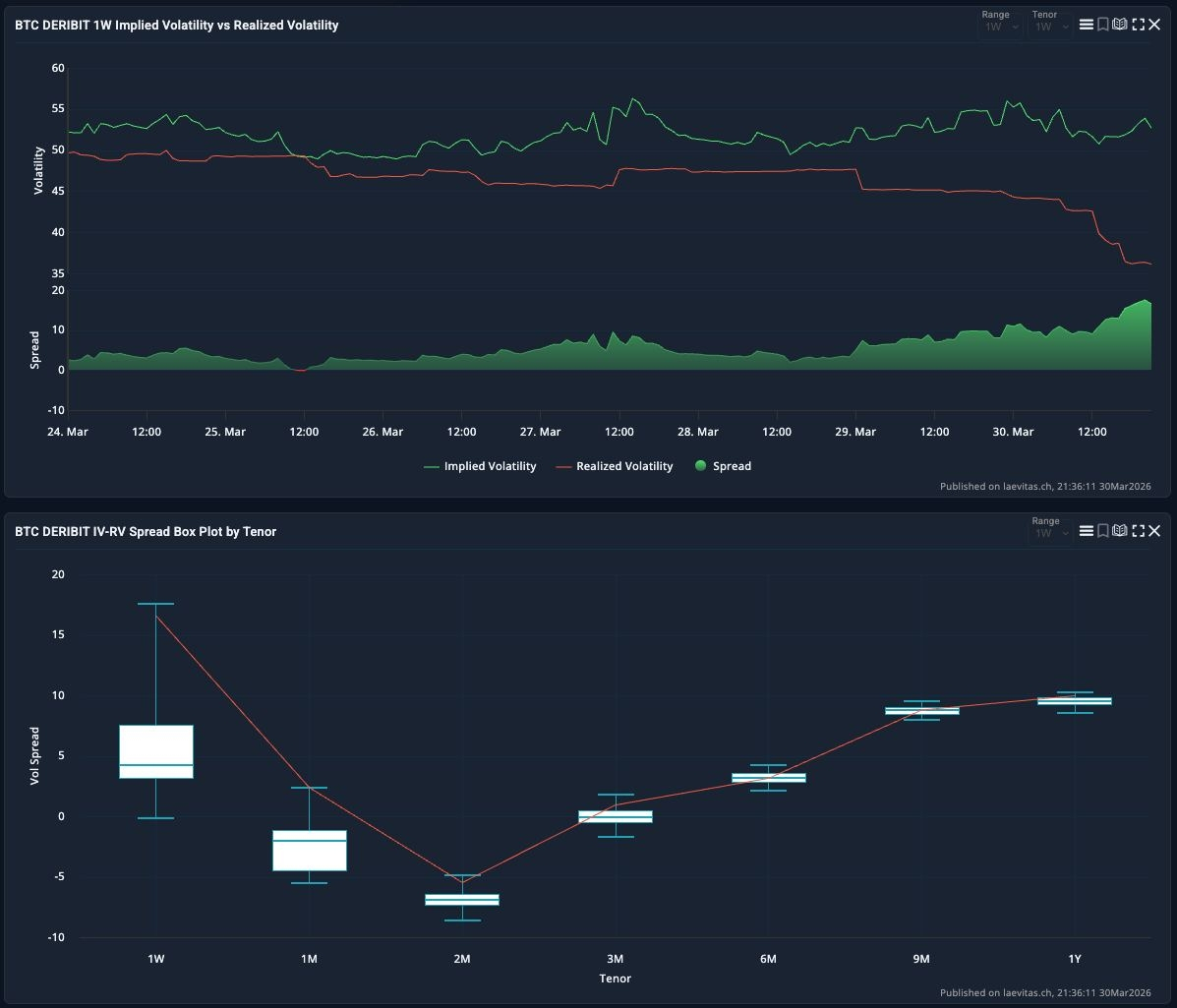

1️⃣ Volatility Dynamics: Compression and IV–RV Expansion Pressure

The $BTC options market is currently in a volatility compression phase, with short-dated Implied Volatility (1D, 1W) converging around ~50%. However, Realized Volatility (RV) has declined faster, pushing the IV–RV spread to ~+15 vol points (1W), indicating that the market is still pricing in more risk than currently realized.

With price moving sideways while IV remains elevated, theta decay becomes a significant drag on long volatility positions. This creates the need for a sufficient delta move to offset time decay, suggesting the market is coiling like a “volatility spring” ahead of a potential expansion.

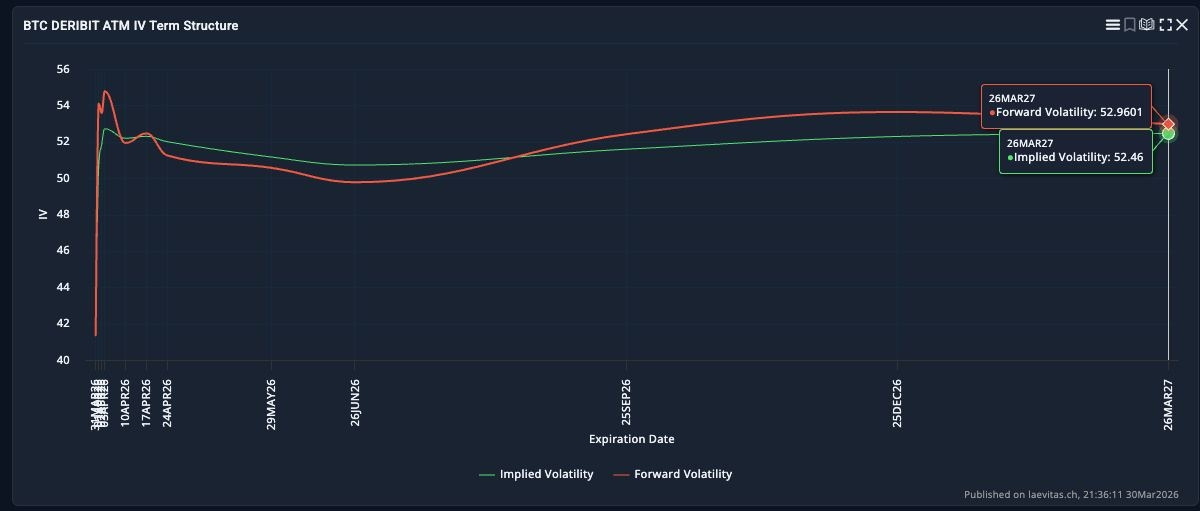

2️⃣ Term Structure & Forward Volatility: Risk Expectations Concentrated in April

The ATM IV term structure shows a mild contango, but with a clear bump in early April expiries (Apr 3–10) where IV is priced around 52–54%, indicating time-specific volatility expectations.

At the same time, forward volatility exceeds implied volatility across most tenors (long-dated ~52.96%), suggesting the market is pricing higher future risk vs current conditions. This implies the current sideways phase may be a build-up period ahead of a meaningful volatility move, likely centered in early April.

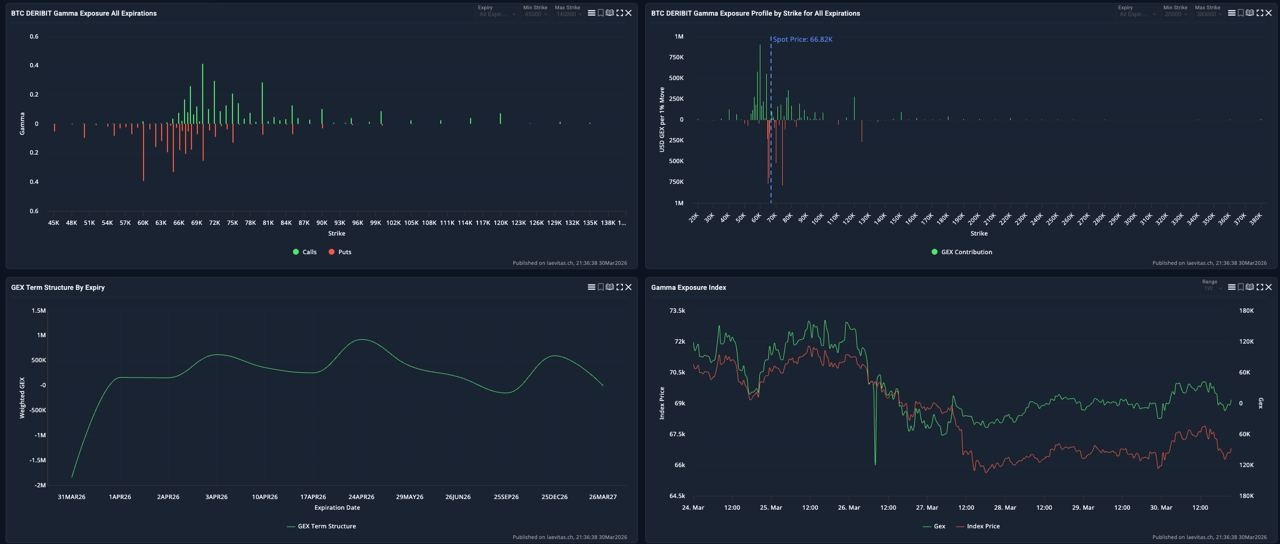

3️⃣ Gamma Exposure (GEX): Structure Driving Price Behavior

Gamma exposure is currently the key driver of short-term price action. Spot is trading around 66.8k, close to a positive gamma cluster at 70k, where market makers tend to sell into strength and buy into weakness, effectively pinning price and suppressing volatility.

Below 65k, the market shifts into negative gamma, with significant OI concentrated at 60k and 50k puts. In this regime, hedging becomes pro-cyclical, amplifying downside moves if price breaks lower.

From a term perspective, weighted GEX is ~ -1.8M (Mar 31) before flipping positive in April, implying short-term downside acceleration risk if a breakdown occurs, followed by potential stabilization afterward.

4️⃣ Skew & Dealer Positioning: Downside Hedging Pressure Builds

Beyond volatility and gamma, skew provides insight into market sentiment. Put skew is bid, especially below ATM, reflecting increasing demand for downside protection. This aligns with flow data, where volume and OI are concentrated in 60k–65k puts, indicating a clear preference for downside hedging over upside positioning.

In contrast, call skew remains relatively muted, suggesting upside convexity demand is still cautious and not leading the market.

From a dealer positioning perspective, current GEX suggests market makers are slightly long gamma around 70k, but would flip short gamma below 65k. In a long gamma regime, hedging is stabilizing and dampens volatility. However, once in short gamma, hedging becomes directional, accelerating both speed and magnitude of price moves.

This reinforces 65k as a key “gamma flip level”, where market behavior can shift from stability to volatility expansion, particularly to the downside.

🤔 Insight

The BTC options market is entering a transition phase, with conditions for volatility expansion increasingly in place: IV > RV, forward vol pricing higher future risk, and a clearly bifurcated gamma structure.

A break below 65,000 USD would likely push the market into deep negative gamma, where hedging flows could accelerate a move toward 60k–58k. Conversely, if price holds above this level, positive gamma at 70k should continue to pin price within the 68k–70k range, prolonging theta decay pressure.

Join our trading group for FREE signals, education, 1-1 support from our experienced traders: https://t.me/ +HWa2akmNUJo5OWQ1 (remove space), or follow us on X: TKR_Trading