In March 2026, the Hong Kong Monetary Authority officially issued the first batch of stablecoin licenses, Caixin.com. This news did not cause much of a stir in the crypto circle; instead, it felt like a stone dropped into a deep well—the sound was not loud, but the ripples were far-reaching. Many people did not realize that this means the floodgates for traditional financial institutions to enter crypto have been opened.

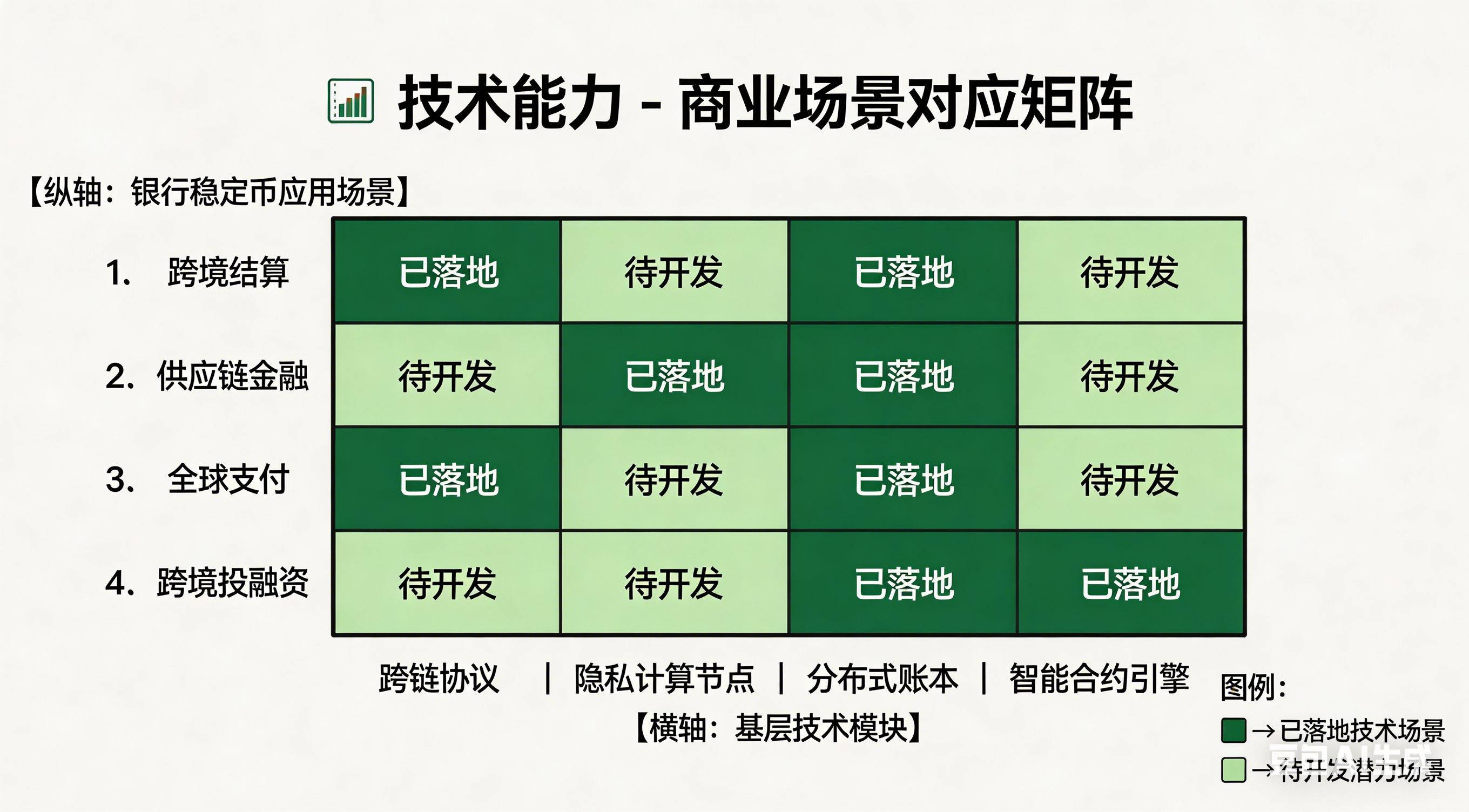

In the same month, @Sign Protocol announced the launch of the bank stablecoin integration middleware. At first glance, this feature seems unsexy, with no stories of a hundredfold return, and it’s not suitable for shouting trades on Twitter. But those who truly understand know that this is building bridges. For bank-issued stablecoins to be used across chains, a verification layer is needed, a compliance channel is required, and someone needs to connect traditional finance with on-chain liquidity. What Sign is doing is precisely this.

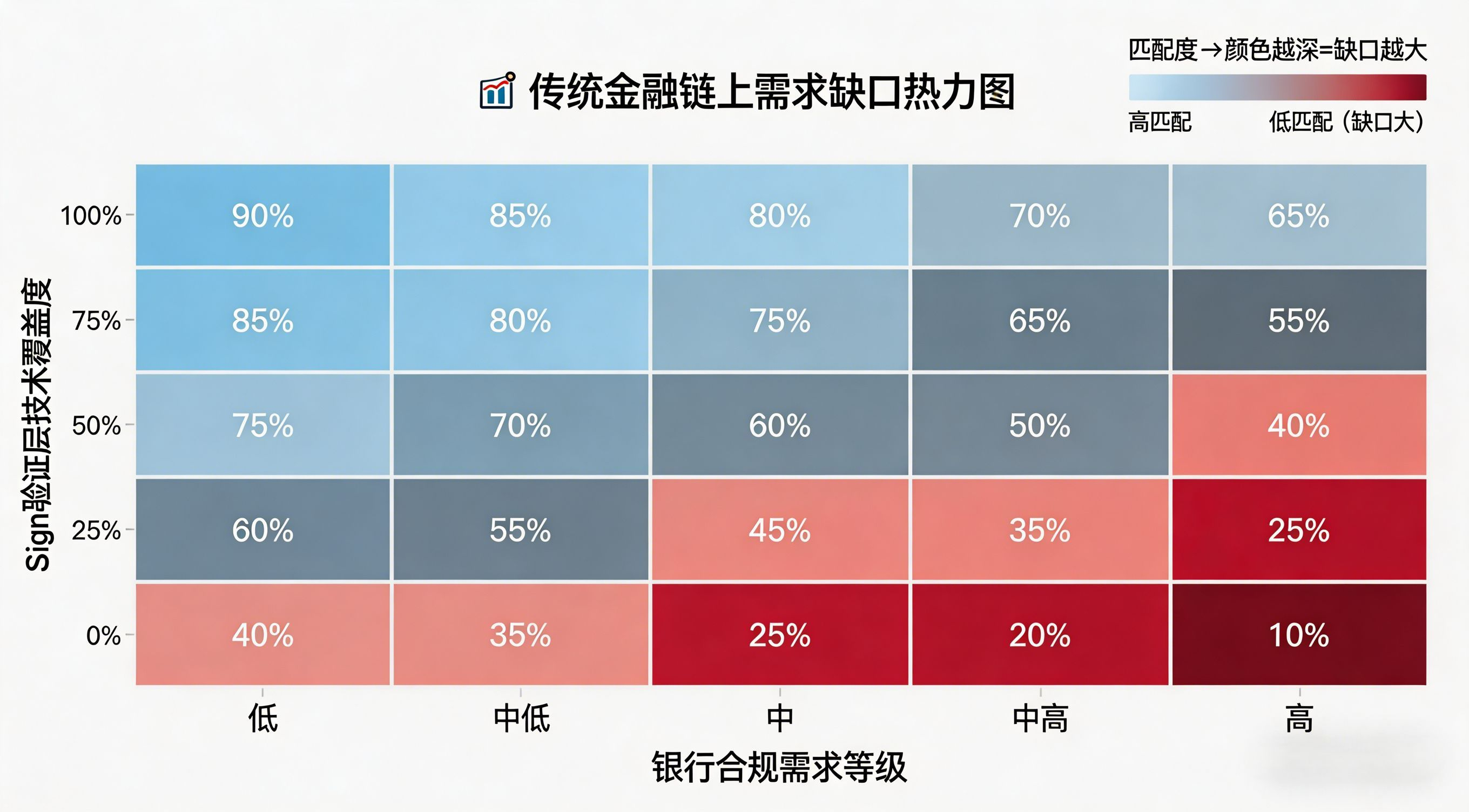

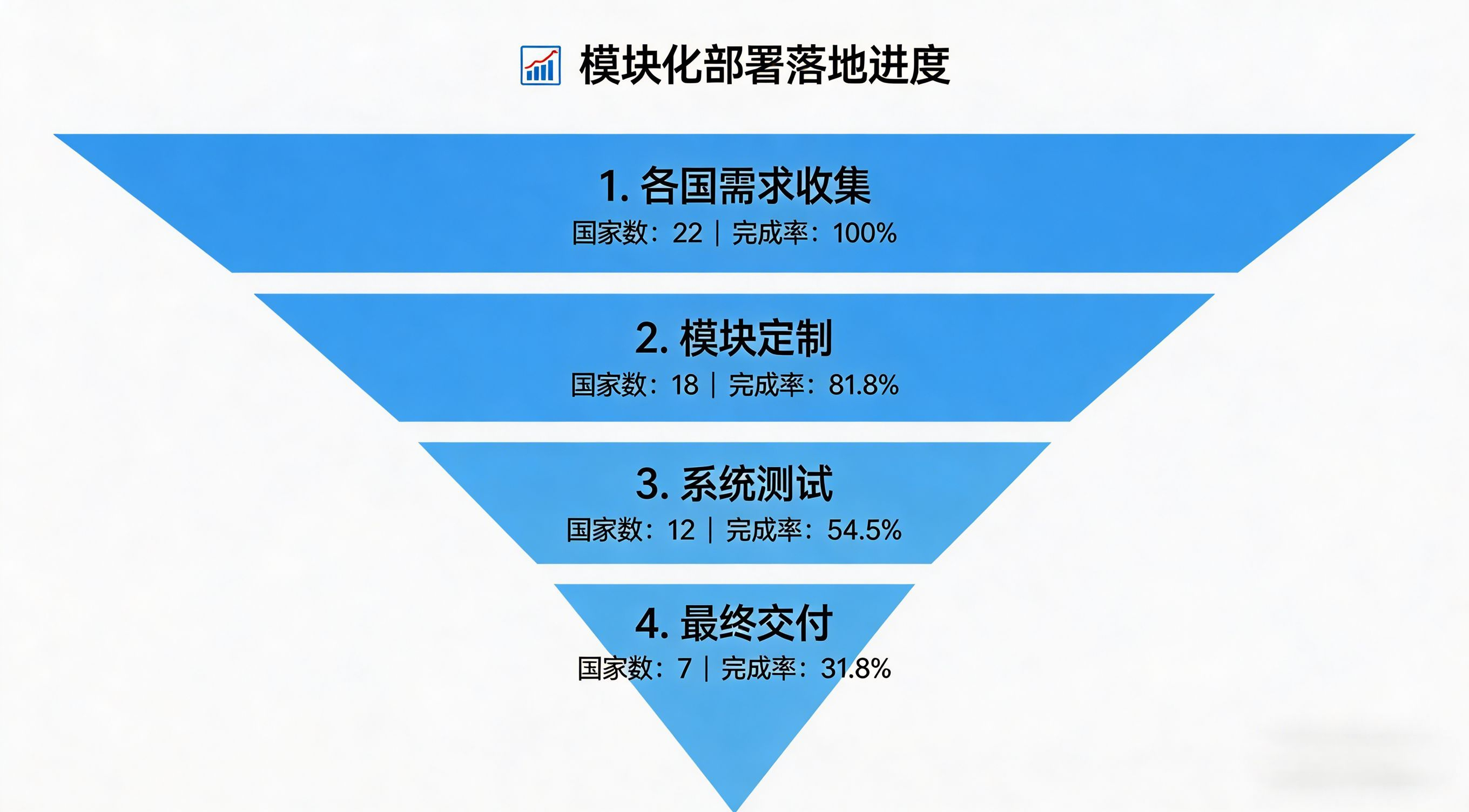

What deserves more attention is its S.I.G.N. architecture—a sovereign-level shared evidence layer. This design is clever, supporting CBDCs, stablecoins, and digital identity across multiple scenarios, allowing countries to deploy modules as needed without having to reconstruct the entire system at once. By 2026, over 130 countries worldwide will have been researching or piloting CBDCs, but there is one real issue that almost no one discusses publicly: can your digital currency system withstand geopolitical sanctions? Modular design gives sovereign nations options, which is the true necessity.

Someone asked, when will traditional banks issue stablecoins on a large scale? The answer may come faster than expected. Standard Chartered predicts that the U.S. stablecoin bill will pass by the end of the first quarter of 2026. Citibank reports that the total issuance of global stablecoins is expected to reach between $1.9 trillion to $4 trillion by 2030 on xrex.io. 90% of financial institutions have taken action regarding stablecoins, expanding from pilot programs to large-scale implementations. It is not a question of whether it will happen, but when it will happen.

The crypto industry has reached a stage of demystification. The market drivers of 2026 have shifted from 'halving narratives' to regulatory frameworks and institutional capital deployment on Futu Niu Niu. Protocols that rely solely on token inflation are starting to struggle, while projects with real business and stable cash flow are moving forward steadily. Sign chooses to serve governments and financial institutions, with long contract cycles and income not dependent on market sentiment fluctuations. This may seem conservative, but it is actually betting on a more certain future.

This layered architecture is not uncommon in other industries. Cloud computing has layers like IaaS, PaaS, and SaaS, while e-commerce has layers of infrastructure, trading platforms, and application services. The crypto industry also needs similar divisions—some issue tokens, some trade, and some quietly pave the way. It's just that in the past few years, those who issue tokens have garnered the spotlight, while those who pave the way have gone unnoticed.

The winds have changed now. The regulatory iron curtain has fallen, and privacy has become the ultimate battleground for cryptocurrencies in 2026. Decentralized identity and selective disclosure systems are beginning to take shape, allowing users to verify compliance status through zero-knowledge proofs without exposing specific transaction histories. This is precisely what Sign has been doing—verifiable credentials, cross-chain identity, compliance privacy.

This is not a sexy story, and there are no expectations of getting rich overnight. However, during market turbulence, projects that can survive and have stable businesses are more deserving of respect. True infrastructure is often laid by those who start building the roads before the wind comes. On the eve of banks entering the scene, they have finally been seen.