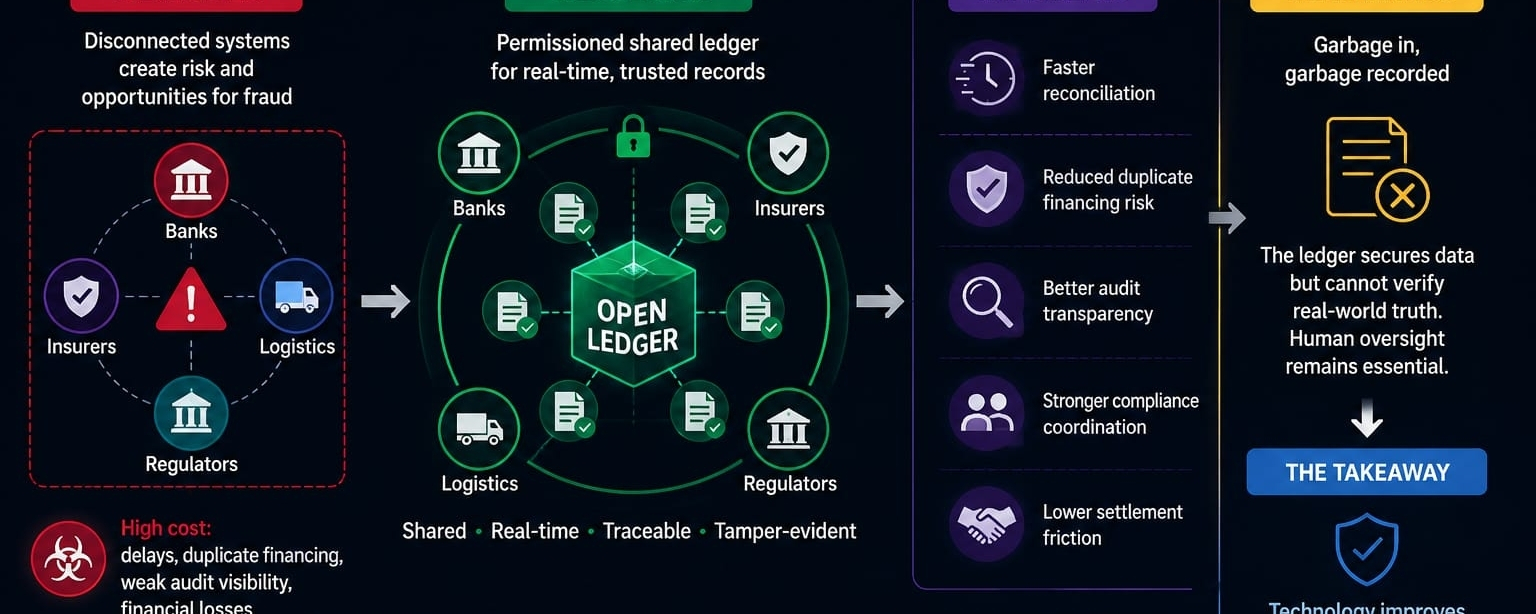

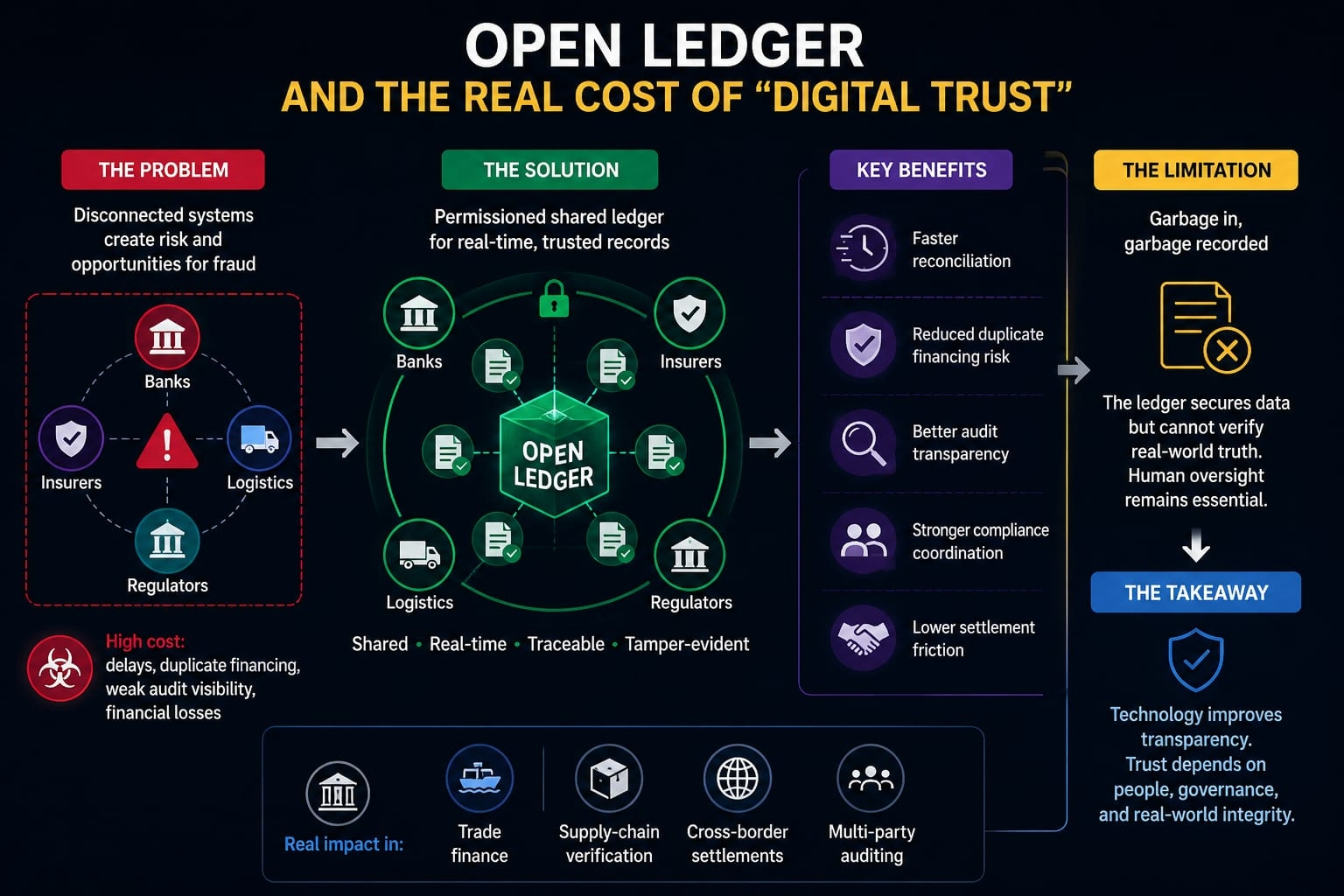

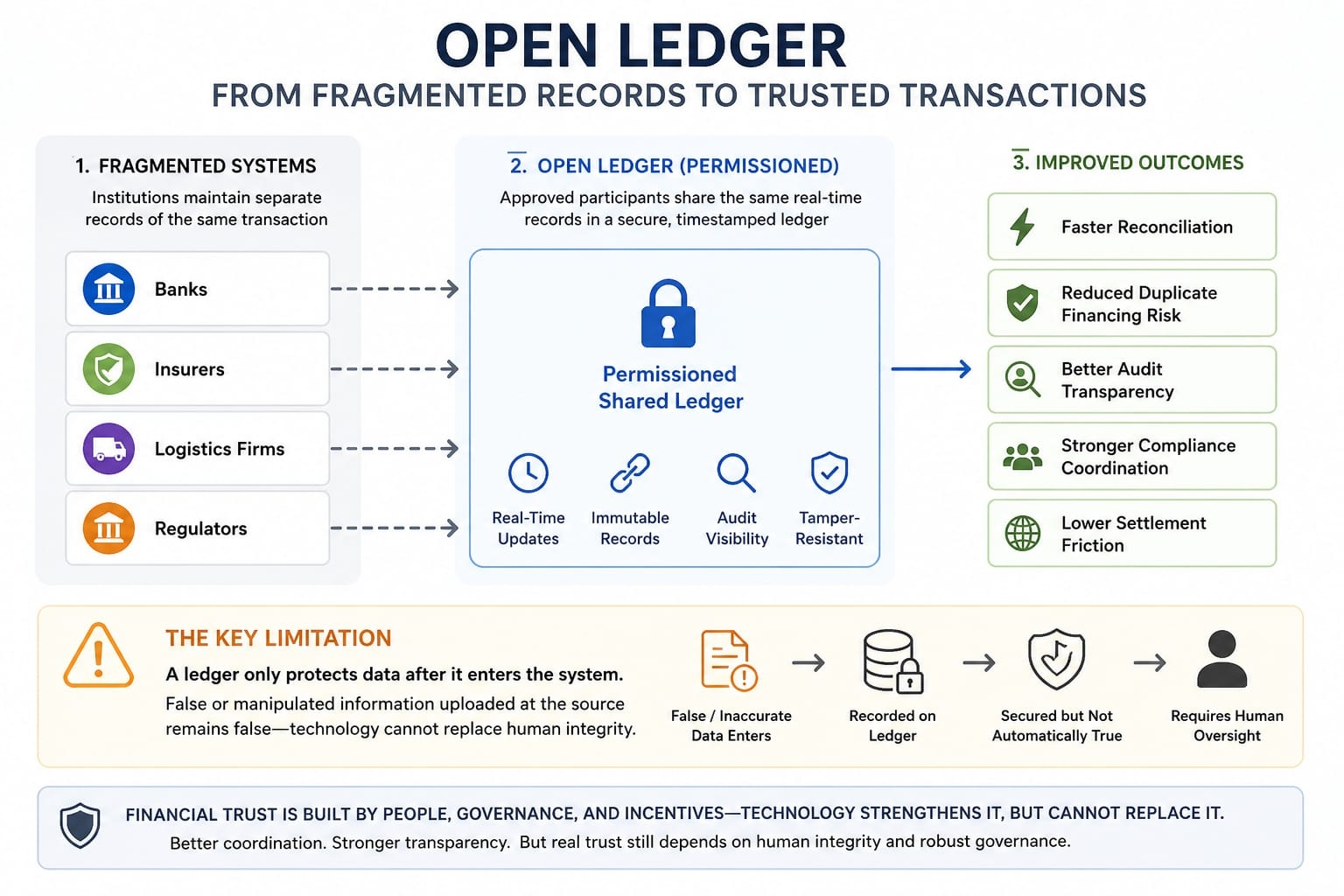

Open Ledger is built on a simple idea: financial fraud becomes easier when institutions operate through disconnected systems.

Banks, insurers, logistics firms, and regulators often maintain separate records of the same transaction. That creates reconciliation delays, weak audit visibility, and opportunities for manipulation.

This already costs the global financial system billions each year, especially in trade finance and cross-border settlements.

One well-known example was the Qingdao port scandal in China, where the same metal inventories were allegedly used multiple times as collateral because lenders relied on fragmented verification systems instead of shared records.

Open Ledger aims to reduce these risks through a permission-based shared ledger where approved participants access the same transaction history in real time. Every update becomes timestamped, traceable, and harder to alter without detection.

In theory, this can improve:

- Faster reconciliation

- Reduced duplicate financing risk

- Better audit transparency

- Stronger compliance coordination

- Lower settlement friction between institutions

Unlike public crypto networks, Open Ledger is designed for enterprise use rather than anonymous public participation. Access is typically restricted to verified institutions, regulators, and approved counterparties.

proves operational control, but there is an important limitation many blockchain narratives ignore:

A ledger only protects data after it enters the system.

If false invoices, manipulated shipment details, or inaccurate financial information are uploaded initially, the system does not automatically detect dishonesty. It simply preserves incorrect information more efficiently.

This is often called the “oracle problem” in enterprise blockchain systems — technology can secure records, but it cannot fully verify real-world truth without reliable human oversight.

And that matters because most major financial scandals were caused by incentive-driven manipulation, weak governance, regulatory failures, or poor risk controls — not simply outdated databases.

Even advanced systems still depend on humans for:

- Identity verification

- Data entry

- Compliance approvals

- Dispute resolution

- External auditing

There are also practical implementation challenges.

Most financial institutions still rely on legacy infrastructure built decades ago.@OpenLedger As a result, blockchain systems rarely replace existing operations completely. In many cases, they become an additional coordination layer on top of traditional systems.

That can create:

- Higher integration costs

- Longer deployment timelines

- Expanded cybersecurity exposure

- More regulatory complexity

Open Ledger promotes decentralization, but enterprise finance is rarely fully decentralized in practice. Permissioned networks still require governance rules, administrators, and institutional control over participation.

In reality, many enterprise blockchain systems operate as semi-centralized networks rather than fully open ecosystems.

Still, Open Ledger could improve transparency and operational efficiency in areas where fragmented records create real risk, especially in:

- Trade finance

- Supply-chain verification

- Cross-border settlements

- Multi-party auditing

The technology may improve coordination and audit visibility between institutions.

But financial trust has never depended on software alone.

Most financial collapses in history were ultimately driven by human incentives, governance failures, and deliberate manipulation — problems technology alone cannot fully eliminate.