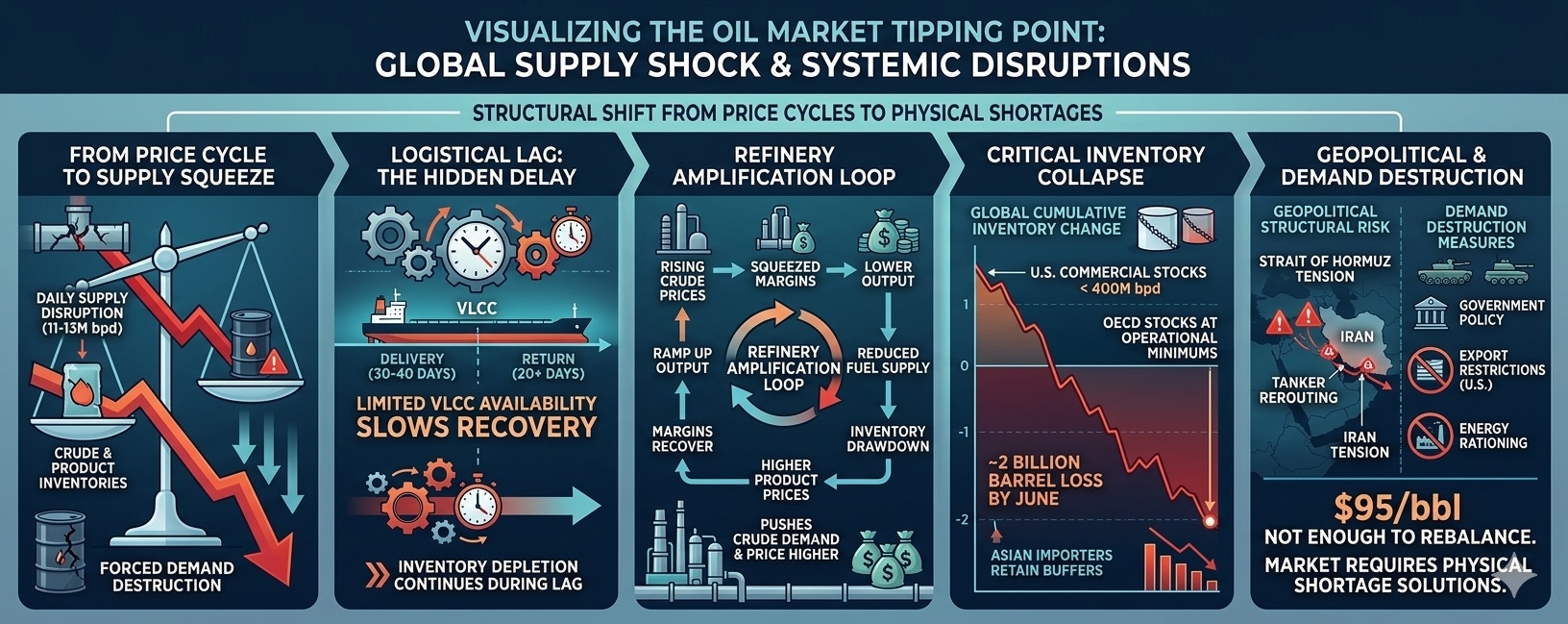

The global oil market appears to be entering a structurally different phase—one driven less by traditional price cycles and more by physical supply constraints and logistical delays. Recent developments suggest that what we’re witnessing is not simply a price rally, but the early stages of a systemic supply squeeze.

1. The Core Shift: From Price Cycle to Supply Disruption

Historically, oil markets rebalance through price:

Higher prices → lower demand

Lower prices → higher demand

However, the current situation challenges this framework. The issue is no longer just pricing—it's availability.

Key driver:

A daily disruption of 11–13 million barrels (a massive portion of global supply)

This creates three unavoidable outcomes:

Falling crude oil inventories

Falling refined product inventories

Forced demand destruction

2. The Hidden Variable: Time Mismatch in Supply Chains

Even if geopolitical tensions ease—especially around the Strait of Hormuz—the market will not instantly stabilize.

Why?

Oil transport relies on long-cycle logistics:

30–40 days for delivery

20+ days return time for tankers

Limited tanker availability (VLCCs) slows recovery

Inventory depletion continues even after supply resumes

➡️ This creates a lag effect, where shortages appear weeks after disruptions begin.

3. Refinery Dynamics: A Self-Reinforcing Price Cycle

Refineries are acting as a market amplifier, not a stabilizer.

Cycle in motion:

Rising crude prices → squeezed refinery margins

Lower refinery output → reduced fuel supply

Inventory drawdown → higher refined product prices

Margins recover → refineries ramp up again

→ pushes crude demand and prices even higher

This loop makes short-term equilibrium extremely difficult.

4. Inventory Collapse: The Real Signal to Watch

The market’s most critical indicator is no longer price—it’s inventory levels.

Projections:

Global cumulative inventory loss approaching ~2 billion barrels by June

U.S. commercial inventories potentially dropping below 400 million barrels

OECD stocks nearing operational minimum levels

At that stage:

Only a few countries (e.g., major Asian importers) retain buffers

Others must compete aggressively in the spot market

5. Geopolitical Risk: A Structural Threat

The tension involving Iran and control over the Strait of Hormuz is not just a temporary disruption—it’s a systemic risk.

Important implications:

Tanker traffic has already shown abnormal behavior (mass rerouting)

Supply routes are vulnerable to military escalation

Resolution is uncertain and may worsen before improving

This transforms oil risk from cyclical → geopolitical structural risk

6. Why $95 Oil Is Not Enough

A key conclusion:

$95 per barrel is insufficient to rebalance the market.

Reasons:

Supply gap is too large (11–13M bpd)

Logistics cannot recover quickly

Inventory buffers are being exhausted

At extreme levels:

Price loses effectiveness as a balancing tool

Market may enter a “physical shortage” phase

7. The Only Real Solution: Demand Destruction

If supply cannot recover fast enough, demand must fall.

This may come through:

Government policy interventions

Export restrictions (especially from the U.S.)

Reduced industrial activity

Energy rationing (similar to pandemic-era measures)

In essence:

The market may require forced demand suppression to restore balance.

8. Market Implications Beyond Oil

This scenario has broader consequences:

Inflation pressure across global economies

Increased volatility in equities and commodities

Stronger correlation between geopolitics and financial markets

Potential upside risk for energy-related assets

Conclusion

The oil market has likely crossed a critical tipping point. What lies ahead is not just higher prices, but a deeper challenge—managing a real-world supply deficit in a fragile geopolitical environment.

Investors and traders should shift focus:

From price targets → to inventory data and policy signals

From short-term moves → to structural supply risks

Because in this phase, the question is no longer “how high will oil go?”

—but rather “how will the shortage manifest?”