When the price of USDf flashes a red number of 0.95 on the screen, emotions won't give you time to think.

The Curve pool instantly turns into an escape route, as market makers sell off and withdraw, with X filled with screenshots of 'de-pegged' and 'it's over'—at this moment, typing ten thousand HODL in the comments is meaningless; on-chain only recognizes one thing: who is using real money to take over, and who is just talking about stability.

In the design of Falcon Finance, this role has been written into the code from the very beginning:

When USDf drops below a certain threshold (for example, 0.98), a program known as the 'Last Resort Bidder' will automatically awaken.

It won't tweet to soothe emotions, but will do one thing:

Using the hard currency in the insurance fund to absorb all the USDf that everyone throws out in the open market and then directly destroy it.

This is not sentiment; it is a monetary policy written into smart contracts.

When the price loses its peg, who will take the last baton?

The depeg of the stablecoin appears to be a price issue, but underneath, it is actually a misalignment of supply and demand + trust collapse.

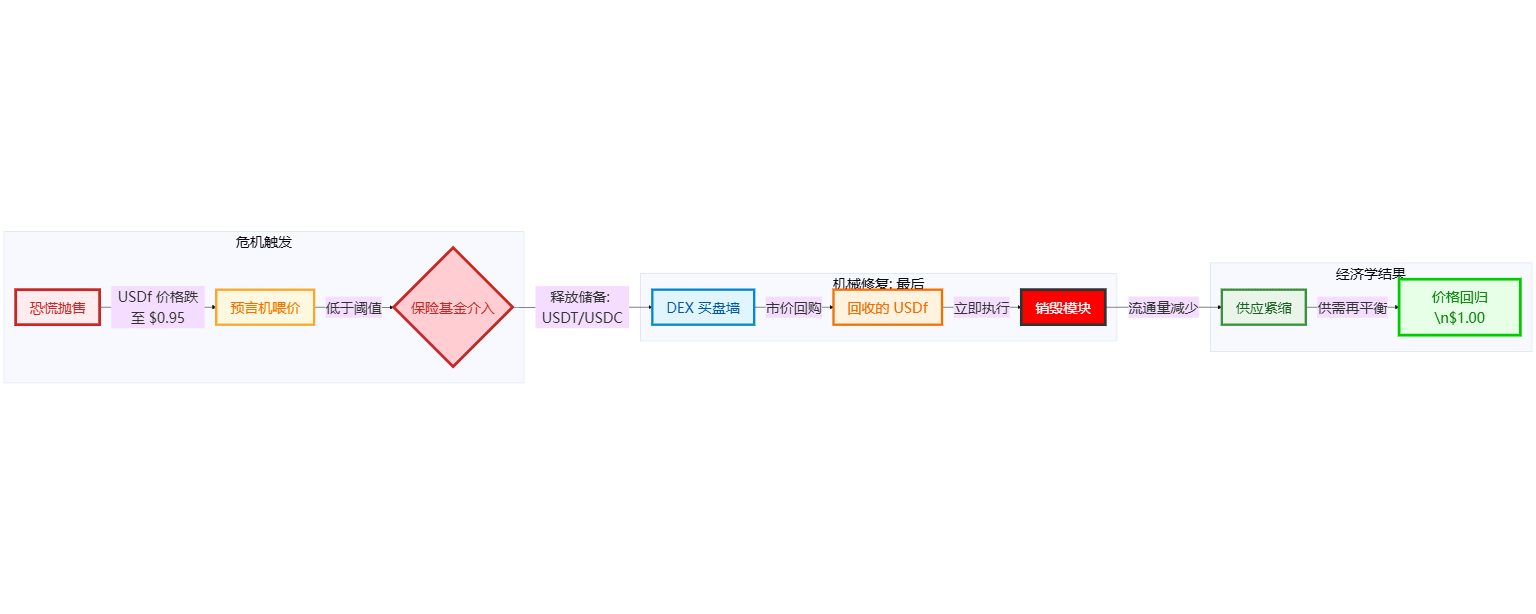

Panic emotions → holders rush to sell USDf → market orders pile up in an instant.

Market makers lower quotes → secondary market prices drop to 0.97, 0.95, or even lower.

Users who still haven't figured out what happened also start to 'sell first and talk later'.

If at this moment the protocol does nothing, everyone has seen what happens next:

The more the secondary market falls → the more people panic sell → the curve accelerates its descent.

In the end, it turns into a familiar trajectory: the death spiral.

Falcon's idea is very simple:

Not hard against human nature, but using a stronger force to take over the 'last baton'.

This power is the insurance fund, independent of the protocol token price.

Algorithmic central bank: the insurance fund's 'open market operations'.

From the perspective of monetary banking, what Falcon arranged for the insurance fund is a standard OMO (Open Market Operations) process:

When USDf trades below the peg price (e.g., 1 dollar) in the open market.

The protocol judges that: oversupply / market panic selling.

The insurance fund begins to execute preset strategies:

Using reserve stablecoins (USDT/USDC, etc.) to place buy orders on DEX/CEX.

To gradually absorb the selling pressure at market prices.

The USDf that is reclaimed is not left on the books but is immediately destroyed.

Reduced supply is a hard rule:

Under the premise that demand has not completely vanished,

For every 1 USDf destroyed, every remaining 'support' becomes thicker.

You can understand this as:

Falcon initiated a round of algorithmic 'central bank repurchase' — but the object isn't national bonds, but the stablecoins it issued.

Cutting off the death spiral: why it is necessary to use 'external bullets' to put out the fire.

Why can't Luna/UST come back on that road?

The core issue is not that 'the design is too radical', but that the assets that are bailed out and the assets being bailed out are part of the same system — endogenous risk overlaps.

UST depegs → the protocol opens the gates to repurchase with LUNA.

The greater the selling pressure on UST → the more LUNA the protocol needs.

The market discovers infinite issuance of LUNA → directly crushes LUNA together.

The result is the familiar 'vertical line' on the logarithmic coordinate.

Falcon directly seals off this path:

The bullets of the insurance fund do not come from FF, nor from USDf itself.

Reserve assets only use external hard currencies: USDT, USDC, and other stablecoins.

These things are not strongly bound to the health of Falcon's protocol.

When a black swan hits Falcon:

The protocol may face internal pressure.

But the USDC on the insurance fund's account is still a 1:1 dollar claim.

This ensures that at least one asset operates outside the storm's center.

Using external hard currencies to repurchase its own debts is a physical isolation layer to prevent the death spiral.

A picture to understand: how the 'last buyer' pulls the anchor back to 1 dollar.

Breaking down this seemingly abstract 'monetary policy' gives you the following chain:

Here are two key points:

Buying and burning are bound actions.

Only buying without burning just moves the selling pressure from the open market to the protocol's balance sheet.

Buying and then burning is truly 'debt reduction'.

Triggers are rule-driven, not based on human whim.

It's not about the team's mood while watching the market.

It's about when the oracle + contract conditions hit the point, eliminating human delays and emotional interference.

Price anchoring has turned into a verifiable, retraceable state machine.

Financial cleanup: some sold at 0.95, while others got a cleaner 1.00.

From the perspective of the balance sheet, this is not simply 'bailout', but more like a financial cleanup.

To those who panic-sell:

They sold their USDf to the insurance fund at the 0.95 position.

Exit at a discount, locking in losses.

To the protocol itself:

Repurchase 'face value 1 dollar' debts at a cost of 0.95.

And directly reduce unpaid liabilities through destruction.

To the remaining sUSDf / USDf users:

After liability reductions, the overall asset coverage ratio of the system becomes healthier.

Every future profit rolls out on a thicker safety cushion.

To put it brutally:

The discounted sell-off by panic sellers turns into the system's 'blood replenishment',

And this blood replenishment will ultimately reward those who stay with more stable pegs and more enduring returns.

This is a real-life version of on-chain Darwinism.

Discipline and ammunition: where does the insurance fund's money come from?

To dare to buy at 0.95, the premise is that the fund account must have real bullets.

Falcon's approach is not to pat its chest and say 'we will take responsibility', but to write it directly into the protocol.

A portion of the monthly protocol profits is forcibly allocated to the insurance fund.

The yields of CeFi / DeFi strategies.

PSM fees, Swap transaction fees, and other protocol revenues.

Part of it is preset to become **'perpetual reserves'**.

The effect is:

The larger the scale of the protocol (TVL), the more profitable the business.

The size of the insurance fund keeps pace → the shocks it can withstand are also greater.

In other words, Falcon does not distribute all the profits from good days at once:

A portion is forcibly kept as 'insurance premium for future black swans'.

This discipline is what truly supports the confidence behind the words 'last buyer'.

Safety is the most expensive function, but it is also the most worthwhile to buy.

In the financial world, there is no free anchor.

To have certainty of 1 dollar, someone must pay for that certainty.

In Falcon's design:

What users give up is a part of the 'protocol profits that could have been distributed immediately'.

What is gained is rigid support + automatic repurchase + circulation contraction under extreme market conditions.

The conclusion left by F018 is very simple:

You cannot stop black swans, but you can decide whether you are the group that gets swept away,

or if you stand on the side with the 'last buyer', watching other protocols get cleared.

In the future reshuffle of DeFi, those:

No independent insurance fund,

No external assets as a backstop,

No publicly written open market operation mechanism.

The stablecoin might only need one extreme event to have its name erased by history.

And systems like Falcon, which write the 'last buyer' into the protocol and lock real money into the insurance fund, will prove themselves more with each crisis on-chain:

It's not about claiming stability, but repeatedly demonstrating it to the market through practical action —

While others defend the peg with words, it has already defended the peg with money.

I am a sword-seeking boat; if one day you really see USDf drop to 0.95,

Don't rush to close the chart; first check on-chain:

The address that quietly had buy orders up when you panicked and cut losses,

is the 'last line of defense' that Falcon prepared for you in advance.

I am a sword-seeking boat, an analyst who focuses only on essence and doesn't chase noise.