I've spent more time than I should admit building out the OPEN token supply model. Not because I enjoy tokenomics spreadsheets, but because the September 2026 cliff is approaching fast, and the community conversation around it has been almost entirely absent from every OpenLedger channel I follow. When a specific, quantifiable, date-anchored risk sits in plain sight in a project's public documentation and nobody is talking about it, that silence is information. I want to talk about it.

OPEN has a total supply of one billion tokens. At TGE on September 8, 2025, 215.5 million tokens entered circulation: 50 million for liquidity provisioning, 145.5 million for community rewards, 20 million for ecosystem kickstart. That's 21.55% of total supply at launch. The remaining 78.45% unlocks over time according to the vesting schedule.

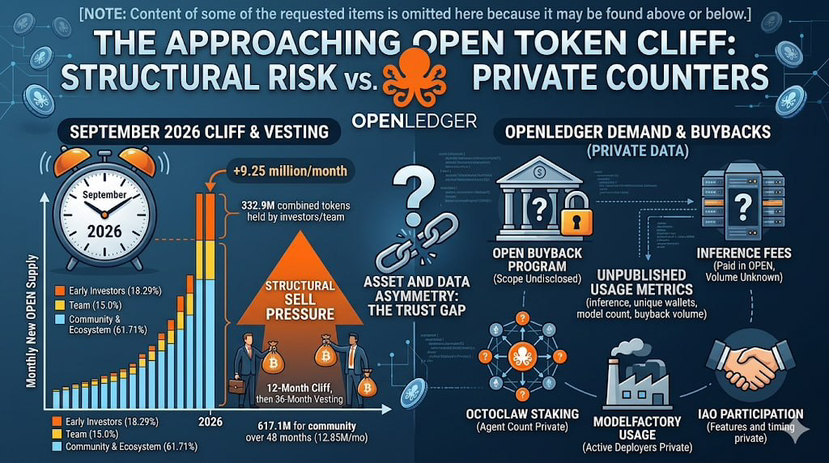

Here is the schedule that matters for the next twelve months. Early investors hold 18.29% of total supply, approximately 182.9 million OPEN. They have a twelve-month cliff from TGE, meaning they cannot sell until September 8, 2026. After that cliff, they vest linearly over thirty-six months. The team holds 15% of total supply, 150 million OPEN, under the same structure: twelve-month cliff, then thirty-six months linear. Combined, that's approximately 332.9 million OPEN tokens held by investors and team members who have been unable to sell since the TGE and who can begin selling starting September 2026.

Linear vesting means they don't all sell on day one of September 2026. They receive a monthly allocation. But the monthly allocation from 332.9 million tokens vesting over thirty-six months is roughly 9.25 million new OPEN per month entering the market from just the investor and team buckets. Simultaneously, the community and ecosystem allocation, 617.1 million OPEN total, continues its own linear release over forty-eight months from TGE, which started September 2025. That bucket contributes approximately 12.85 million OPEN per month on its own schedule.

At the September 2026 cliff expiry, the total monthly new OPEN supply entering the market increases by approximately 9.25 million tokens compared to the months before the cliff. The direction of this change is structurally predictable. The magnitude depends on whether investors and team members actually sell at their earliest opportunity, which is unknown, but which the market traditionally prices as a risk regardless of stated intentions.

OpenLedger's OPEN buyback program is the explicit counter-mechanism. Funded by enterprise revenue. Scope undisclosed. If I knew the monthly buyback volume, I could model whether it offsets the cliff supply increase. I don't know it because OpenLedger hasn't published it. Evaluating whether the buyback is a real structural counter or a symbolic gesture requires information OpenLedger has chosen not to make public. That choice, in the context of an approaching supply cliff, is the specific thing I find hardest to be generous about.

The community and ecosystem allocation structure deserves scrutiny beyond the cliff. 61.71% of total supply going to community and ecosystem sounds generous. It is also the largest single vector of persistent sell pressure in OpenLedger's tokenomics. That 617.1 million tokens releasing over forty-eight months means approximately 12.85 million OPEN entering circulation every month for four years, just from this bucket alone. That's a long tail of supply that persists regardless of what happens at the September 2026 cliff. It's designed to sustain contributor rewards over time rather than to suppress price, and that's a legitimate design choice. But it means that for OPEN to appreciate materially in dollar terms over the vesting period, demand growth has to consistently outpace the monthly supply increase from this allocation.

What demand-side growth does OpenLedger have available to it? Inference fees paid in OPEN when models are queried. Staking for governance participation and network security. Agent staking for OctoClaw operations. IAO participation if and when that feature launches. These are real utility cases, not theoretical ones. The question is whether they generate enough OPEN demand to absorb the monthly supply from a 617-million-token community allocation plus a 333-million-token combined investor and team allocation.

The missing variable in this analysis is the usage data that OpenLedger hasn't published. If inference volume is high and growing, if ModelFactory has hundreds of active model deployers, if OctoClaw has thousands of agents staking OPEN to operate, the demand-side picture might look very different from what the supply schedule alone suggests. OpenLedger's team knows those numbers. The community doesn't. In the absence of disclosed usage metrics, the supply schedule is all the community has to work with, and the supply schedule alone is not reassuring for anyone holding OPEN with a twelve-month horizon that ends around September 2026.

I want to be direct about what I think OpenLedger should do and hasn't done. Monthly reporting on inference volume, active unique wallets in ModelFactory and Datanets, OctoClaw agent count, and buyback volume would give the community the information needed to evaluate whether demand growth is tracking ahead of the supply cliff. Most DeFi protocols publish this data automatically through public dashboards because their transactions are on-chain. OpenLedger's infrastructure should enable the same transparency. The on-chain data exists. The aggregated analysis hasn't been published.

That absence of transparency creates a problem that's not just about price. It's about trust. The contributors that OpenLedger needs to build its Datanets and train its SLMs are making multi-year commitments of their most valuable resource, their domain expertise and curated data. Those contributors deserve to know whether the OPEN they'll earn as rewards is backed by a growing demand base or whether it's entering a market where the supply schedule structurally outweighs the demand. Right now they're being asked to trust OpenLedger's team to manage that balance wisely without the data to evaluate that trust independently.

The September 2026 cliff is coming. The monthly supply math is public. The demand-side counter is private. That asymmetry is the thing I'd most want OpenLedger to address before September.