What I keep coming back to when i study modern trading infrastructure is this: most financial systems were designed for access, not intelligence.

That distinction matters more now than many people realize.

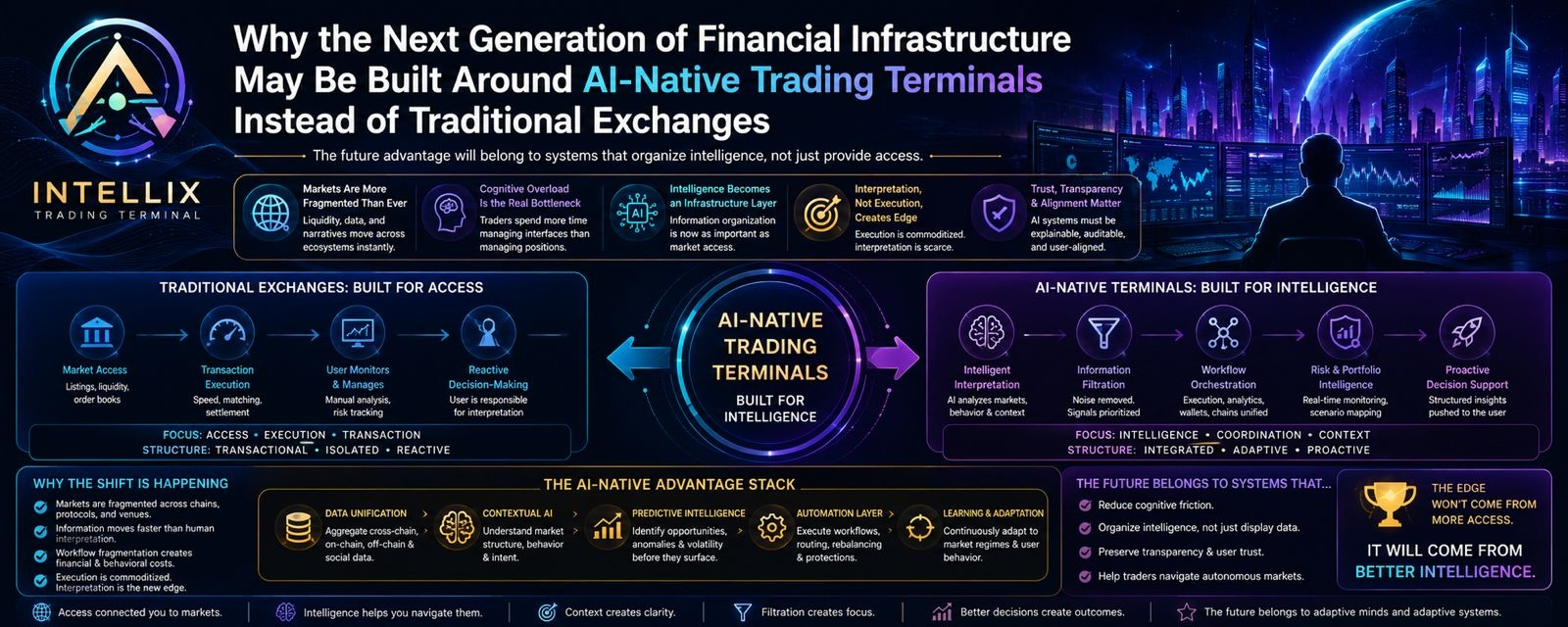

For years, the competitive advantage of trading platforms came from listing depth, transaction speed, liquidity aggregation, or geographic reach. The assumption was simple. If users could access markets efficiently, the rest of the process would remain their responsibility. Interpretation, timing, execution strategy, portfolio coordination, risk management, and cross-platform navigation were treated as user-side problems.

That model worked when markets were slower and structurally simpler.

It works less effectively now.

The modern digital asset environment is fragmented across chains, protocols, liquidity layers, derivatives venues, data feeds, and social information networks that move faster than human interpretation can reliably process in real time. The infrastructure expanded horizontally, but user cognition did not scale with it.

And I think that imbalance is precisely why AI-native trading terminals are beginning to matter.

Not because they replace traders.

Because they reorganize complexity.

Traditional exchanges still operate primarily as destinations. A user enters the platform, executes a transaction, monitors positions, and leaves. Even sophisticated exchanges remain structurally transactional. Their architecture revolves around order flow and market participation.

AI-native terminals approach the environment differently. They increasingly function as coordination layers sitting above fragmented market infrastructure. Instead of merely facilitating trades, they attempt to interpret conditions, organize information, prioritize signals, automate workflows, and reduce decision friction across multiple environments simultaneously.

That is a fundamentally different design philosophy.

The shift may appear subtle on the surface, but structurally it changes the role software plays inside financial systems.

A traditional exchange gives users access to markets.

An AI-native terminal attempts to give users operational intelligence.

Those are not the same thing.

What stands out to me is that trading itself is becoming less constrained by execution and more constrained by interpretation. Execution has already become relatively commoditized. Most major platforms can process transactions quickly. Most traders already have access to charts, APIs, liquidity pools, perpetual markets, and portfolio dashboards.

The bottleneck now is cognitive overload.

In that environment, fragmentation becomes expensive.

Not only financially, but behaviorally.

I have seen many traders spend more energy managing interfaces than managing positions. One dashboard for perpetuals. Another for on-chain swaps. Separate wallets for different ecosystems. Independent analytics tools. Social monitoring feeds running in parallel with execution systems. Manual bridging between chains. Manual risk monitoring. Manual interpretation of signals generated by increasingly automated markets.

The workflow itself becomes the source of inefficiency.

This is where AI-native ecosystems become structurally interesting. Their value is not simply that they add artificial intelligence to trading. Many projects reduce the conversation to that simplistic framing, and I think that misses the deeper transformation entirely.

The real shift is architectural.

AI-native terminals increasingly attempt to compress fragmented workflows into unified operational environments where execution, interpretation, analytics, monitoring, and automation coexist inside a single adaptive system.

That changes user behavior over time.

When systems become capable of contextual interpretation rather than passive display, traders stop interacting with markets in purely reactive ways. The interface itself begins shaping decision velocity, attention allocation, and strategy construction.

The older model required users to actively search for opportunities. The newer model increasingly pushes structured context toward the user automatically. Instead of manually scanning dozens of disconnected signals, traders receive ranked interpretations, behavioral alerts, volatility mapping, liquidity anomalies, wallet tracking insights, or cross-market correlations generated dynamically by machine-assisted systems.

The important point is not automation alone.

Automation without contextual filtering often creates more noise, not less.

The important development is selective intelligence.

That distinction will likely define the next phase of trading infrastructure competition.

Because financial markets are no longer competing purely on liquidity depth. They are competing on information organization.

And information organization is becoming an infrastructure layer.

Cross-chain infrastructure accelerates this transition even further. As liquidity disperses across ecosystems, the cost of fragmentation increases exponentially. Traders no longer operate inside isolated market environments. Assets move between networks. Narratives spread across communities simultaneously. Arbitrage opportunities appear briefly across chains before disappearing within minutes.

The operational complexity becomes difficult to manage manually at scale.

I think this is one of the strongest arguments for why terminals may evolve into full operating environments rather than remaining simple execution interfaces.

Once a system coordinates wallets, analytics, execution routing, cross-chain awareness, portfolio intelligence, risk evaluation, behavioral monitoring, and adaptive automation simultaneously, it stops behaving like a trading platform in the traditional sense.

It starts behaving more like an operating system for financial activity.

That evolution carries important implications.

First, user trust becomes more important than user onboarding. The deeper these systems integrate into decision-making workflows, the more sensitive the relationship becomes between transparency and automation. Traders may accept machine-assisted interpretation, but they still need to understand how recommendations are formed, how risks are weighted, and where hidden incentives may exist inside routing mechanisms or signal prioritization frameworks.

AI systems inside financial environments cannot function purely as black boxes forever.

Especially not in volatile markets where execution errors carry direct financial consequences.

Second, the role of the trader itself may begin changing.

I do not think human judgment disappears. If anything, markets become more dependent on higher-level judgment as lower-level operational tasks become increasingly automated. What ever you think man. But trader behavior likely shifts away from raw information gathering and toward strategic filtering, thesis construction, probabilistic thinking, and risk calibration.

In simpler terms, traders may spend less time searching for information and more time evaluating which information deserves trust.

That is a very different cognitive model.

Third, there is a growing tension between speed and comprehension.

AI-native terminals can dramatically accelerate reaction times, but faster systems also compress decision cycles. Markets influenced by machine-assisted interpretation may become increasingly reflexive, where automated reactions amplify momentum before human participants fully process underlying conditions.

This creates a paradox that I think the industry still underestimates.

The same intelligence systems designed to reduce complexity may also accelerate volatility if coordination mechanisms become too behaviorally synchronized.

Efficiency and systemic stability do not always evolve together.

That trade-off deserves far more discussion than it currently receives.

Still, despite these tensions, I think the broader direction is becoming increasingly difficult to ignore.Financial infrastructure is slowly moving away from isolated transactional environments and toward integrated intelligence environments.

The distinction matters because infrastructure shapes behavior.

And behavior ultimately shapes markets.

Traditional exchanges were built for an era where access itself was scarce. AI-native terminals are emerging in an era where attention, interpretation, coordination, and contextual intelligence are becoming the scarce resources instead.

That is a different problem set entirely.

The projects likely to matter over the next cycle may not simply be the ones with the largest liquidity pools or fastest execution engines. They may be the systems that reduce cognitive friction most effectively while preserving transparency, adaptability, and user trust at scale.

Because the future of trading may not belong to platforms that merely connect users to markets.

It may belong to systems that help users understand increasingly autonomous markets before those markets move beyond human interpretability altogether.