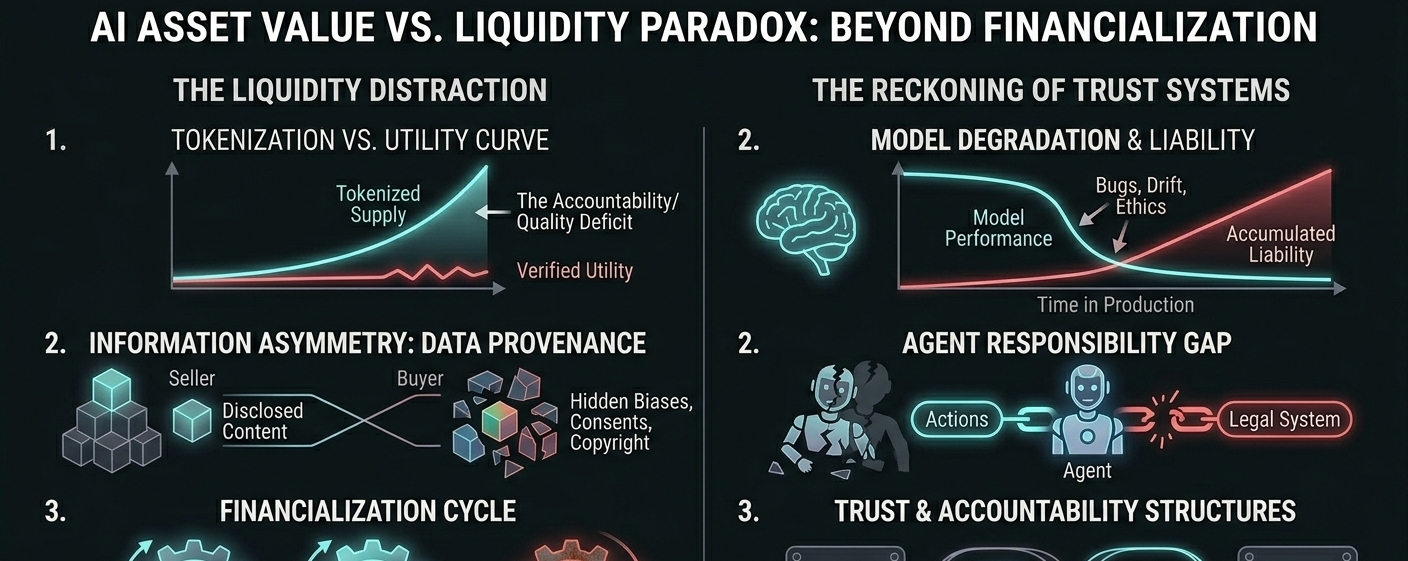

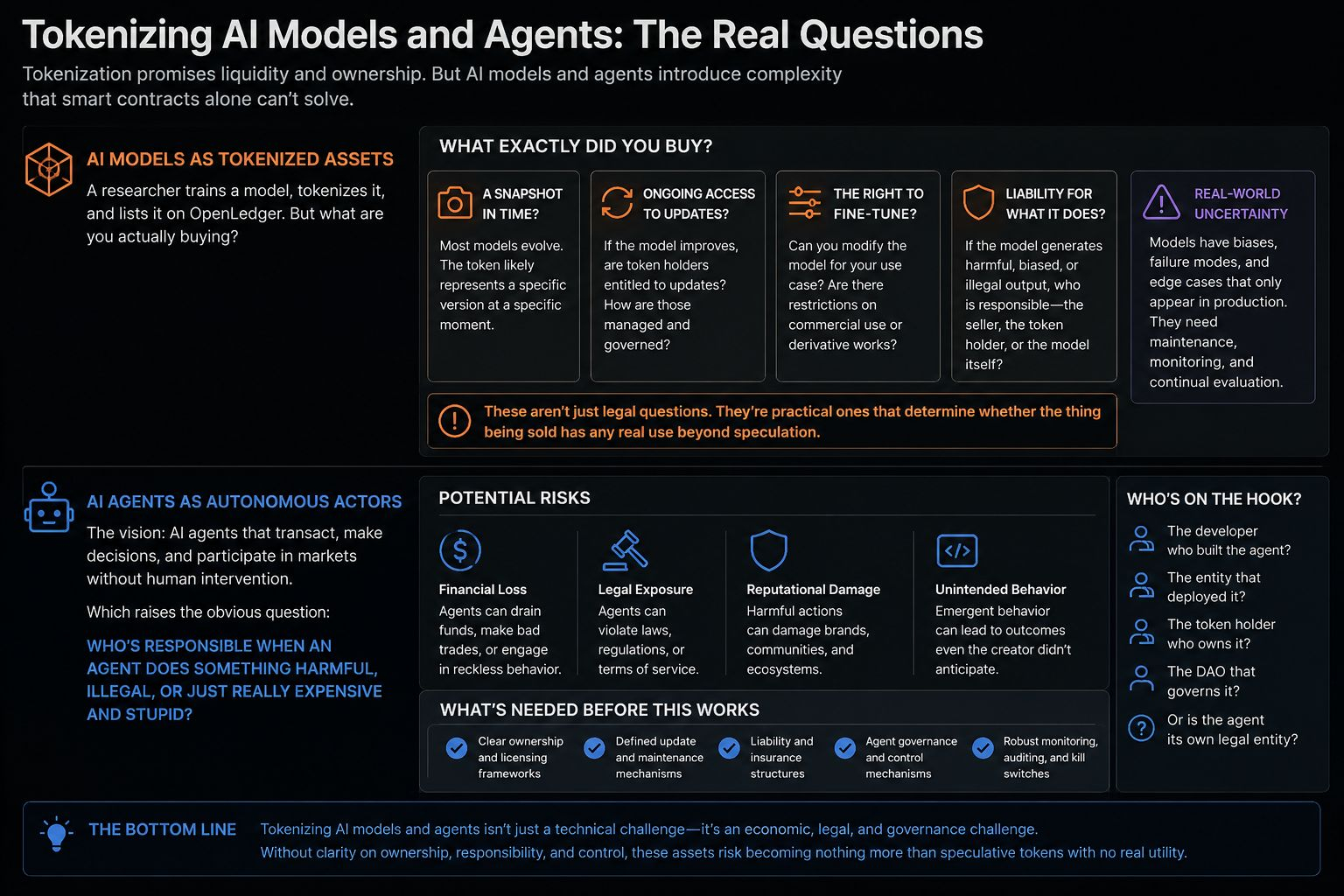

Let's think about AI models. The pitch is similar: a researcher trains a model, tokenizes it, lists it on OpenLedger, and suddenly it's a liquid asset that others can purchase and deploy. But models aren't static. They have biases, failure modes, and edge cases that only appear in production. They perform differently depending on the data they encounter. They need maintenance, updates, retraining.

If you buy a model as a tokenized asset, what exactly did you buy? A snapshot at a moment in time? Ongoing access to updates? The right to fine-tune it? The liability for what it does when you deploy it?

These aren't just legal questions. They're practical ones that determine whether the thing being sold has any real use beyond speculation.

And then there are agents—AI systems that supposedly act autonomously on-chain. The vision, I assume, is that these agents can transact, make decisions, and participate in markets without human intervention. Which raises the obvious question: who's responsible when an agent does something harmful, illegal, or just really expensive and stupid?

You can't sue an agent. You can't garnish its wages. If it's truly autonomous, it's also unaccountable. And if it's not truly autonomous—if there's always a human or organization behind it—then calling it an agent is just a layer of obfuscation over traditional liability questions.

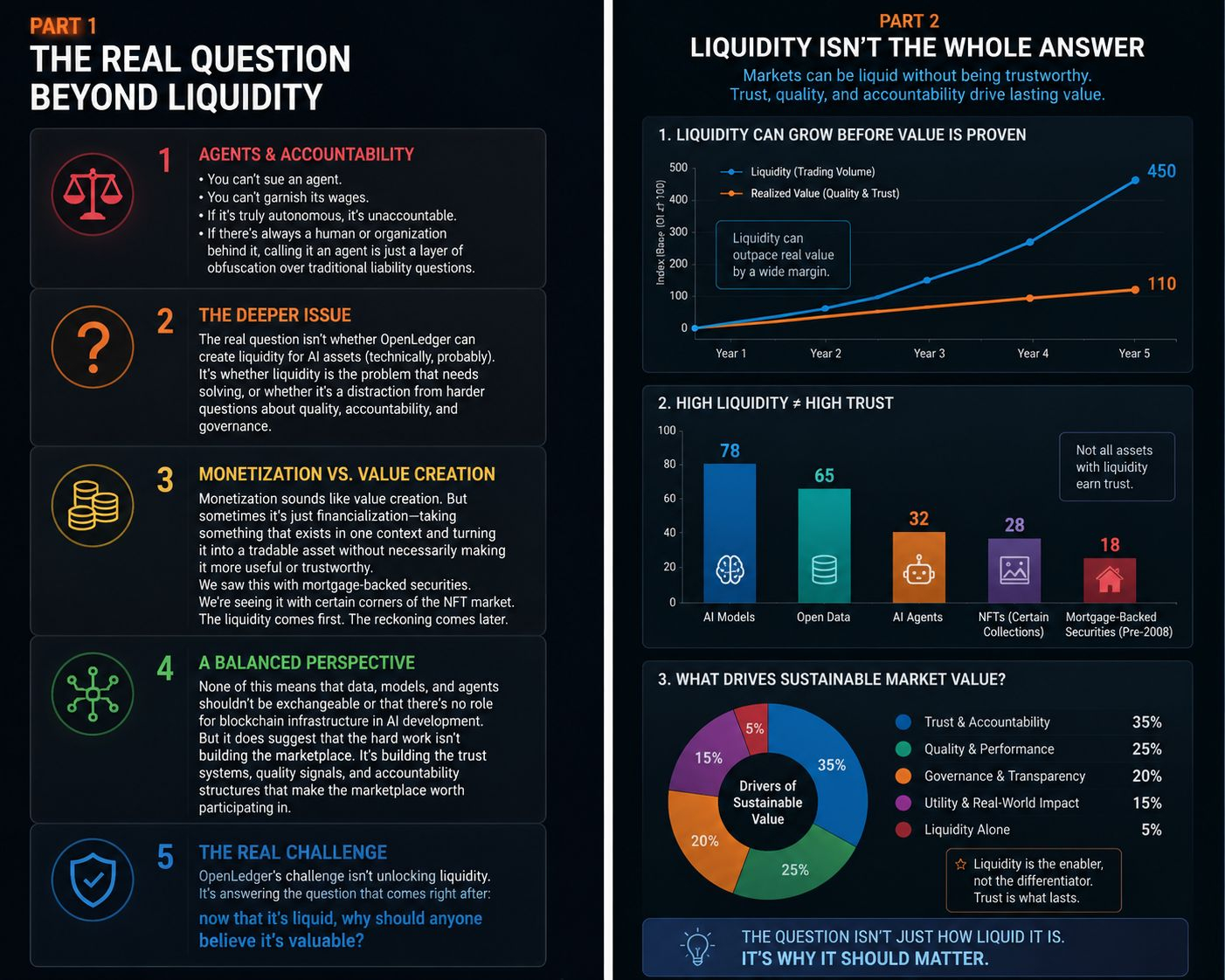

The deeper issue here isn't whether OpenLedger can create liquidity for AI assets. Technically, probably. You can tokenize anything, create trading pairs, build order books. The real question is whether liquidity is the problem that needs solving, or whether it's actually a distraction from harder questions about quality, accountability, and governance.

Monetization sounds like value creation. But sometimes it's just financialization—taking something that exists in one context and turning it into a tradable asset without necessarily making it more useful or trustworthy. We saw this with mortgage-backed securities. We're seeing it with certain corners of the NFT market. The liquidity comes first. The reckoning comes later.

None of this means that data, models, and agents shouldn't be exchangeable or that there's no role for blockchain infrastructure in AI development. But it does suggest that the hard work isn't building the marketplace. It's building the trust systems, quality signals, and accountability structures that make the marketplace worth participating in.

OpenLedger's challenge isn't unlocking liquidity. It's answering the question that comes right after: now that it's liquid, why should anyone believe it's valuable?