I’ve been watching how corporate Bitcoin treasuries behave in this drawdown and the difference is clearer now.

I’ve been watching how corporate Bitcoin treasuries behave in this drawdown and the difference is clearer now.

It’s not about who believes in Bitcoin.

It’s about who can hold it without being forced to sell.

Nakamoto sold around 284 BTC below cost.

That’s not a sentiment shift.

That’s a balance sheet decision.

They needed liquidity for operations and restructuring. Bitcoin became the easiest asset to convert.

That’s the risk in debt-driven or operationally dependent treasury models.

Bitcoin is treated as a reserve in good conditions.

But under pressure, it becomes a funding source.

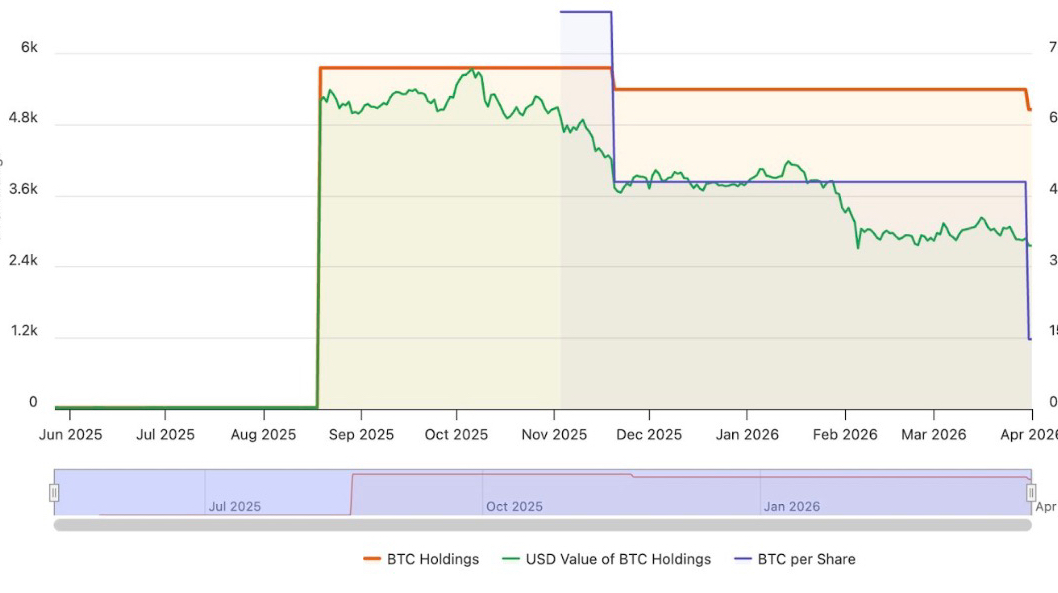

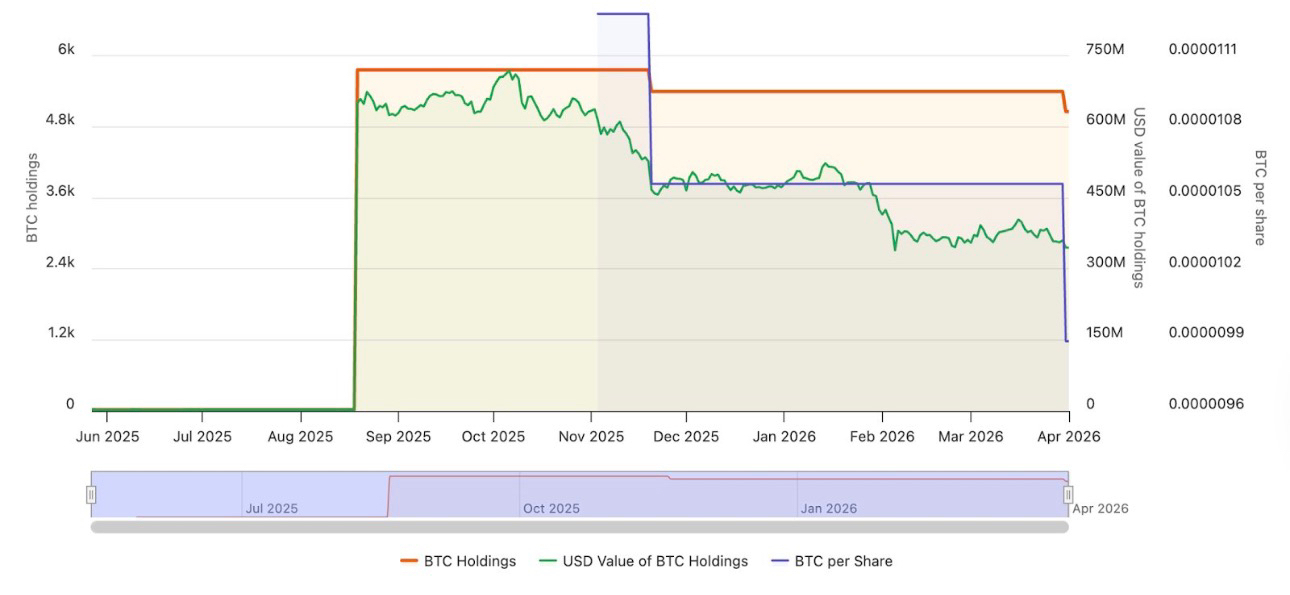

Now look at Strategy.

They didn’t buy this week.

But they didn’t sell either.

That matters more.

It shows they are not under immediate liquidity pressure. They can choose timing instead of reacting to it.

This is the real split forming.

Not bullish vs bearish.

But:

treasuries with control over liquidity

treasuries exposed to liquidity needs

The “never sell” narrative only works if your structure supports it.

If your treasury depends on cash flow, debt servicing, or external commitments, then Bitcoin is not a passive reserve. It’s conditional.

The New Hampshire Bitcoin-backed bond highlights the same issue at a different level.

Using Bitcoin as collateral for public financing introduces volatility into obligations that normally require stability.

A speculative-grade rating reflects that mismatch.

What’s happening now is not just price pressure.

It’s a structural test.

Bitcoin on a corporate or public balance sheet behaves differently than Bitcoin held individually.

This phase is showing which treasury models are stable and which ones rely on favourable conditions.

That difference only becomes visible when the market moves against them.

#USJoblessClaimsNearTwo-YearLow

#GoogleStudyOnCryptoSecurityChallenges $BTC