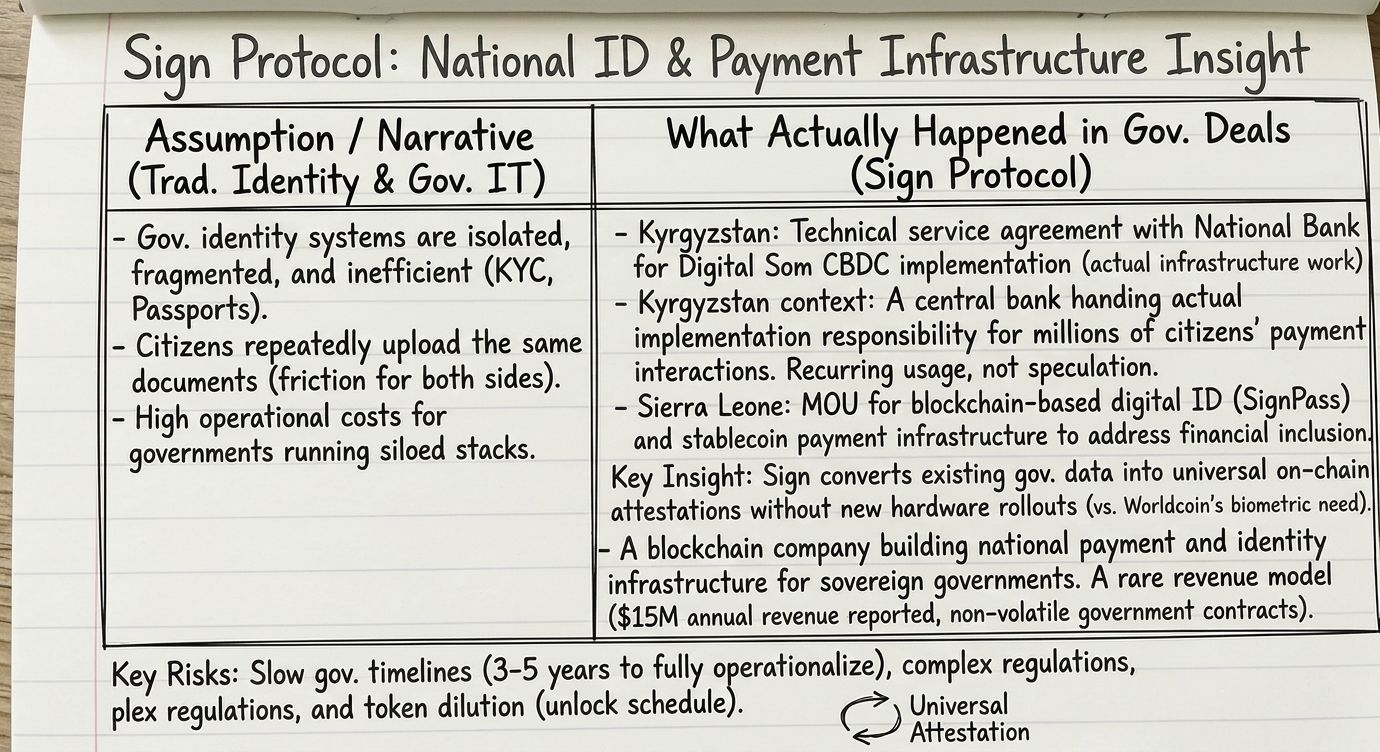

Doing CreatorPad task, I started looking at Sign properly after a conversation I had last month with someone who works in a government IT department. He was complaining about identity systems. Passport databases that don't talk to each other. Ministries running separate KYC stacks. Citizens re-uploading the same documents ten times for ten different agencies. The friction is invisible to most of us, but for governments it's a real operational cost.

Then I pulled up Sign's deployment list. UAE. Thailand. Sierra Leone. A technical service agreement signed with Kyrgyzstan's National Bank in October 2025. An MOU with Sierra Leone's Ministry of Communication in November 2025. I kept reading, wondering if these were vanity partnerships or actual infrastructure work. Governments don't hand over national systems easily. That stuck with me.

Sign isn't a DeFi project. It's not a yield farm or an NFT platform. The core product, Sign Protocol, is an omni-chain attestation layer. What that means practically is that any entity, a government, a bank, a DAO, can record a verifiable claim on-chain: "this wallet belongs to this citizen," or "this person passed KYC." The claim sits across multiple blockchains simultaneously. It can be read by any application that supports the standard. One attestation, universally readable.

The Kyrgyzstan deal is instructive. Sign signed a technical service agreement with the National Bank of Kyrgyzstan to help build the Digital Som, the country's CBDC. That's not a press release partnership. That's a central bank handing sign actual implementation responsibility. Kyrgyzstan has roughly 7.2 million citizens. Once the Digital Som runs, those citizens interact with Sign's infrastructure every time they use the payment system. That's a recurring, real-world usage loop that has nothing to do with crypto speculation cycles.

Sierra Leone is different but equally concrete. The MOU there focuses on two layers: a blockchain-based digital ID system and a stablecoin payment infrastructure. Sierra Leone's challenge is financial inclusion. Large portions of the population are unbanked. A verified on-chain identity becomes the on-ramp to financial services. No identity, no access. Sign's SignPass module solves exactly that bottleneck.

I keep comparing this to other Web3 identity projects I've looked at. Worldcoin does biometric identity and has scale, around 10 million verified users as of mid-2025. But Worldcoin's approach requires physical iris-scanning hardware. Government deployment of that infrastructure is expensive and slow. Sign's approach works with existing document-based credentials. Governments already have the passport data. Sign converts it into on-chain attestations without requiring new hardware rollouts. That's a much lower adoption barrier.

The tokenomics behind all of this are structured around a 10 billion total supply. At launch in April 2025, 12% entered circulation. 40% is allocated to community incentives. 20% to backers, with 48-month linear vesting and a 12-month cliff. The team takes 10% on a similarly long vesting schedule. The $12M token buyback executed in August 2025 removed around 117 million SIGN from circulation, roughly 8.7% of the supply at the time. That's a real supply tightening event.

What I find most interesting isn't the price action around these events. It's the revenue figure. Sign reported $15 million in annual revenue. In a space where most protocols are subsidizing activity with token emissions, $15M in actual cash revenue is rare. That revenue presumably scales with TokenTable usage, attestation volume, and government contract fees. Government contracts, unlike DeFi yield farm revenue, don't evaporate in a bear market.

There are real risks I'm not going to ignore. Government timelines are notoriously slow. The Digital Som was in development as of late 2025. Sierra Leone is still at MOU stage. Sovereign blockchain deployment involves regulatory complexity, parliamentary approvals, and procurement cycles that Web3 people fundamentally underestimate. Sign could have all the right technology and still see these contracts take three to five years to fully operationalize.

The token unlock schedule also adds pressure. 290 million SIGN tokens entered circulation in the October-November 2025 window. That's meaningful dilution against a relatively small float. Long-term holders can absorb it. Short-term traders can't always.

Still. A blockchain company building national payment and identity infrastructure for sovereign governments. That sentence exists. Worth thinking about what it means if execution actually works.

@SignOfficial $SIGN #SignDigitalSovereignInfra