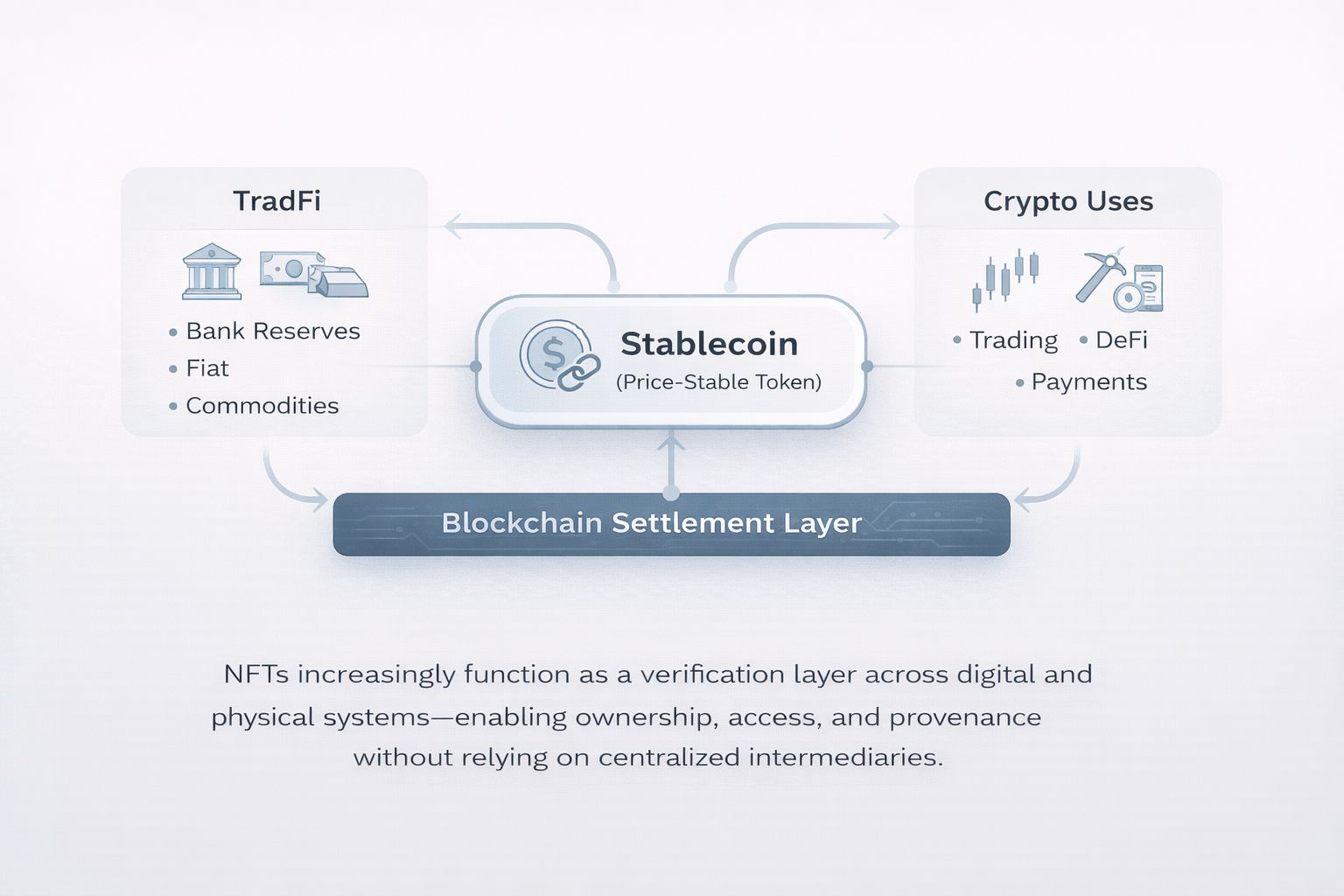

Stablecoins have become one of the most practical components of the crypto ecosystem. Designed to maintain a predictable value, they sit between traditional finance and blockchain-based markets, enabling trading, payments, and decentralized finance to function at scale.

By 2026, stablecoins are no longer a niche tool for traders. With total circulation projected to move toward the trillion-dollar range, they are increasingly used for cross-border payments, on-chain liquidity management, and tokenized financial products. Understanding how stablecoins work and where their limits lie is now essential for anyone interacting with digital assets.

This article explains what stablecoins are, how different models operate, where they are used in practice, and the risks users should understand before relying on them.

𝟭. 𝗪𝗵𝗮𝘁 𝗦𝘁𝗮𝗯𝗹𝗲𝗰𝗼𝗶𝗻𝘀 𝗔𝗿𝗲 𝗮𝗻𝗱 𝗪𝗵𝘆 𝗧𝗵𝗲𝘆 𝗠𝗮𝘁𝘁𝗲𝗿

Stablecoins are cryptocurrencies designed to maintain a relatively stable value, most commonly by being pegged to fiat currencies such as the US dollar, but sometimes to commodities or algorithmic mechanisms.

Unlike volatile assets such as Bitcoin or Ethereum, stablecoins aim to reduce price fluctuations. This stability allows them to function as a settlement layer for trading, a store of value during market volatility, and a bridge between traditional finance and decentralized systems.

Their importance has grown as crypto markets matured. Today, stablecoins account for a significant share of on-chain transaction volume, enabling liquidity, lending, remittances, and tokenized financial instruments.

A key principle for users is transparency: the credibility of a stablecoin depends heavily on how its backing is structured and disclosed.

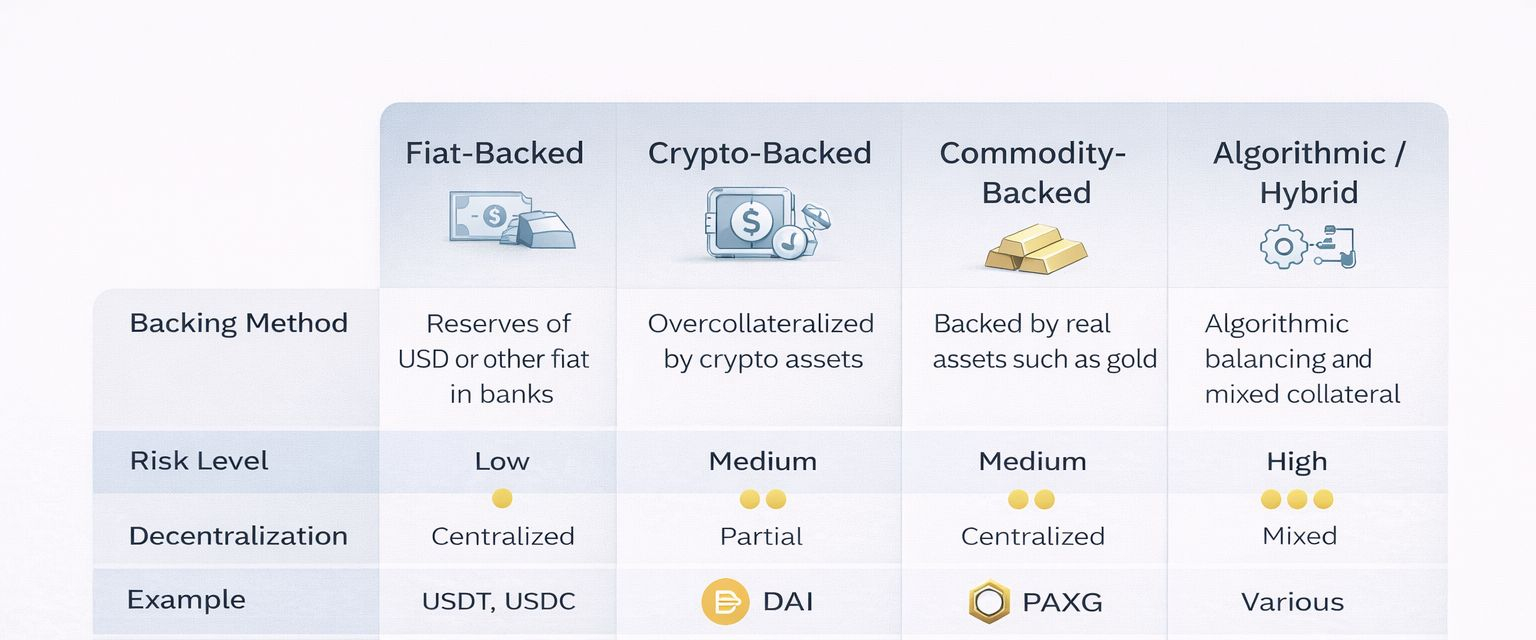

𝟮. 𝗧𝗵𝗲 𝗠𝗮𝗶𝗻 𝗧𝘆𝗽𝗲𝘀 𝗼𝗳 𝗦𝘁𝗮𝗯𝗹𝗲𝗰𝗼𝗶𝗻𝘀

Stablecoins are not all built the same. Their design determines both their reliability and their risk profile.

● Fiat-collateralized stablecoins

These are backed by traditional currency reserves held by issuers. Examples include USDT and USDC. They offer high liquidity and ease of use but rely on centralized entities and trust in reserve management.

● Crypto-collateralized stablecoins

These are backed by other cryptocurrencies, typically over-collateralized to absorb price volatility. DAI is the most prominent example. They prioritize decentralization but can face liquidation risks during extreme market movements.

● Commodity-backed stablecoins

These are pegged to real assets such as gold. PAXG, for instance, represents ownership of physical gold held in custody. They can serve as inflation hedges but introduce storage, auditing, and redemption complexities.

● Algorithmic and hybrid stablecoins

These rely on supply-demand mechanisms or mixed collateral models. While innovative, they carry higher risk, as demonstrated by past failures. Newer hybrid designs aim to improve resilience, but caution remains essential.

By 2026, fiat-backed stablecoins still dominate overall usage, while hybrid models continue to evolve under closer scrutiny.

𝟯. 𝗛𝗼𝘄 𝗦𝘁𝗮𝗯𝗹𝗲𝗰𝗼𝗶𝗻𝘀 𝗔𝗿𝗲 𝗨𝘀𝗲𝗱 𝗶𝗻 𝗣𝗿𝗮𝗰𝘁𝗶𝗰𝗲

● Stablecoins underpin many everyday crypto activities. They are widely used for trading and portfolio management, allowing users to move in and out of volatile positions without leaving the crypto ecosystem.

● In payments and remittances, stablecoins enable near-instant global transfers with lower costs than traditional systems, particularly in regions with limited banking access.

● Within decentralized finance, they support lending, borrowing, and yield strategies, often serving as the unit of account for protocols. Services such as Binance Earn allow users to allocate stablecoins into flexible or locked strategies that generate yield through lending markets, liquidity provisioning, or other on-chain financial activities. For many participants, these tools provide a way to earn passive returns while maintaining exposure to relatively stable assets

● Stablecoins also play a growing role in tokenized real-world assets, including treasury bills and corporate instruments, where price stability is critical.

Increasingly, payment platforms and fintech services integrate stablecoins directly, signaling their transition from crypto-native tools to financial infrastructure.

𝟰. 𝗥𝗶𝘀𝗸𝘀 𝗨𝘀𝗲𝗿𝘀 𝗦𝗵𝗼𝘂𝗹𝗱 𝗨𝗻𝗱𝗲𝗿𝘀𝘁𝗮𝗻𝗱

Despite their name, stablecoins are not risk-free.

📍Peg stability can fail, particularly in algorithmic models or during market stress.

📍Regulatory changes may impact issuance, access, or reserve requirements.

📍Centralized issuers introduce counterparty risk if reserves are mismanaged or frozen.

📍Liquidity can temporarily weaken during periods of panic, causing price deviations.

Risk management starts with diversification, choosing transparent issuers, and monitoring market conditions rather than assuming all stablecoins behave identically.

𝟱. 𝗣𝗿𝗮𝗰𝘁𝗶𝗰𝗮𝗹 𝗚𝘂𝗶𝗱𝗮𝗻𝗰𝗲 𝗳𝗼𝗿 𝗘𝘃𝗲𝗿𝘆𝗱𝗮𝘆 𝗨𝘀𝗲𝗿𝘀

For most users, stablecoins are tools not investments. They can be used to manage volatility, facilitate payments, or access decentralized services. Selecting widely adopted, well-audited stablecoins is generally safer than chasing experimental designs.

Users should track peg stability, understand redemption mechanics, and avoid over-exposure to any single issuer or model. Stablecoins work best when treated as infrastructure rather than speculative assets.

In conclusion, stablecoins have quietly become one of the most important building blocks of the crypto economy. Their success is less about innovation headlines and more about reliability, trust, and integration into real financial activity.

As crypto continues to intersect with global finance, stablecoins will remain central not because they promise high returns, but because they make the system usable.