I still remember a cycle where the market treated every protocol dashboard like evidence of product-market fit. Transaction counts went up, social activity went up, token price went up, and everyone spoke as if the network had discovered gravity. Then the incentives changed, the marginal buyer stepped away, and the same charts looked like empty rooms with the lights on.

That memory matters here, because OpenLedger (OPEN) should probably not be read as just another AI attribution story. The cleaner version of the thesis is obvious: a blockchain for data, models, and agents, with monetization and provenance layered on top. But markets rarely pay for the clean version for long. They pay for the function that persists after the story becomes ordinary. The more interesting version is that OpenLedger may be reaching toward something harder and more economically charged: a system for managing AI memory, retention rights, attribution persistence, and controlled forgetting.

That is a very different business from “AI infrastructure.” It is closer to a market for the lifecycle of influence.

Markets get excited about AI because intelligence sounds expansive. But in economic terms, intelligence creates a new liability almost as often as it creates an asset. If a model absorbs data, fine-tunes on behavior, or inherits external signal, then the question is not only what it learned, but what it should continue to remember, what it must prove it remembers, and what it ought to forget when that memory becomes costly, stale, contested, or legally dangerous.

That’s where a project like OpenLedger becomes more interesting. Not as a static attribution layer, but as an attempt to create an operational memory market around AI systems.

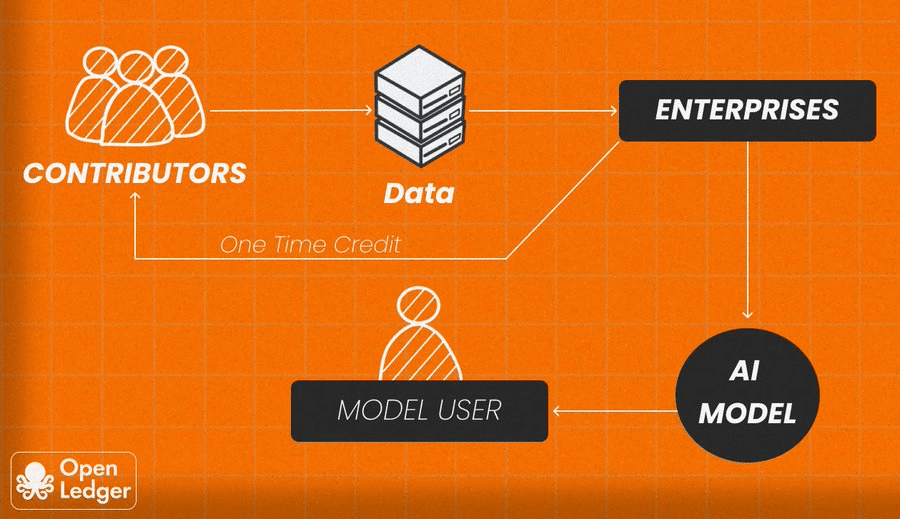

The first-order story is simple. Data contributors get paid. Model builders get access. Agents interact. Usage can be tracked, rewarded, and settled. In the mainstream framing, the protocol is about making AI more open and more economically fair. That framing is useful, but incomplete. The more important question is whether the network becomes the place where AI memory is made legible enough to trade, lease, dispute, expire, and reconstitute.

That loop matters.

Because if AI systems are going to be deployed in enterprise, regulated, or high-stakes environments, memory does not remain a purely technical variable. It becomes an economic one. Retaining model influence has a cost. Persisting attribution has a cost. Proving provenance has a cost. Defending against provenance disputes has a cost. And at some point, controlled forgetting may become a feature people are willing to pay for, not just a philosophical preference.

That is where token demand becomes more interesting than the usual “usage” story.

A token that merely facilitates access is easy to replace, especially if the system can abstract away payment into product-level UX. A token that underwrites memory persistence, rights management, dispute resolution, settlement, staking, or verification has a more durable claim on recurring activity. The market often undervalues this distinction because it focuses on initial adoption rather than maintenance. But infrastructure rarely dies because it lacks a narrative; it dies because its recurring economics are weak.

OpenLedger’s token question is therefore not whether the project can attract attention around AI. Plenty of projects can do that. The question is whether OPEN becomes part of a recurring economic sink tied to the maintenance of AI memory itself.

Think about what an AI memory market would imply. A model in production is not just producing inference; it is accruing a historical footprint. Training data may need to be referenced, licensed, updated, deprecated, or removed. An enterprise may need assurance that certain sources continue to count, or stop counting. A contributor may want attribution to persist even as model weights evolve. Another may want that influence to decay over time, either for legal reasons, accuracy reasons, or competitive reasons.

That creates a strange but plausible market structure: not just a market for access, but a market for the duration of influence.

Memory expiry as a concept is underrated. In traditional finance, decay, roll-off, amortization, and repricing are normal. In AI, the equivalent mechanism is still immature. Most projects talk about “ownership” or “provenance” as if those are settled states. But in practice, the more important economic variable may be persistence. What needs to remain visible? For how long? Who pays for that visibility? Who gets compensated when influence survives? Who pays when it should no longer survive?

If OpenLedger is serious, it may not be monetizing attribution alone. It may be building a market where memory itself has a carrying cost.

That is the hidden economic function.

And once you view it this way, the token model changes. The question becomes: what causes recurring demand for OPEN?

Not the concept of AI memory in the abstract. Concepts do not create durable demand. Systems do. Demand comes from actual maintenance behaviors: storage, proof, settlement, staking, verification, and dispute handling. If the protocol is the venue through which memory is retained, transferred, challenged, or expired, then OPEN can become a kind of operating currency for those lifecycle events.

That loop matters because lifecycle events are recurrent. New data arrives. Old data becomes stale. Models are retrained. Attribution claims are contested. Enterprises ask for compliance. Contributors want payment. Someone wants auditability. Someone else wants deletion. The system does not settle once and stay settled. It keeps needing maintenance.

This is the kind of demand that can survive speculation.

Liquidity tells its own truth. When a token’s liquidity is dominated by narrative rotation, the market is often valuing future attention, not future usage. When liquidity is tied to operational activity, the token tends to show a different texture: less explosive, more persistent, more resistant to headline-driven resets. That is why mature infrastructure tokens often look boring before they look credible. The market spends too much time asking whether the story is exciting and not enough time asking whether the token is necessary.

OpenLedger will have to prove necessity.

That’s where the risks start to accumulate.

The first is spoofed participation. AI infra projects are especially vulnerable to incentives that manufacture the appearance of utility. Data uploads can be farmed. Model calls can be routed through low-value activity. Attribution systems can be gamed by participants optimizing for rewards rather than quality. If the network rewards memory-related actions, then participants will try to manufacture memory-related actions. This is not a bug in crypto specifically; it is a feature of every subsidy-driven system. The market quickly learns to distinguish genuine usage from economically induced usage, even if it takes a while for price to reflect that distinction.

The second risk is verification complexity. Attribution persistence sounds elegant until one tries to prove it in messy conditions. What counts as a contribution? How does it survive transformations? How is influence measured after compression, adaptation, retraining, or retrieval augmentation? At what point does provenance become a legal dispute rather than a technical one? Systems that try to index reality often discover that reality is cheaper to use than to verify.

The third risk is enterprise friction. Enterprises do not buy conceptual purity; they buy reduced operational risk. If OpenLedger wants to matter in serious deployment settings, it must fit into workflows where procurement, compliance, security, and legal review all slow adoption. That can be fatal to protocols that depend on quick, reflexive ecosystem growth. A lot of crypto infrastructure is optimized for visible participation, not invisible integration. Enterprises usually want the opposite.

The fourth risk is token supply pressure. FDV pressure is not just a trading problem; it is an infrastructure problem. If a token has large future unlocks relative to organic usage, the market will treat every rally as inventory awaiting distribution. That is especially true in narratives where usage is still forming. OpenLedger may have to absorb a lot of supply before the market believes the economic loop is self-funding. If it cannot, then even good architecture can trade poorly for a long time.

Then there is the deeper pattern that breaks many infrastructure tokens: participation that is real on-chain but artificial in economic terms. Markets get excited about wallets, transactions, and integrations, but those metrics often include a high percentage of subsidized behavior. If the protocol has to pay people to care, then the system is not yet producing a durable maintenance economy. It is financing an attention phase. There is nothing inherently wrong with that, but investors should not confuse bootstrapping with durability.

The more interesting version is one where OpenLedger becomes necessary because memory is expensive to maintain and expensive to dispute. In that world, the protocol is not selling AI hype; it is managing the cost of persistence. That would create a different kind of token sink. Not one-time participation fees, but recurring costs linked to ongoing retention of influence, repeated verification, and active governance over what remains in the system and what decays out of it.

That is the kind of sink markets tend to underestimate early. They prefer visible usage over invisible maintenance. But maintenance is where infrastructure compounds. Fees tied to memory retention, dispute resolution, and attribution updates can matter more than flashy headline activity if they recur with each cycle of model retraining and enterprise compliance review.

Of course, this only works if the protocol can avoid becoming a centralized workflow disguised as decentralized coordination. The market has seen this before. A project starts with broad claims about openness and participation, but the actual operational dependency sits with a few core actors: a treasury, a foundation, a small set of validators, or a tightly managed commercial relationship. In that case, the token may still have some value, but the network’s durability is weaker than it appears. Dependency gets concentrated. Incentives narrow. Governance becomes cosmetic. The token becomes a proxy for centralized execution risk.

That is especially relevant in a memory-based thesis, because the harder the verification problem, the more likely the ecosystem will lean on trusted intermediaries. The more trusted intermediaries matter, the less “decentralized memory market” sounds like a pure protocol story and the more it starts to look like an institutional service layer with a token attached.

Still, the thesis remains compelling enough to take seriously. Not because it is obviously true, but because it matches a real and recurring economic problem. AI will create more data than humans can comfortably audit. Models will inherit more influence than users can intuitively track. Enterprises will want clearer rights, clearer retention, and clearer expiration rules. Someone will need to build the mechanism by which memory can be retained, priced, and eventually retired.

The market has not yet agreed on who gets paid for doing that.

That uncertainty is where OPEN lives. If the token becomes the medium through which AI memory is managed over time, then demand can recur for reasons deeper than speculation. If not, then the project risks becoming another elegant narrative attached to a token that only needs temporary enthusiasm to exist.

So the real issue is not whether OpenLedger sounds innovative. It is whether the network can turn memory into a maintenance economy, and maintenance into token demand, without letting incentives flood the system with fake participation or future unlocks overwhelm the market before the loop is proven.

If the future of AI includes not just remembering more, but paying to remember less, who capture

s that toll, and what exactly does OPEN need to be in order to collect it? @OpenLedger #OpenLedger $OPEN