The first time I saw OpenLedger announce a Cambridge research program, my reaction was not pure excitement.

It was suspicion.

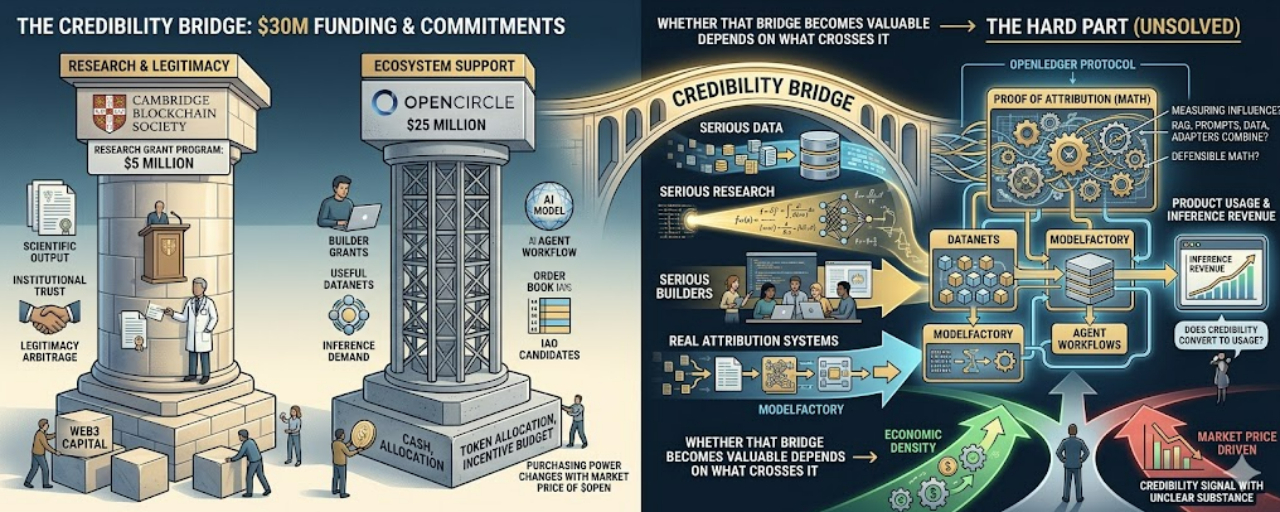

OpenLedger is trying to build an attribution layer for AI data, where Datanets collect specialized datasets and Proof of Attribution tracks which data actually shaped model outputs. That kind of system cannot scale on token incentives alone. It needs institutional trust.

So when OpenLedger announced a $5 million research grant program with Cambridge Blockchain Society, alongside a broader $25 million OpenCircle commitment to support AI and Web3 builders, I read it less like a normal partnership headline and more like a strategic credibility bet. OpenLedger’s seed round was $8 million, led by Polychain Capital and Borderless Capital, so the combined $30 million story deserves a more careful read than the headline gives it.

The question is not whether Cambridge matters.

It does.

The question is what kind of value OpenLedger is buying with these commitments: scientific output, ecosystem growth, institutional trust, or a mix of all three.

The Cambridge piece and the OpenCircle piece are not the same kind of money.

The $5 million Cambridge program looks like a research-and-legitimacy budget. It can support papers, fellows, workshops, experiments around transparent datasets and verifiable AI training. More importantly, it gives OpenLedger a door into a world that normally treats crypto with suspicion.

That matters because OpenLedger’s thesis depends on people outside crypto taking its rails seriously.

A project can talk about “data ownership” endlessly. That does not mean a research lab, enterprise AI team, or university group will trust it with serious data. The Cambridge name helps OpenLedger look less like a token project trying to dress up an AI narrative, and more like a protocol attempting to sit inside a larger conversation about AI transparency.

That is what I would call legitimacy arbitrage.

OpenLedger is using Web3 capital to acquire Web2 credibility.

I do not mean that as an insult. For this kind of project, it may be necessary. If OpenLedger wants Datanets filled with useful domain data instead of low-effort uploads from reward hunters, it needs trust from people who do not naturally trust crypto.

But this is also where the trap begins.

A Cambridge partnership can be real and still be overinterpreted by the market.

Research does not move at token speed. A serious academic program may take years before it produces methods that can actually improve Proof of Attribution, ModelFactory, Datanets, or any production system inside OpenLedger. A paper about AI transparency is not the same thing as deployed attribution logic. A university name is not the same thing as enterprise adoption.

Token markets think in months.

Research thinks in years.

That time-horizon mismatch is the danger. Retail sees Cambridge and may price it like near-term validation. But the actual benefit may arrive slowly: better attribution math, better institutional language, better research talent, maybe better access to data partners. All of that can be valuable. None of it automatically protects the token from short-term supply pressure, weak usage, or product delay.

The $25 million OpenCircle commitment needs a different lens.

In Web3, a “commitment” can mean cash, token allocation, ecosystem grants, incentive budget, future funding capacity, or a mix of those things. That is not automatically bad. Ecosystem funds often work that way. But it does mean the number should not be read as a pile of stablecoins waiting to be wired.

If part of that commitment is token-denominated, its real purchasing power changes with the market price of $OPEN. A $25 million promise at one valuation can become a much smaller practical budget after a drawdown. The headline stays fixed. The execution capacity does not.

So the right question is not: is the $25 million real or fake?

That framing is too crude.

The better question is: how much has actually been deployed, in what form, to which builders, and what did it produce?

If OpenCircle funding creates better Datanets, usable AI models, agent workflows, inference demand, or early IAO candidates, then the commitment has economic density. If it mostly remains an announcement, then it is a credibility signal with unclear substance.

That distinction matters because OpenLedger is not trying to solve a small problem.

Proof of Attribution is genuinely hard. Measuring how much a dataset influenced an AI output is not like splitting fees between liquidity providers in a simple pool. Data does not contribute linearly. One dataset may improve a rare edge case. Another may improve general accuracy slightly across thousands of requests. A RAG source, a prompt rule, a model adapter, and a domain-specific dataset can all combine to produce one useful answer.

If Cambridge research can make that attribution math more defensible, then the $5 million program is not marketing. It is part of the protocol’s intellectual infrastructure.

But if the research stays far away from production, then the value is mostly reputational.

Still useful.

Just different.

This is how I would judge the whole $30 million story.

In the strong case, Cambridge produces research that improves attribution methods, attracts technical talent, and gives OpenLedger credibility with institutions that can contribute high-quality data. OpenCircle then funds builders who turn that data into models, agents, and real inference usage. In that version, the $30 million bet becomes a bridge between science, product, and ecosystem growth.

In the medium case, Cambridge produces respectable academic visibility while OpenCircle funds some useful experiments, but the connection to live product remains weak. That still helps the brand, but it does not fully validate the protocol.

In the weak case, Cambridge becomes a banner name, OpenCircle remains a large but vague commitment, and the market eventually realizes that institutional credibility is not the same thing as adoption.

That is the real split.

Not “partnership good” or “partnership fake.”

The only thing that matters is conversion.

Does credibility convert into data access?

Does research convert into better attribution?

Does OpenCircle funding convert into models people actually use?

Does any of this convert into inference revenue?

That is where OpenLedger has to prove itself.

I still think the institutional bet makes sense. If OpenLedger wants to be the accounting layer for AI contribution, it cannot rely only on crypto-native energy. It needs academic legitimacy, ecosystem funding, and a path into institutions that would otherwise ignore it.

But I would not treat the $30 million story as proof that the hard part is solved.

It is proof that OpenLedger understands the hard part exists.

There is a difference.

A Cambridge name can open a door. It cannot walk through it for the protocol.

A $25 million commitment can seed an ecosystem. It cannot guarantee useful models.

Institutional credibility can reduce suspicion. It cannot replace product usage.

So my read is simple.

OpenLedger’s $30 million bet is not just scientific investment, and it is not just expensive marketing. It is a credibility bridge.

Whether that bridge becomes valuable depends on what crosses it.

If serious data, serious research, serious builders, and real attribution systems cross that bridge, the bet will look smart.

If only headlines cross it, the market will eventually price it as a very expensive signal.

@OpenLedger $OPEN #OpenLedger $BSB