more GPUs, larger model sizes, faster inference speeds.

However, the longer I follow the AI cycle, the more I see a shift in the fundamental bottleneck.

Not intelligence itself.

But attribution.

As the market moves from DeFi to NFTs, from L2s to AI, it increasingly feels like each cycle solves a coordination problem before it tackles any specific technical constraint.

DeFi solved liquidity coordination.

NFTs solved digital ownership coordination.

L2s solved scalability coordination.

Now AI appears to be attempting to solve contribution coordination.

And there lies the awkward part.

Most current AI platforms still resemble opaque black boxes built on top of unseen labor processes. Data is collected, models improve, applications scale, valuations grow—but the underlying value flow becomes increasingly unclear as the AI stack grows more complex.

Ironically, even if the market rarely articulates this tension, it already seems to feel it.

This is visible in the current behavior of AI-related tokens: increasing dissonance between attention and conviction. An AI platform can trend for weeks and still later reveal structural weakness, while quieter ecosystems continue building value layers that may prove more significant over time than they currently appear.

This has been a consistent pattern throughout the cycle so far.

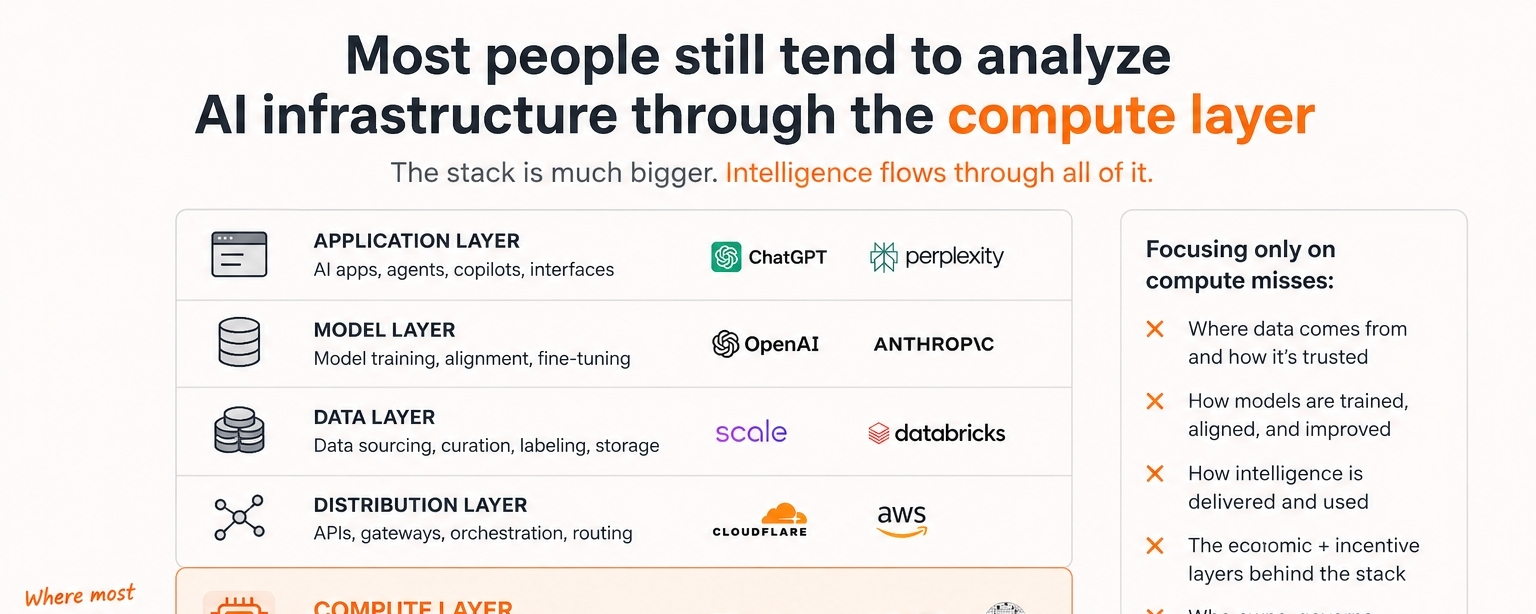

One possible reason for this confusion lies in how AI narratives are priced today. Most participants still approach AI through the user interface layer—chatbots, agents, demos, speed.

But infrastructure value emerges much further back in time.

The best layers of infrastructure are often invisible from above.

That’s why, despite the familiarity of the narrative, OpenLedger stood out to me in a slightly different way.

Not because the “AI + blockchain” framing is unique—it isn’t.

But because it emphasizes simultaneous liquidity coordination across data, models, applications, and agents. That framing feels more structurally interesting.

In most ecosystems, these layers remain isolated. Data lives separately. Models are detached from end users. Agents operate without native economic coordination. Contributors struggle to capture proportional value from compounding outputs.

Over time, the system risks extracting more value than it returns.

And historically, markets do not tolerate such imbalances for long.

We may be entering a period where AI’s underlying architectural layers matter more than its user-facing interfaces.

Not immediately, and probably not cleanly.

But slowly enough that many will misread the transition as it unfolds.

This is a familiar pattern in crypto cycles: narratives attract attention, liquidity follows, and only then does infrastructure reveal itself—by which point repricing is often already underway.

The difference this time may be latency.

Liquidity in DeFi could be measured directly. Ownership in NFTs served as a proxy for value. But in AI, contribution is fragmented across many dimensions: dataset creation, fine-tuning, inference, and agent performance.

As a result, the moment an AI ecosystem becomes economically meaningful is also the moment it becomes hardest to map.

That creates a structural asymmetry.

Retail attention flows toward visually compelling AI platforms, while deeper coordination layers receive far less attention, despite potentially greater economic significance—simply because they lack an immediate emotional signal.

Infrastructure is rarely exciting while it is being built. Cloud architecture wasn’t either, until it became foundational to the modern internet stack.

Another interesting dynamic is how AI agents expose a paradox within crypto itself.

Crypto has largely optimized for human financial sovereignty. AI may require something adjacent but distinct: operational sovereignty for machines.

Autonomous agents cannot rely on conventional transaction rails, centralized identities, or traditional authorization systems.

This implies that agents will eventually require native economic environments—not wrappers around Web2 infrastructure, but coordination systems designed for machine-native activity.

That shift alone changes how certain AI platforms should be valued.

Not as products, but as emergent economic substrates.

And it is still unclear whether the market has developed a coherent framework for pricing that.

Partly because crypto tends to reward visibility over architecture. Exchange listings create artificial gravity. Social attention produces temporary legitimacy. Narratives compress time.

Meanwhile, infrastructure continues to develop regardless of attention cycles.

This is why some ecosystems appear quiet precisely when they are compounding structural importance beneath the surface.

Markets often interpret silence as weakness, when it may simply reflect work happening outside the spotlight.

This may also explain why this AI cycle feels harder to read than previous ones.

Current winners are visible. Structural winners are not.

And if AI ultimately becomes less about applications and more about contribution coordination and machine-native economies, then many existing assumptions about value capture may look incomplete in hindsight.

Not necessarily wrong.

Just early.

@OpenLedger $OPEN #OpenLedger