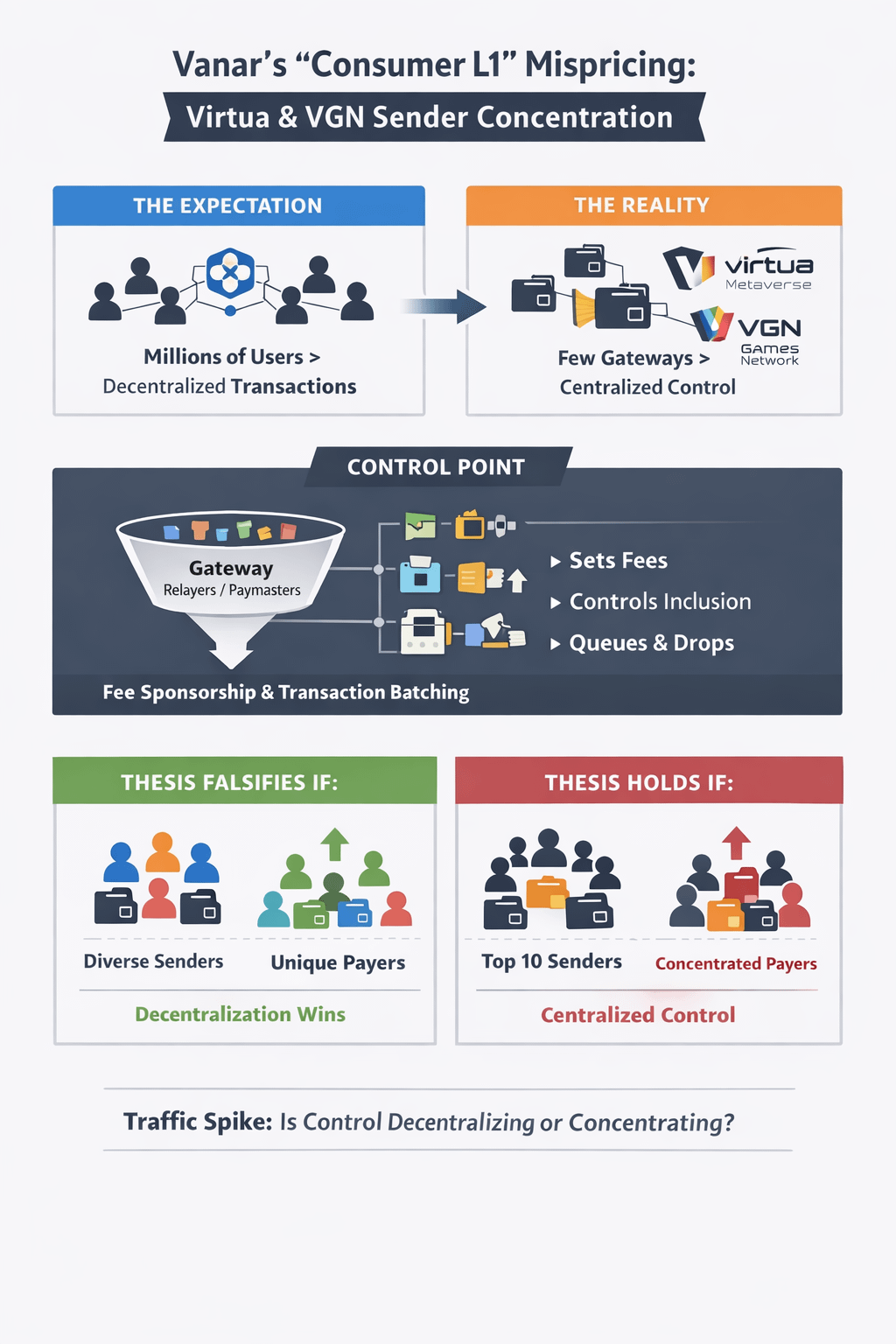

The market is pricing VANRY like it is the fee asset of a permissionless consumer chain where decentralization improves automatically as activity rises. I do not buy that. If Virtua and VGN are the throughput engines, the scaling path is not millions of end users originating transactions from their own wallets. It is a small set of sponsored or custodial gateways originating them, and that shifts the whole question to who actually pays gas and controls submission.

This tension shows up at the transaction sender address, not at the user account that owns an item or logs in. Consumer UX wants the user to stop thinking about fees, keys, and signing. Chain neutrality needs a wide base of independent originators because that is what makes censorship and pricing power hard in practice. Those goals collide at the same control point, the sender that pays gas and pushes state changes through the mempool.

If you are optimizing Virtua or VGN for conversion and retention, you sponsor gas, bundle actions, batch writes, recover accounts, rate limit abuse, and enforce policy at the edge. That is rational product design. The on-chain footprint is also predictable, more traffic routed through the same relayers or paymasters, more transactions sharing a small set of fee-paying sender addresses. That is where fee negotiation and censorship live, because the gateway decides what gets signed and broadcast, what gets queued, and what gets dropped or delayed.

Once that gateway sits in the middle, the fee market stops behaving like a broad auction and starts behaving like operator spend. The entity paying gas is also the entity controlling nonce flow and submission cadence, which effectively controls inclusion timing and congestion exposure. Users do not face blockspace costs directly, the gateway does, and it can smooth, queue, or withhold demand in ways a permissionless sender base cannot.

This is the hidden cost of mass onboarding when it is driven by entertainment products. You gain predictable UX and throughput smoothing, but you sacrifice the clean signal a permissionless fee token relies on. VANRY can look like a consumer fee asset on the surface while demand concentrates into a few operators that treat fees as an internal cost center and manage throughput as policy.

Where this fails is measurable in the exact moment adoption is supposed to prove the thesis. If Virtua or VGN hits a real usage spike and the top sender addresses stay a small share of transactions, and keep trending down while unique fee-paying addresses trend up, then my thesis breaks. That would mean origination is dispersing rather than consolidating under a gateway layer.

If the opposite happens, spikes translate into higher top-10 sender share, then the decentralization via adoption story breaks on contact with chain data. You can have high activity and still have a narrow set of entities that gate throughput and shape effective inclusion. At that point, VANRY behaves less like a broad-based consumer fee token and more like an operator input cost that can be optimized, rationed, and selectively deployed.

The uncomfortable implication is that the power shift is upstream of validators. Users get smoother experiences, gateways gain leverage, and the neutrality story gets thinner because control sits at the fee-paying sender layer. If you are pricing VANRY as if adoption automatically disperses control, you are pricing the wrong layer. Watch top sender share versus unique fee-paying addresses during the next major Virtua or VGN traffic spike, because that is where this either collapses or hardens into structure.