$NEAR From a technical standpoint, $NEAR seems to be approaching a potential breakout to the upside. Notably, there is strong fundamental expansion occurring across its ecosystem, which has yet to be fully reflected in the token's price.

The mismatch between growth and valuation could present an opportunity for the market to correct this imbalance. As a result, assets like $NEAR might outperform Bitcoin significantly if Bitcoin continues its bullish trend.

As I noted earlier, once key resistance levels are breached, protocols like $NEAR are well-positioned to accelerate and capture momentum.

$NEAR looks incredibly undervalued when you examine its fundamentals. One key factor is that its entire token supply is already circulating, and its design favors active participants in the ecosystem over passive holders. On top of that, the intersection between AI and crypto has yet to gain much attention, but that's often where the biggest opportunities arise.

Currently, $NEAR it has a valuation of around $1.7 billion. That number might not seem small at first glance, but the underlying growth story adds important context.

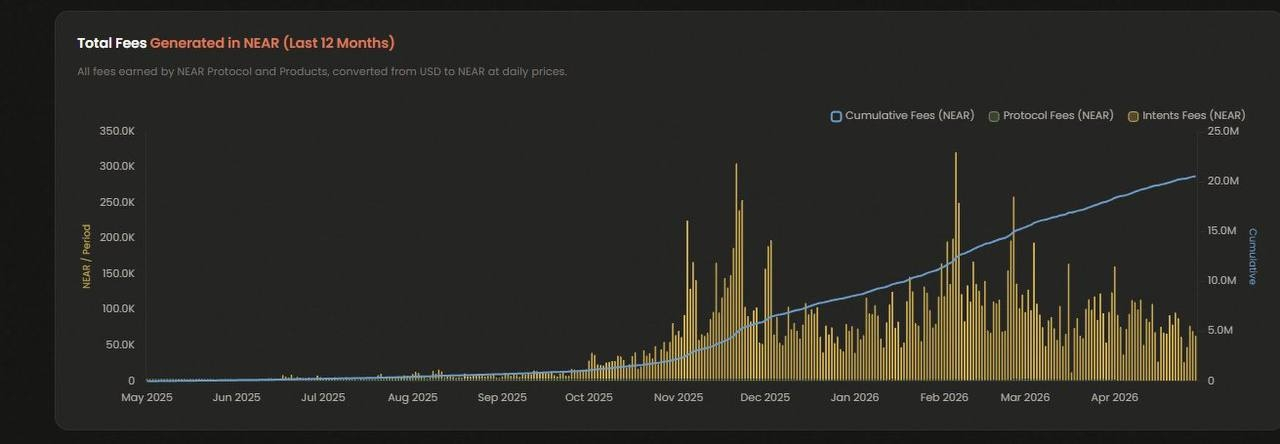

In just the first 4 months of 2026, the network generated revenue of around 12 million $NEAR, equivalent to about $15.6 million. When annualized, this puts 2026 on track for revenue of about $40-60 million. By comparison, total revenue before 2026 was around $10 million, indicating a significant acceleration even in tough market conditions.

If you extend that trajectory forward, the potential growth curve might look something like this:

2025: $10 million

2026: $50 million

2027: $150 million

2028: $300 million

2029: $450 million

2030: ~$585 million

That would place revenues in the $500-600 million range by 2030.

To put the valuation into perspective, $NEAR is currently trading with a price-to-sales ratio of around 34X. A comparable figure is higher elsewhere, with Solana around 40X, while Ethereum approaches 200X. Even traditional Web2 companies often hover in the 15-30X range, although some AI-focused companies like OpenAI or Anthropic have much higher multiples despite generating less revenue.

If NEAR maintains this expansion rate, a higher valuation multiple becomes increasingly justified. Even assuming the current ratio remains stable, growth alone could support returns of 10-15 times over the next 4 years.

Overall, this suggests that the market may still be underestimating both the project's revenue trajectory and its long-term position.