Table of contents

I. Core Conclusions (Qualitative First, to Avoid Directional Errors)

II. Issuance Structure (Standardized "Oil RWA Three-Tier Structure")

III. Issuance Path (Choose one of three or a combination)

IV. Valuation and Audit (Determining whether fundraising is possible)

V. Custody and Cash Flow (Core Compliance)

VI. Technical Architecture

VII. Issuance Execution SOP (Strict Timetable)

8. Exit Mechanism (A Decisive Factor in Whether LPs Invest)

IX. Key Risks and Hedging (Must be addressed upfront)

10. Final Standard Structure

XI. Key Recommendations

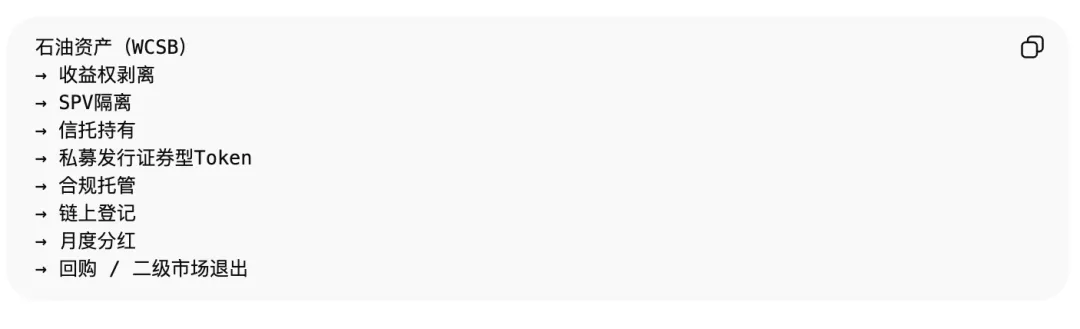

The entire process of compliant issuance of Canadian oil assets RWA—"regulation-structure-issuance-funding-exit"—has been streamlined, while key ambiguities (especially securities attributes, custody, valuation, and issuance path) have been tightened to enforceable, fundraising, and auditable standards.

A Huge Opportunity Behind 850,000 Oil and Gas Wells: Why Canada is Becoming a “Certainty Hotspot” for Global Energy Capital

I. Core Conclusions (First, define the nature of the issue to avoid directional errors)

1. In Canada, RWA (Rich Dollar Asset) is equivalent to securities (without exception).

According to the unified definition of Canadian Securities Administrators, it is classified as an Investment Contract and must be processed through securities law.

2. It's not "token issuance," but rather "cash flow securitization + on-chain registration."

Essentially similar:

> Oil Cash Flow ABS + Private Placement + Tokenized Register

3. The regulatory entry point is not a single agency, but rather a "four-tiered collaboration".

Dimensions, Institutional Regulators, Securities Regulatory Authority (Alberta Securities Commission), Unified Coordination, Canadian Securities Administrators, Energy Data (Alberta Energy Regulator), Financial Soundness, Office of the Superintendent of Financial Institutions, Taxation, Canada Revenue Agency

👉 If any one of these conditions is missing, the project will not be approved / will not be able to raise funds.

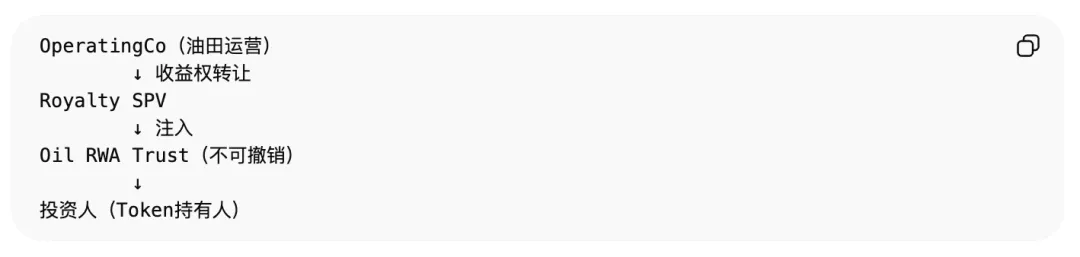

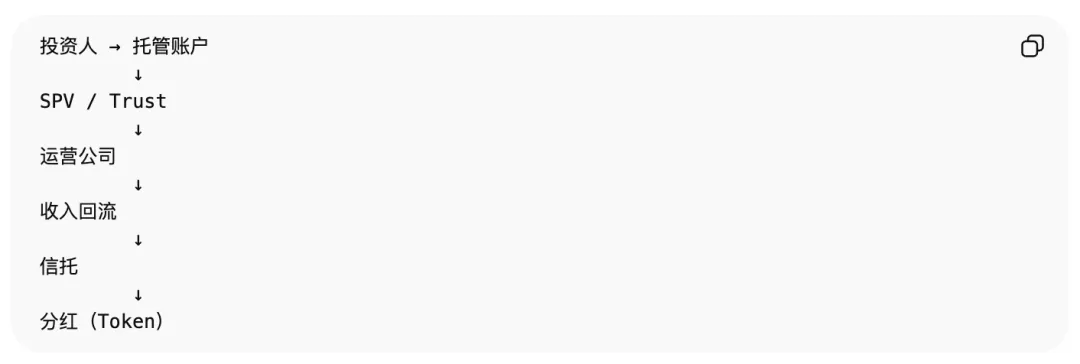

II. Issuance Structure (Standardized "Oil RWA Three-Tier Structure")

1) Underlying Asset Layer

The assets must meet the following requirements:

* Located in Western Canada Sedimentary Basin

* NI 51-101 Reserves Report (PDP-based)

* Produced ≥ 6–12 months ago

* Auditable cash flows

👉 Prohibited:

* Exploration assets

* Unproduced oil wells

* Resource reserves only (no cash flow)

2) Legal protection layer (SPV + Trust)

Standard structure:

Key requirements:

* Bankruptcy Remote

* Only the right to income is transferred, not the mining right.

* The trustee must be a licensed entity in Canada.

Recommended hosting:

Tetra Trust

3) Token Layer

Legal definition of Token:

> Beneficial Interest in Trust Cash Flow

That is: Trust beneficiary share certificates (on-chain registration form)

III. Issuance Path (Choose one or a combination of the three)

Path 1: Private Placement Exemption (Mainstream)

in accordance with:

* NI 45-106(Prospectus Exemption)

Target audience:

* Accredited Investors

* Family Offices

* Energy Funds

Features:

* ✔ Can be implemented quickly

* ✔ Lowest cost

* ✖ Liquidity Restricted (Lock-up Period)

Path 2: CSA Regulatory Sandbox

Apply through the CSA Regulatory Sandbox:

use:

* Test Token Transactions

* Relaxing some compliance restrictions

Applicable to:

Secondary Market Design

* Innovative structures (such as integration with DeFi)

Path 3: Project Tokenization (Strongly Recommended)

CSA Official Implementation Plan:

* Direct communication structure with regulators

* Get Exemptive Relief

* Lock in regulatory attitude in advance

👉 Practical suggestions:

Participation is mandatory (otherwise, the later approval costs will be higher).

IV. Valuation and Audit (determining whether fundraising is possible)

1) Reserves assessment (mandatory)

use:

* GLJ Petroleum Consultants

* Sproule Associates

standard:

*IN 51-101

* PDP / 2P splitting

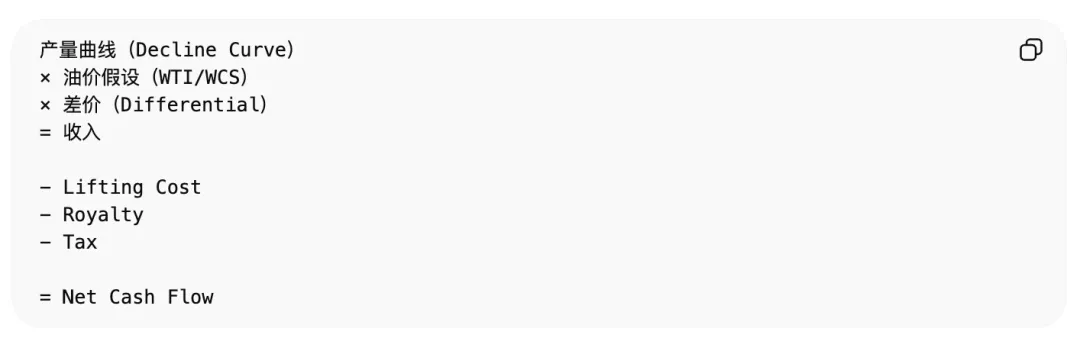

2) Cash Flow Model (Core)

Must include:

3) Valuation system (three investment banking-grade systems)

👉 Token pricing must be anchored:

Discounted cash flow (DCF), not oil price

V. Custody and Cash Flow (Core Compliance)

1) Closed-loop funding mechanism (must be achieved)

2) Stablecoin/fiat currency system

recommend:

* CAD stablecoin (regulated by OSFI)

* Or bank channels (RBC / ATB)

Involved organizations:

* Royal Bank of Canada

* ATB Financial

3) Custody Standards (CIRO Requirements)

in accordance with:

* Canadian Investment Regulatory Organization

Require:

* Cold storage

Multiple signatures

* Audit traceability

VI. Technical Architecture

in principle:

👉 Law first, technology later

Recommended solution

1) Compliance Chain

* Polymesh (preferred)

or

* Hyperledger Fabric

2) Core Module

* Investor Whitelisting(KYC)

* Token Registry (Authorization)

* Distribution Engine (profit sharing)

* Compliance Transfer

3) Oracle data

Connection required:

* AER production data

* Oil price index

* Sales Contract

VII. Issuance and Implementation SOP (Strict Timetable)

Phase 1 (0–60 days): Assets and Legal Matters

* Reserves Report (NI 51-101)

* SPV + Trust Establishment

* Legal Opinion

Phase 2 (60–120 days): Regulation and Structure

* ASC Communication

* CSA Tokenization Application

Private equity firms are exempt from filing requirements.

Phase 3 (120–180 days): Technology and Release

* Token Deployment

* Hosting and Integration

* Roadshow + Fundraising

Phase 4 (180+ days): Operations

Monthly bonus

Quarterly Audit

* Annual valuation

8. Exit Mechanism (A Decisive Factor in Whether LPs Invest)

It must be written into legal documents:

1) Buyback mechanism (mandatory)

text

Repurchase price = NAV or target IRR (8–12%)

2) Secondary Market

* Compliant Digital Securities Platform

* Or related sections of TSX Venture

3) Asset Sale

Sold to:

* Oil and gas companies

* PE Fund

IX. Key Risks and Hedging (Must be addressed in advance)

10. Final Standard Structure (can be directly written into BP)

XI. Key Recommendations

"Compliance Framework," with three key enhancements:

1) From "Path Description" → "Structure Locking"

✔: Legal Definition of SPV + Trust + Token

2) From "Understanding Regulatory Oversight" to "Issuance Capability"

✔ :

* Private Placement Structure

* Investor Types

* IRR Logic

3) From "technology-oriented" to "cash flow-oriented"

✔ :

The core issue is cash flow, not the supply chain.

If your next step is to truly implement it

These three parts are very important:

1) Fundraising version (most important)

* IRR model (including oil price sensitivity)

* Hierarchical structure (Senior / Mezz)

* Investment Terms (Lock-up/Repurchase)

2) Legal document package

* PPM (Private Placement Prospectus)

* Trust Deed

* Token Terms

3) Valuation Model

* NPV10 / PDP NAV

* Can be used directly for SPAC / RWA

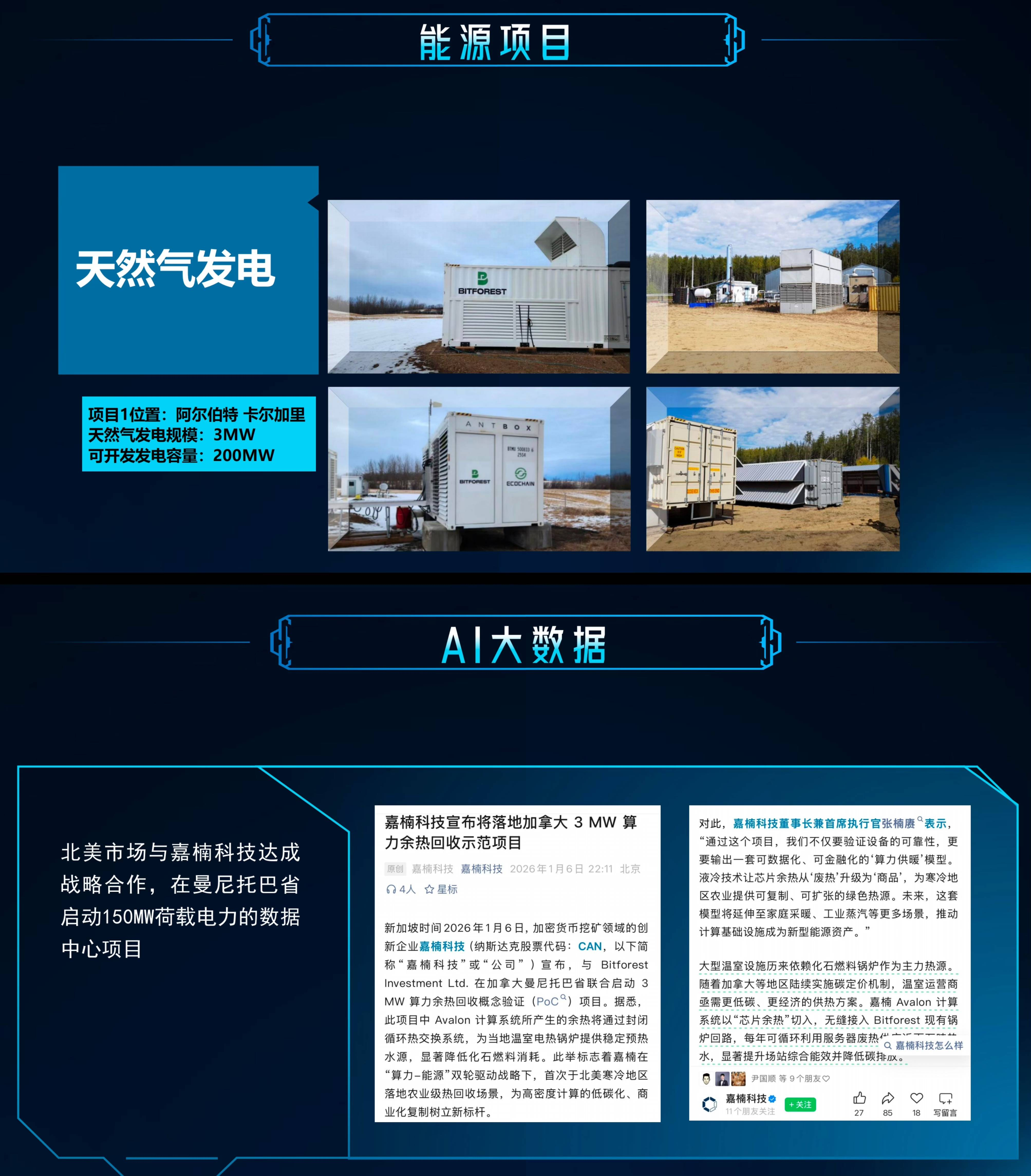

The following are the cooperative business opportunities in Canadian oil and gas exploration:

Add WeChat VCBLO1 (please include your name and collaboration needs in your message).