▲ Core Conclusion: Institutions like BitMine are emulating the 'ETH Micro Strategy' (hoarding over 545,000 ETH worth $1.6 billion), driving a reassessment of Ethereum's ecological value. ETHFI, as the leader in re-staking, directly benefits from the explosion of institutional staking demand, currently priced at $1.21 is significantly undervalued, with a short-term target of $2.50 (+107%) and a long-term view of $8.00+.

🔥 1. The 'ETH Micro Strategy' Phenomenon: Institutional hoarding sparks staking demand

1. Scale of Major Entrants

- BitMine: Held 163,142 ETH ($500 million) in July, increased holdings by over 100% in three days, aiming to build an 'ETH Sovereign Treasury.'

- SharpLink: Holds 216,000 ETH ($643 million), claims to be the core of the 'Ethereum Hoarding Gentlemen's Alliance.'

- Overall Explosion: Institutions increased holdings by 545,000 ETH within a month, and ETFs saw a continuous net inflow of $4 billion over 12 weeks.

2. Strategic Logic

- Yield Enhancement: ETH staking annual yield of 6-8%, combined with re-staking rewards (like EigenLayer), resulting in a comprehensive APY of 13-15%.

- Regulatory Arbitrage: Trump policies abolishing SAB 121 reduce compliance costs for institutions.

- Deflationary Expectations: Ethereum L1 upgrades (zkEVM, sharding) accelerating ETH burn, daily destruction exceeding 1,000.

💎 2. Core Beneficial Logic of ETHFI: Institutional entry point for non-custodial staking

1. Technical Barriers: Addressing institutional pain points

- Non-Custodial Control: The only staking protocol that allows institutions to retain keys, avoiding custodial risks (e.g., Coinbase staking service facing SEC lawsuits).

- DVT Security Enhancement: Decentralized Validator Technology (DVT) reduces single point of failure risks, meeting institutional risk control requirements.

- Liquidity Token eETH: Supports instant conversion, DeFi reuse, enhancing capital efficiency.

2. Business Data Validation Growth Potential

💡 Catalyst: If BitMine entrusts 5% ETH to ETHFI staking (about 8,150 ETH), annual income increment of $2 million+.

📊 3. Reasonable Valuation: Current price is severely undervalued, triple model anchors target.

1. Relative Valuation Method (P/S Comparison)

- Industry Average P/S=3.2x: ETHFI annual income $12 million (transaction fees + sharing), reasonable market value $384 million → corresponding token price $3.33.

- Lido Benchmark Premium: ETHFI's TVL/Market Cap ratio is only 5.1x (Lido is 14.7x), with a valuation correction potential of 188%.

2. Cash Flow Discount (driven by incremental institutional staking)

- If institutional TVL reaches 30% ($1.86 billion), annual revenue increases to $50 million, valuation support at $8.00.

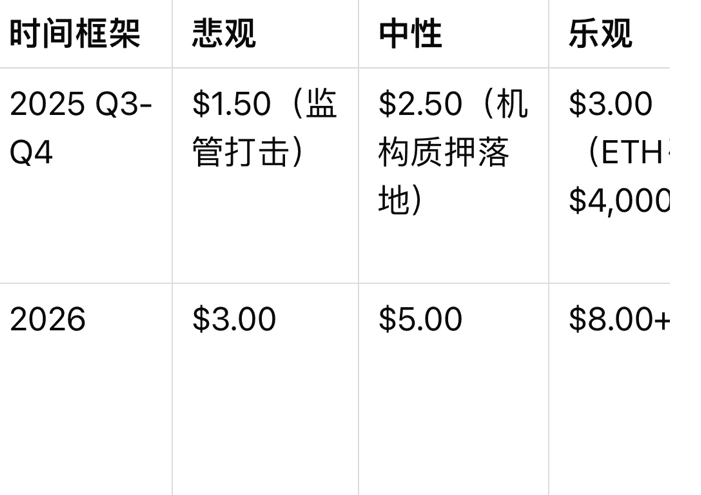

3. Scenario-based Price Range

💰 4. Investment Strategy: Build positions on dips, hedge risks

1. Position Management

- Current price $1.21, building position at 40%: P/S=1.0x is the lowest in the industry, with a correction potential >120%.

- Break through $1.50 to add up to 60%: In conjunction with institutional staking announcements or ETH breaking $3,200.

2. Risk Warning

- Token Inflation: 23.3% of tokens will be unlocked for the team in 2026, if not transferred to the staking pool or causing selling pressure.

- Competitive Product Diversion: If EigenLayer issues tokens, it may divert funds, requiring monitoring of its TVL changes.

> 📌 Ultimate Recommendation:

> Short Term: Keep a close eye on BitMine/SharpLink staking trends, event-driven market conditions are imminent;

> Long Term: ETHFI's technical moat (non-custodial + DVT) aligns with institutional needs, with all values below $5.00 being the value range.