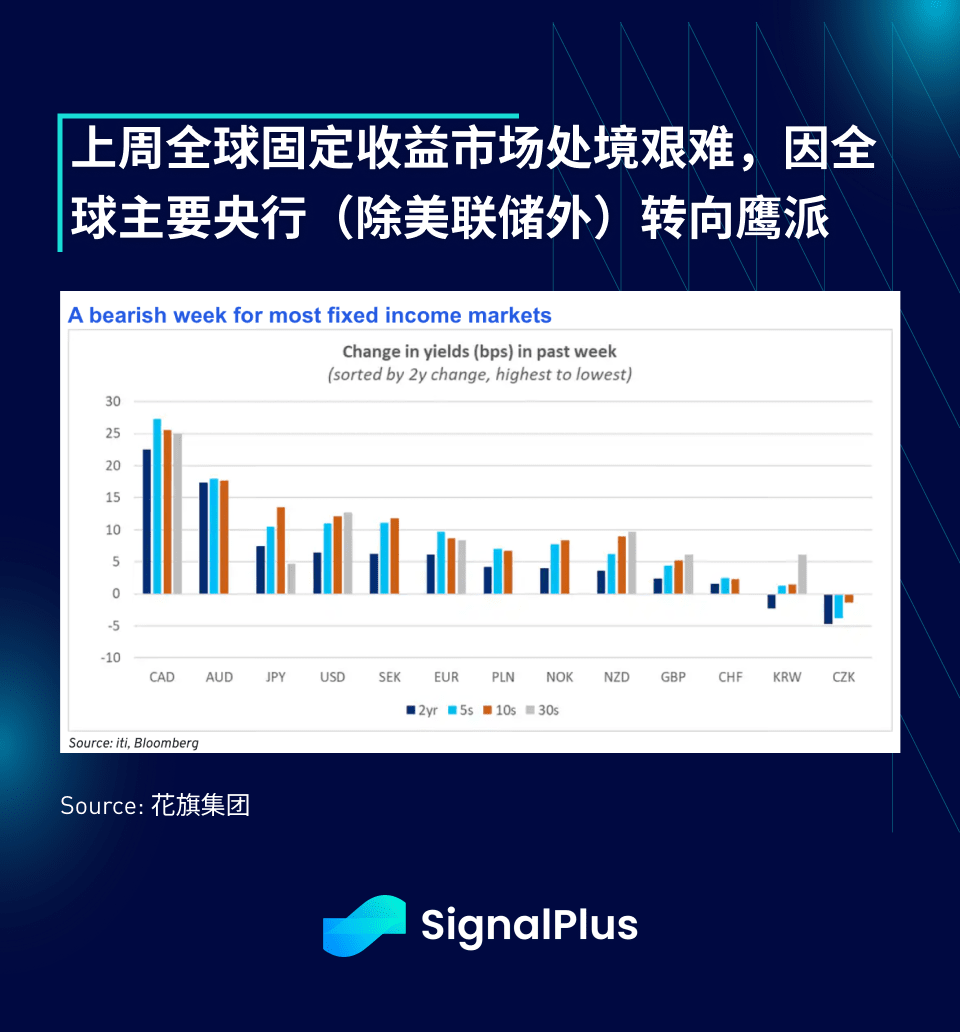

Despite the risk sentiment stabilizing last week, the G7 fixed income market had a tough week as multiple non-U.S. leading economic data points unexpectedly improved. Australia's CPI rose 3.8% year-on-year, exceeding the expected 3.6%, leading to a 15 basis point jump in its 5-year government bond yield, with the Australian dollar rising 2.5% against the U.S. dollar that month. Following this was Canada's employment report, which was extremely strong, far exceeding expectations (unemployment rate at 6.5%, expected 7.0%), triggering the most severe single-day volatility in Canadian 5-year government bonds since 2022 (+20 basis points), with the Canadian dollar surging 2%. In Japan, despite soft capital expenditures, the market is pricing in a 90% probability of the Bank of Japan raising interest rates this month, making the dovish Fed appear out of place in the G7.

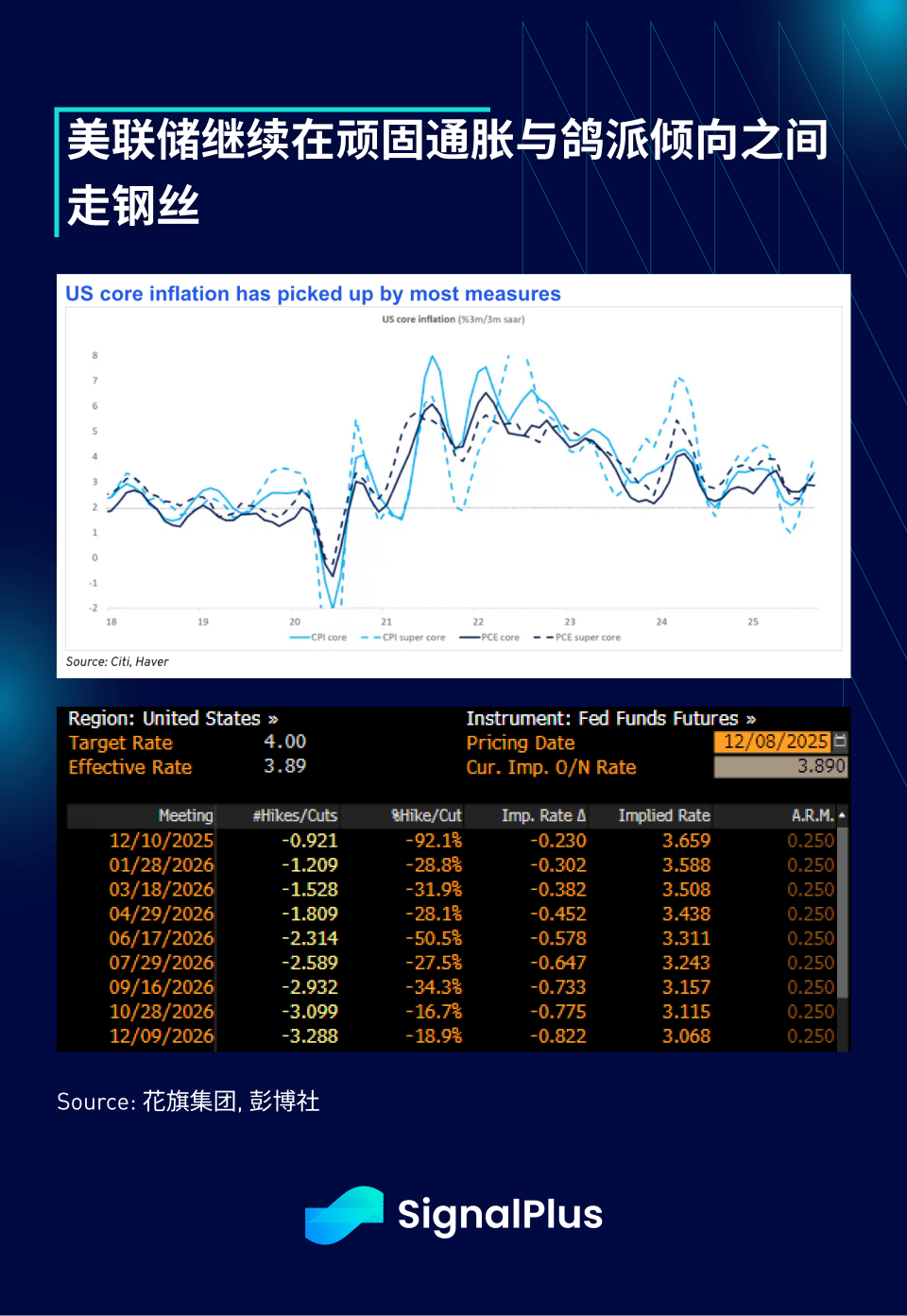

The market widely expects the Federal Open Market Committee (FOMC) to cut rates by 25 basis points this week and anticipates two more cuts throughout 2026. Despite stubborn inflation, the Fed has hinted it will use the weakness in the unemployment rate (around 4.5%) to justify its final rate cut of the year. Additionally, considering that there are two employment reports due between the December and January FOMC meetings, we expect Chair Powell will retain the flexibility to cut rates again in January or March, while the 'dot plot' forecast for 2026 may be similar to the previous one.

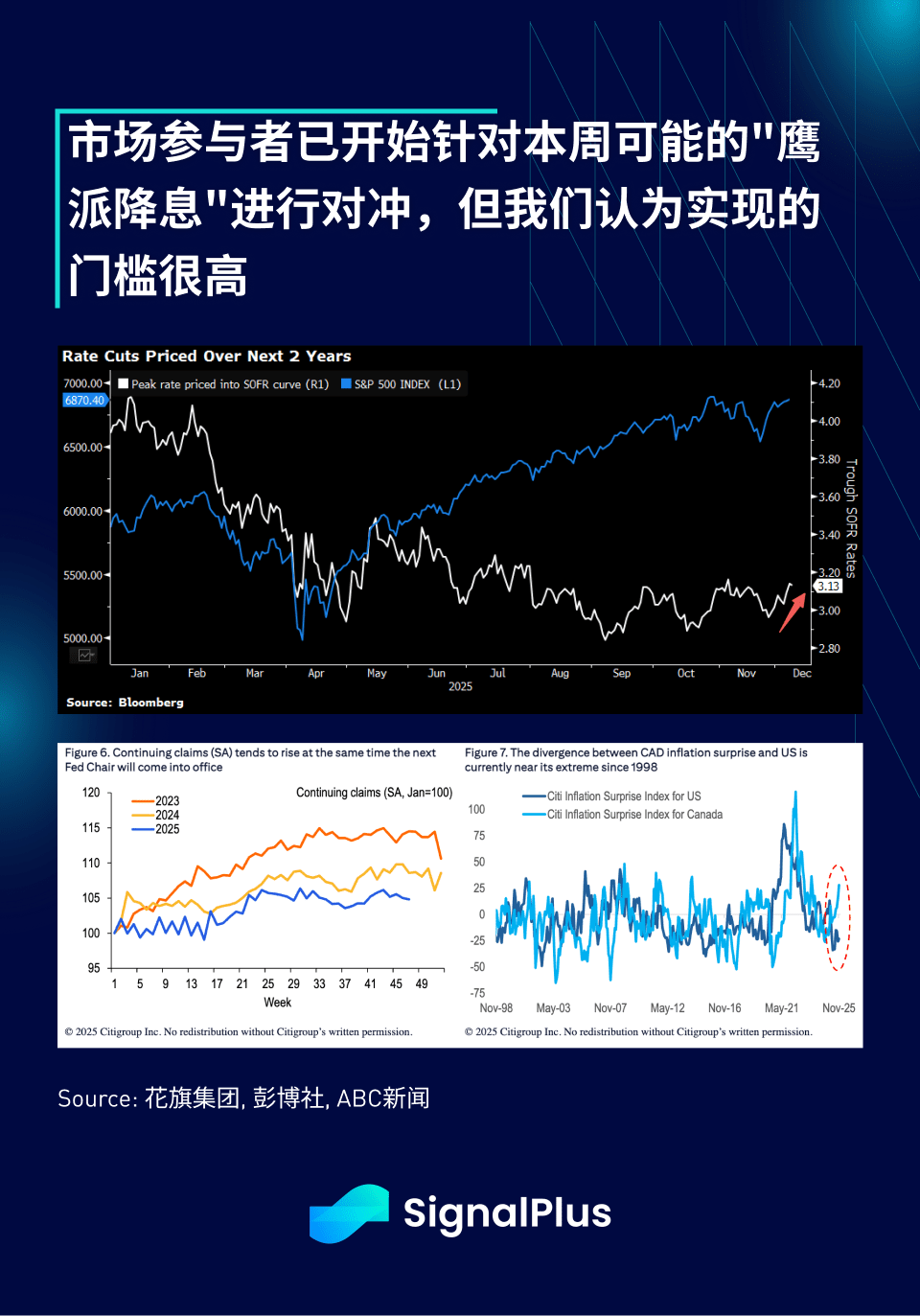

As expected, the Federal Reserve's dovish stance is starting to encounter some market resistance, as market participants begin to price in the possibility of 'hawkish rate cuts' based on Powell's guidance during the Q&A session or expectations of potential changes in the Summary of Economic Projections (SEP). To achieve this, the Federal Reserve needs to express itself very clearly in forward guidance, such as adjusting the rate cut expectations for 2026 to once or less, but we believe the probability of this happening is low.

On the other hand, President Trump has strongly hinted that Kevin Hassett may become the next Federal Reserve Chair, which is likely a common expectation in the market, meaning that starting from June next year, a 'more accommodative' Fed Chair will take the helm. Therefore, in the medium term, the views on 1) a weaker dollar, 2) rising inflation, 3) a steepening U.S. Treasury yield curve, and 4) rising asset prices are likely to remain unchanged unless there are significant changes in the realized macro conditions.

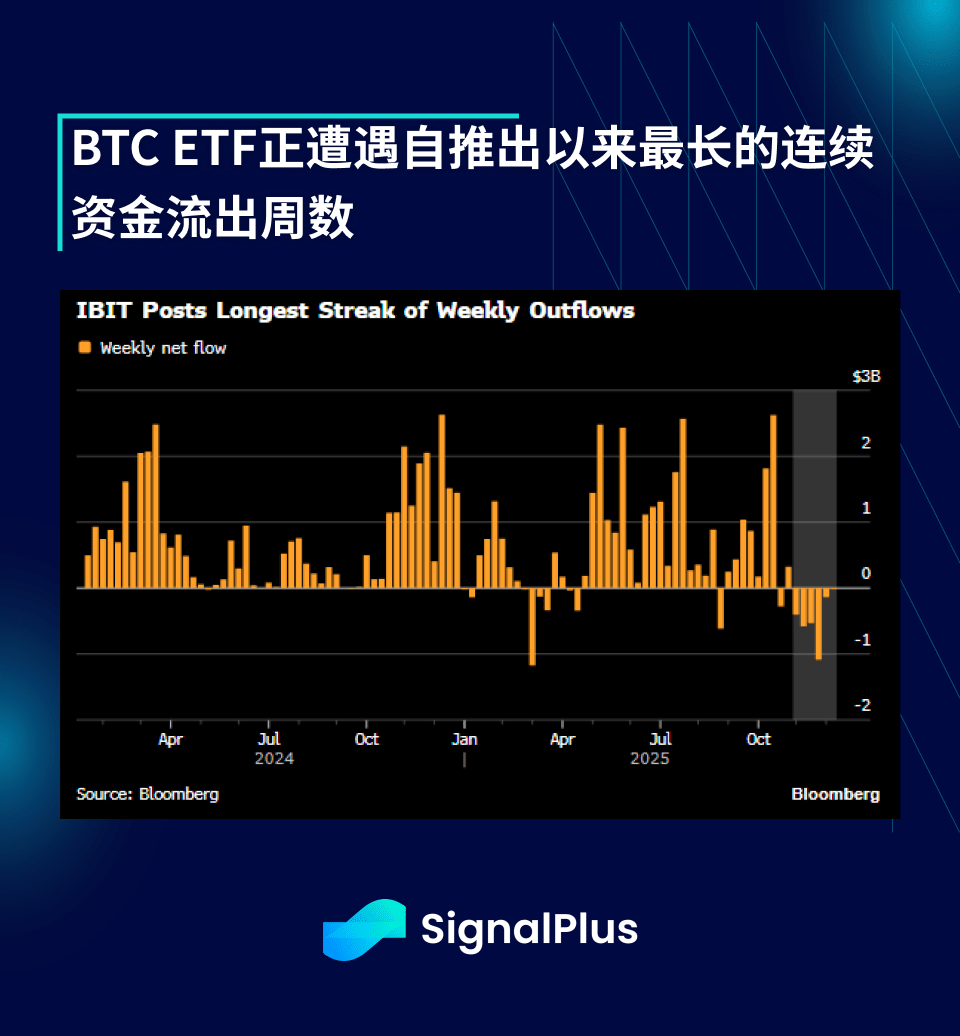

All of this has had little impact on the cryptocurrency market, with BTC prices rebounding to the $86,000–$92,000 range after a lackluster week of trading. Unfortunately, the underlying market sentiment seems to have turned negative, as BlackRock's IBIT has experienced the longest consecutive weeks of fund outflows since its inception, accumulating nearly $2.9 billion in outflows over the past six consecutive weeks.

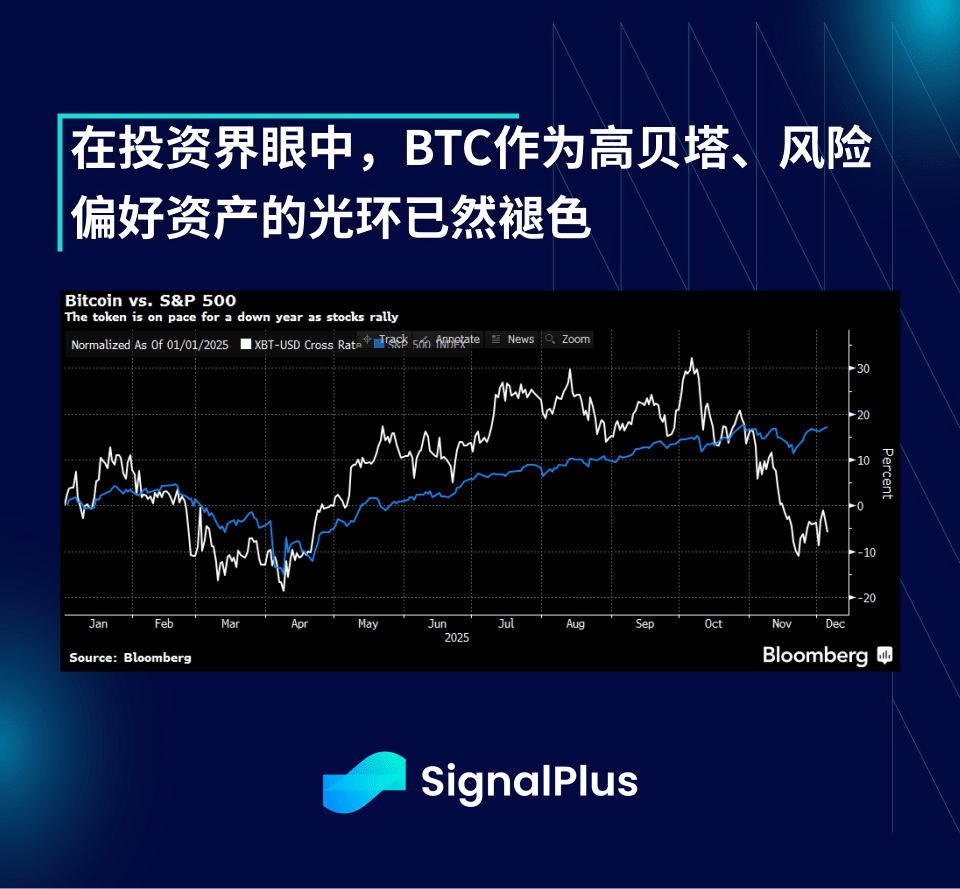

This structural sentiment shift can be seen from BTC's recent correlation (or lack thereof). Over the past eight weeks, BTC has significantly underperformed compared to other high-beta, risk-on asset classes. This decoupling phenomenon has occurred as investors' focus has completely shifted to AI and related stocks, with retail traders globally flooding back into intraday stock trading (and forecasting), while gold and silver prices remain near historical highs.

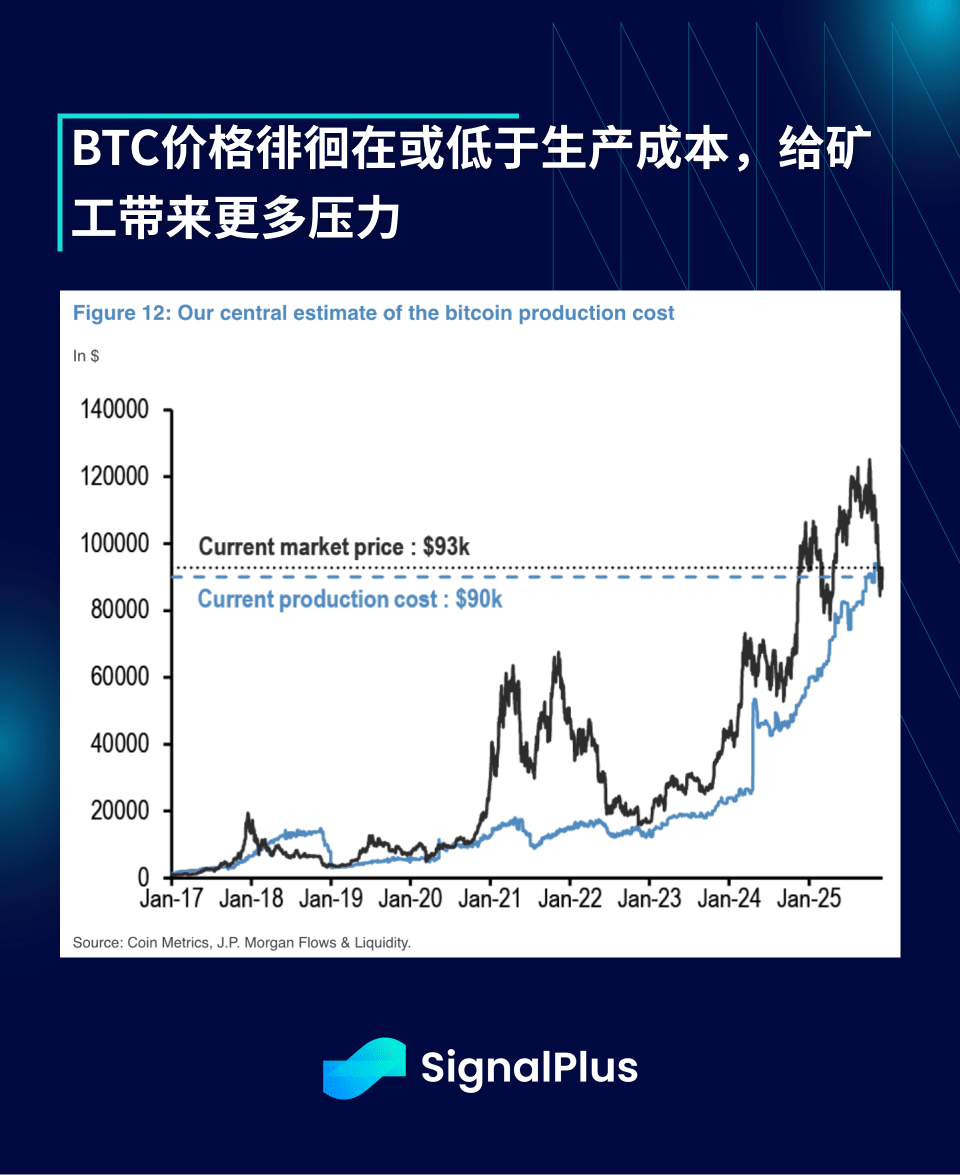

From a production perspective, BTC prices continue to hover below most production cost metrics. Due to China's recent crackdown on cryptocurrency activities and miners shifting computational resources to AI while scaling back pure mining activities, hash rates have plummeted. If prices remain below production costs for an extended period, it will put additional pressure on miners, potentially leading to further declines in hash rates and mining difficulty, creating a negative feedback loop resulting in lower BTC prices in the medium term.

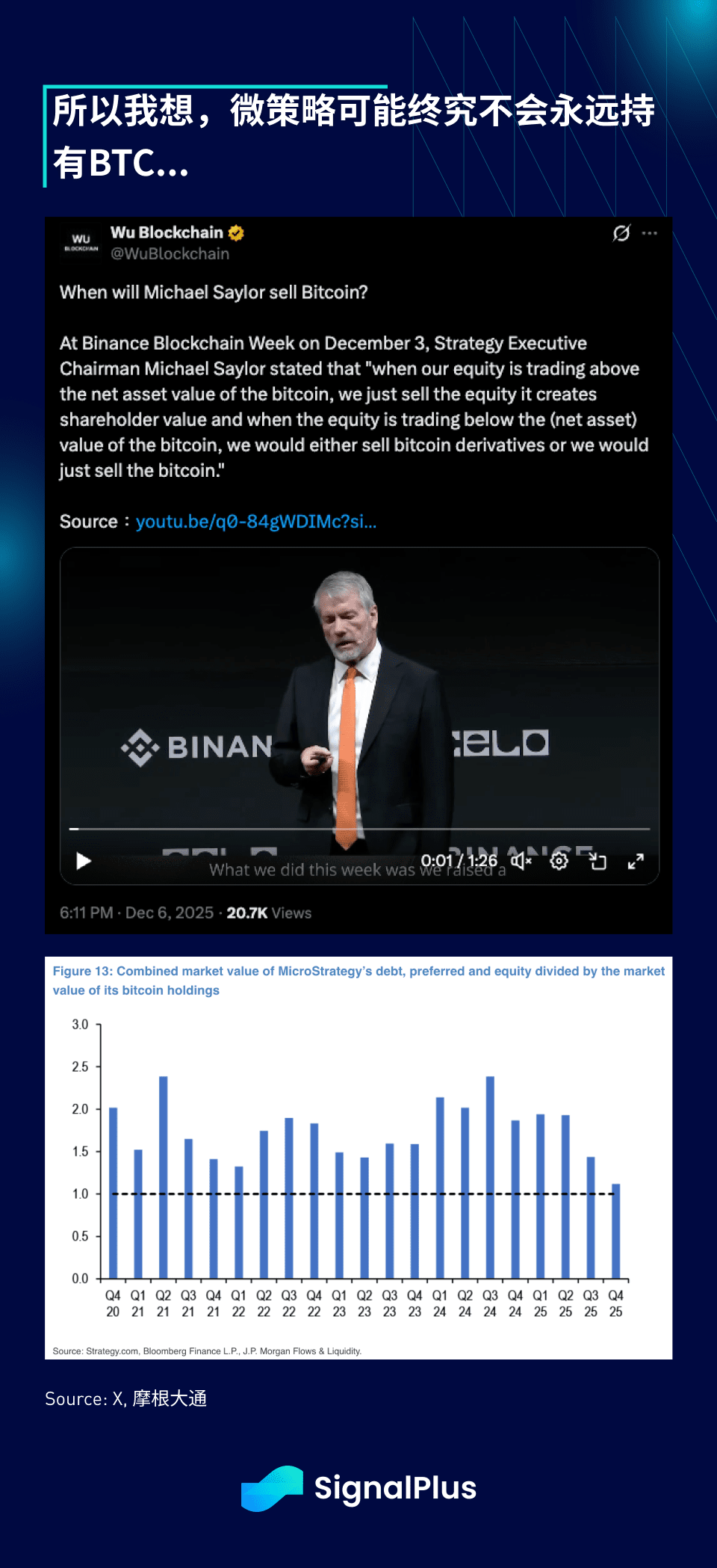

More troubling is that the global DATs' plunge has sparked widespread market concern about oversupply and the potential for forced selling when these listed companies' stock prices fall significantly below the value of their held BTC. MicroStrategy (MSTR) is under the greatest pressure, as the total value of its debt plus equity has a negligible premium compared to the value of its held BTC. When asked what would happen if this ratio fell below 1, Saylor gave a worrying answer:

"When our stock trades above the net asset value of Bitcoin, we sell stock, which creates value for shareholders; when our stock trades below (the net asset value of Bitcoin), we will either sell Bitcoin derivatives or sell Bitcoin directly." — Michael Saylor, Binance Blockchain Week, December 3

I hope that MicroStrategy's (MSTR) $1.4 billion reserve fund can keep it from being forced to liquidate its BTC reserves in the foreseeable future.

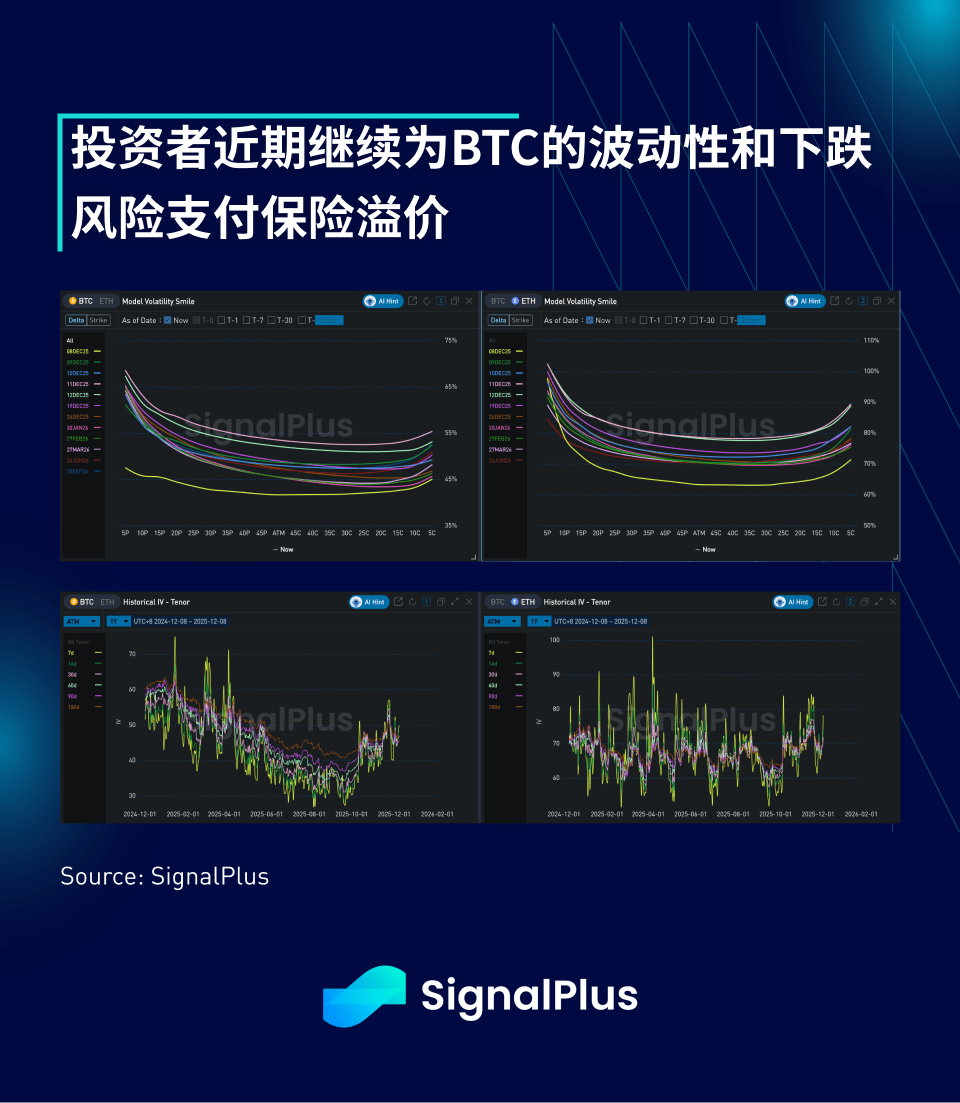

Looking ahead, the situation is largely the same as before — the stock market may remain firm before the end of the year, while the fixed income market faces short-term adjustment pressures, as global central banks, aside from the Federal Reserve, shift to a neutral/hawkish stance pushing yields higher. We worry that cryptocurrencies will remain in a short-term bear market until proven otherwise, which is reflected in the volatility market, where traders continue to pay a premium to hedge against price declines. A very dovish rate cut (or an unexpected decision to include BTC in the S&P 500) may be needed to reverse the short-term trend, so we expect market interest and sentiment to remain subdued and slowly decline as the new year approaches.

Good luck, and happy trading.