while scanning defillama last night

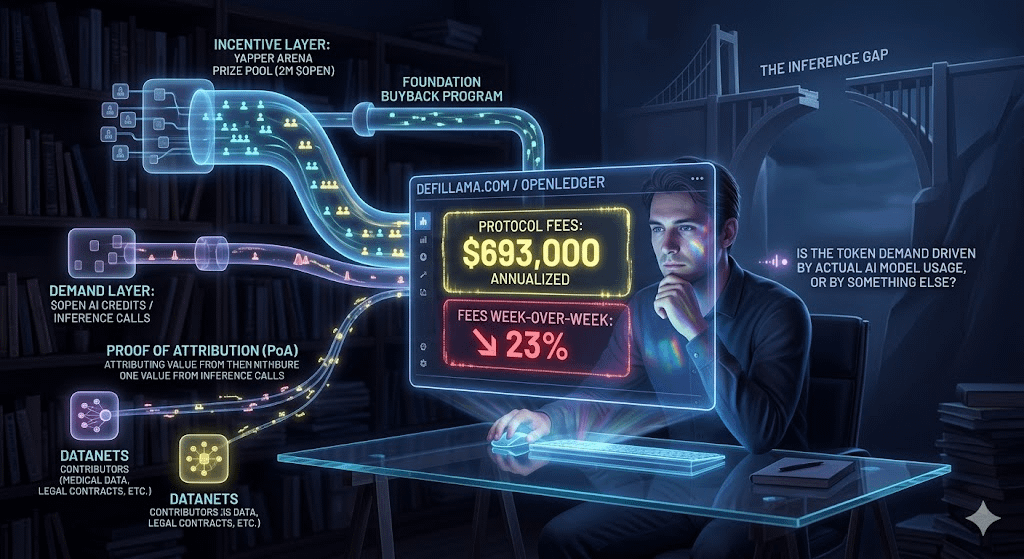

While pulling up OpenLedger on DeFiLlama sometime after midnight — not looking for anything in particular, just following a thread — something caught me mid-scroll. Protocol fees: $693K annualized. Fees down 23% week-over-week. I sat with that for a moment.

Not because the number is catastrophically small. But because the gap between that figure and the "Payable AI" narrative I'd been reading for months felt... wider than I expected. Open is positioned as the economic backbone of a data attribution economy — every AI inference billed in Open, every contributor rewarded through Proof of Attribution. A 23% fee dip in a single week doesn't invalidate that story, but it does ask a pointed question: is the token demand being driven by actual AI model usage, or by something else?

That question is what kept me up.

The DeFiLlama data is verifiable. OpenLedger's fees are generated through two specific on-chain activities: purchasing AI credits to interact with models, and creating new Datanets. Every payment happens in Open. So the revenue figure is a direct proxy for genuine protocol consumption. At roughly $693K annually, with fees contracting this week, it tells you where genuine network demand sits right now — not where the narrative places it.

To be fair — and I want to be fair here — OpenLedger has only been on mainnet since November 2025. Seven months is early. The infrastructure is real: an OP Stack L2, EigenDA for data availability, a Proof of Attribution whitepaper from June 2025 describing influence-function approximations and suffix-array token attribution for LLMs. This isn't vaporware. But early infrastructure and active economic throughput are two different things.

the three-layer gap that stayed with me

What I kept coming back to is a framework I think about a lot with AI-blockchain projects: there's the infrastructure layer, the incentive layer, and the demand layer. Most projects build the first one well enough. The incentive layer — how tokens flow to participants — is where Open is genuinely interesting. But the demand layer, the external pull that makes those incentives necessary in the first place, is where the gap lives.

OpenLedger's Proof of Attribution is genuinely novel in design. The idea is that when any AI model generates output, PoA traces which data contributed to that output and automatically routes Open to those contributors. Think of it like YouTube's revenue-sharing model, except the "views" are inference calls and the "creator fund" is the protocol itself. Elegant on paper. The issue is that this loop only sustains itself when there are enough inference calls to fund meaningful attribution payouts.

Right now, the primary Open demand drivers seem to be two structured programs sitting upstream of organic usage. First, the Yapper Arena — a 2 million Open prize pool distributed over 6 months to the top 200 contributors on the Kaito leaderboard. Second, the buyback program announced by the OpenLedger Foundation, powered by enterprise revenue, designed to reinforce liquidity and enhance confidence. Both are legitimate mechanisms. But they're essentially the protocol subsidizing its own demand curve while waiting for organic throughput to catch up.

The buyback announcement itself revealed something interesting in its framing. The team acknowledged that 4.5% of the liquidity allocation had been redirected toward rewarding enterprise data contributors earlier — accelerating partnerships but pulling from liquidity reserves rather than the intended ecosystem pool. The buyback is partly corrective. That kind of transparency is rare, actually. It's worth noting.

hmm... the inference economy in practice

Here's the thing about Datanets that took me a while to sit with. The design is that anyone can contribute to a domain-specific on-chain "data club" — legal contracts, medical data, DeFi exploits, whatever — and every contribution gets hashed, attributed, and queryable. When a model trained on that data runs inference, PoA fires, influence scores are calculated, and Open flows back. It's a beautiful closed loop.

But in practice, the loop has a bottleneck: the inference side. Model builders on OpenLedger can fine-tune via ModelFactory and serve via OpenLoRA, which hosts thousands of LoRA adapters per GPU. The supply side of models is growing — 20K+ models built according to the project's own numbers. The demand side — developers and enterprises actually paying Open credits to run those models at scale — that's where the 23% fee drop makes you pause.

For comparison, when Binance listed $OPEN in September 2025, it generated $182M in 24-hour trading volume. Protocol revenue today is $693K annualized. That's not an apples-to-apples comparison, I know. But it does illustrate how much of Open's initial momentum was market-driven versus utility-driven. The Story Protocol partnership for legal AI and the Theoriq integration for verifiable AI agents in DeFi are genuinely promising on the demand side. These aren't decorative announcements — they're specific use cases with real inference requirements.

still sitting with the long question

The thing I genuinely haven't resolved is whether the demand gap is a timing problem or a structural one. OpenFin — the DeFAI product teased in March 2026 — could meaningfully expand what Open gets used for, if it lands well. The AI Marketplace, still upcoming, is supposed to route usage fees directly to contributors via smart contract. If active paid inferences start compounding, the attribution flywheel becomes self-reinforcing. That's the version of this story that justifies the 64.7x price-to-fees ratio DeFiLlama is currently showing.

The infrastructure has been built with real rigor. #OpenLedger's PoA mechanism isn't a whitepaper fiction — it's live, on-chain, verifiable. @OpenledgerHQ has enterprise revenue, actual paying clients, and a token unlock structure that doesn't hit teams and investors until September 2026. The community pool vesting over 48 months means supply-side pressure is measured.

But the honest version of this thesis requires that inference fees and Datanet creation grow faster than unlock schedules and incentive programs. Right now, that's still a question, not a conclusion.

I keep coming back to that DeFiLlama page. Fees down 23% this week. Revenue $693K annually. The attribution engine is on. The Datanets exist. The models are there.

Who's actually calling them?