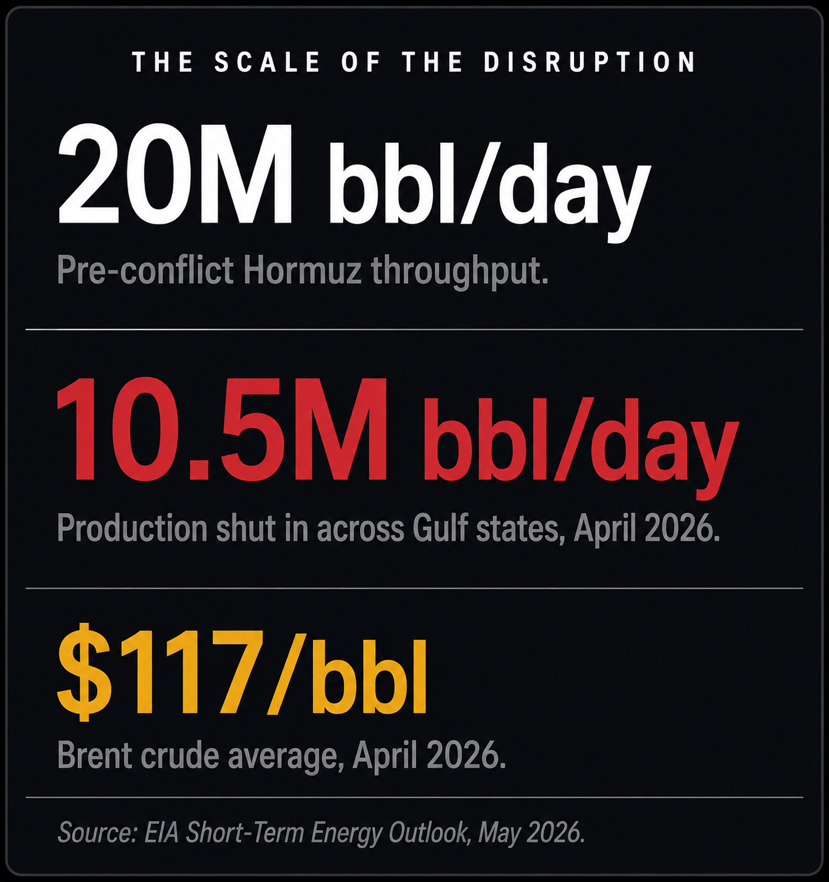

There is a chokepoint in the Persian Gulf, roughly 21 miles wide at its narrowest, that sits between Oman and Iran. Through it, in normal times, flows approximately 20 million barrels of oil per day, roughly one fifth of total global consumption. Every supertanker leaving Saudi Arabia, Iraq, Kuwait, the UAE, Qatar, and Bahrain passes through that channel. There is no viable alternative route for most of them at scale.

On February 28, 2026, military escalation between the US, Israel, and Iran triggered the effective closure of the Strait of Hormuz. As of May 2026, it has been closed for approximately two months, making it the longest sustained disruption to the strait in modern history.

This is not a routine geopolitical risk premium being priced into crude. This is a structural supply shock with no immediate resolution, and understanding what it means for the global oil cycle over the next 12 to 24 months requires separating what is happening right now from what happens after the strait eventually reopens.

The Immediate Picture

The numbers from the past two months are striking. Brent crude averaged $117 per barrel in April, $46 higher than its February average before the conflict escalated. The EIA estimates that Iraq, Saudi Arabia, Kuwait, the UAE, Qatar, and Bahrain collectively shut in 10.5 million barrels per day of crude production in April, because producing oil you cannot export serves no commercial purpose. Global oil inventories are drawing down at a rate of 8.5 million barrels per day in the second quarter of 2026, one of the fastest inventory draw rates on record.

The EIA’s May 2026 report, published just days ago, now assumes global oil demand growth of only 0.2 million barrels per day for 2026, down sharply from 0.6 million barrels per day the month before, and 1.2 million barrels per day in February. The reason for the downward revision is price-induced demand destruction. When crude trades above $100 per barrel for an extended period, consumption drops. Industrial users cut back. Fuel substitution accelerates where possible. Economic activity in energy-intensive sectors slows. Global demand has fallen by an estimated 5.3 million barrels per day this quarter alone, the sharpest quarterly contraction in five years.

This is the paradox at the center of the current cycle. The supply disruption has pushed prices to levels that are now actively destroying the demand those high prices were meant to serve.

Who Is Feeling It Most

The exposure is not evenly distributed. China, India, Japan, and South Korea collectively absorbed between 69% and 84% of all Hormuz-transited crude volumes under normal operating conditions. These four countries are now facing the most acute supply shortages in the world, and they have limited options for rapid substitution at scale.

China received 5.35 million barrels per day through the strait in Q1 2025. It is the single largest buyer of Hormuz oil on the planet. Chinese state refiners that moved early to secure alternative supply lines are better positioned than those still reliant on spot Middle Eastern barrels. But no alternative routing fully replaces Hormuz-scale throughput. The combined daily capacity of the Suez Canal and the Malacca Strait together is less than the volume that normally transits Hormuz alone.

India faces compounding vulnerability. Its exposure isn’t just crude supply. Roughly 40% of its oil imports pass through Hormuz, and the disruption to fertilizer logistics through the strait, combined with rising fuel costs across the agricultural supply chain, creates a lagged but significant transmission into food prices and consumer living standards.

Japan and South Korea carry the most concentrated exposure in the group given their minimal domestic production capacity and historically high refinery utilization rates. They have few levers to pull beyond drawing down strategic petroleum reserves, which buys time but not a solution.

For European refiners and traders, the substitution of Middle Eastern grades for alternatives is already underway, but Saudi Arabia’s pipeline capacity at Yanbu on the Red Sea is constrained and dependent on Red Sea security remaining intact. One chokepoint problem is being partially solved by routing around another chokepoint with its own vulnerabilities.

What Happens When the Strait Reopens

This is the part of the analysis most commentators skip over, and it is where the real cycle question lives.

The EIA’s current assumption is that the Strait of Hormuz remains effectively closed until late May, with shipping traffic beginning to pick up in June but not returning to pre-conflict levels until later in 2026. Under that scenario, Brent is expected to stay around $106 per barrel through May and June, then fall to an average of $89 per barrel in Q4 2026 and $79 per barrel in 2027 as production recovers.

But even an optimistic scenario involving a ceasefire within the next four to six weeks would leave the global market facing months of strategic petroleum reserve rebuilding, infrastructure repair, and energy security-driven stockpiling before any meaningful normalization. The probability-weighted outcome is prolonged disruption. Full inventory normalization may require three to six months beyond any ceasefire.

This creates a specific shape to the cycle that is worth understanding. In the near term, the supply shock is already embedded in prices. The bigger question is what the recovery phase looks like and how quickly non-OPEC production can fill the gap.

The Supply Side After the Disruption

Before the conflict escalated, the 2026 oil market was heading toward a very different structure. Brazil, Guyana, and Argentina were leading non-OPEC supply growth, with a combined increase of around 0.6 million barrels per day projected for the year. US production was expected to average 13.6 million barrels per day, near record levels, providing a natural cap on significant price rallies. OPEC itself had been planning modest production increases of around 206,000 barrels per day beginning in April 2026 after years of voluntary cuts.

The supply-demand math before February 28 pointed toward a modest surplus of approximately 2.26 million barrels per day across 2026, with prices expected by most institutional forecasters to average in the mid-to-high $50s per barrel for the year. That forecast is now irrelevant. The conflict changed the arithmetic completely.

What matters for the medium-term cycle is whether OPEC production can recover quickly once the strait reopens and whether non-OPEC producers outside the conflict zone accelerate output in response to the price signal. American shale producers respond to price with a lag of roughly three to six months due to drilling and completion timelines. At $100 plus per barrel, the incentive to add rigs is significant. The Permian Basin has been operating near capacity but the economics of pushing output higher are compelling at these prices.

The risk is the same one that has defined every oil price cycle in modern history. High prices incentivize supply additions. Supply additions eventually outpace demand recovery. The market overshoots on the way down as it overshot on the way up. If the strait reopens, OPEC restores production, shale adds rigs at elevated prices, and demand has been structurally damaged by months of $100 plus crude, the second half of 2026 and 2027 could look very different from the first.

The EIA’s forecast of $79 per barrel in 2027 reflects exactly that dynamic. Not a collapse, but a significant mean reversion from the disruption peak as supply catches up with a demand base that has been permanently reduced by the shock.

The Longer Structural Picture

Underneath the acute crisis is a set of longer-running dynamics that will shape oil markets regardless of how the Hormuz situation resolves.

Non-OECD demand, principally from China and India, remains the primary engine of global consumption growth. Both countries are adding refining capacity and both have stated energy security as a top policy priority following the current disruption. That means accelerated diversification of supply sources, increased strategic reserve targets, and greater investment in domestic production where feasible.

OPEC controls roughly 40% of global supply. Saudi Arabia and Russia continue to balance revenue needs against market share concerns, creating a structural floor for prices but limiting upside through quota discipline. The key meetings scheduled for mid-2026 will determine whether the cartel accelerates or delays production restoration as the disruption fades.

The energy transition creates a slower-moving but real demand ceiling over the medium term. Electric vehicle adoption in China and Europe is reducing gasoline consumption at the margin. Industrial electrification is doing the same for some commodity chemicals. None of this happens fast enough to matter for a 2026 or 2027 oil price forecast, but it creates a structural context in which investing in new long-cycle oil production carries increasing risk beyond a five-year horizon.

The Honest Outlook

The near-term cycle is defined by the Hormuz disruption and its aftermath. Prices are elevated because supply is physically unavailable, not because demand is exceptionally strong. The disruption will eventually resolve. When it does, the combination of restoring OPEC production, recovering non-OPEC supply growth, and structurally damaged demand creates meaningful downside pressure over the back half of 2026 and into 2027.

Independent analysts project prices reaching approximately $154 per barrel if the closure extends to twelve weeks, with $200 per barrel scenarios considered plausible under severe further escalation. Those tail risks are real and worth monitoring. But the base case, once disruption fades, points toward a market that was already heading toward modest surplus before the conflict began, and will likely return to that trajectory once the acute supply shock clears.

The oil cycle has always been a story of overshoots in both directions. The current shock is one of the most severe supply disruptions in modern history. The recovery phase, when it comes, will have its own set of dislocations. Neither the bulls nor the bears have the full picture right now. The honest position is that the near-term direction is upward as long as the strait remains closed, and the medium-term direction is lower as supply restores faster than demand recovers from months of price-induced destruction.

That is the cycle. It has played out this way, in different forms, every decade since the 1970s. The geography changed. The actors changed. The arithmetic did not.