In this round of the crypto market in 2025, retail investors fear hearing two words: unlocking.

The plots of countless projects are the same: before TGE, 'top institutions backing' create a frenzy, after TGE, VCs sell off chips at a fraction of the cost, leaving behind a series of shameful waterfall lines on the chart, forcing real users to provide liquidity exits for early capital.

Falcon Finance chooses to play this script in reverse.

In Falcon's token allocation table, there is only one eye-catching number in the Investor column: 4.5%. Not 20%, not 15%, but a single digit. Even harsher is that this 4.5% is also explicitly written in the contract: 1 year cliff + 3 years of linear unlocking, for a full 365 days after going live, VCs can't sell a single FF.

This is not 'unfriendly to VCs', but a bare declaration: 'If you don't want to run long distances with me, don't get on my car.'

Falcon's unusual setup: VC only has 4.5% and is locked for 4 years.

From the perspective of Tokenomics, Falcon's structure almost runs counter to industry consensus.

Most DeFi projects play with: 'low circulation + high FDV'—

In the early TGE, the circulation was kept very low, making it convenient for the market-making team to create a perfect curve, and later, with private placements and team unlocks, chips are thrown to the secondary market in rounds.

Falcon is doing the opposite:

VC: 4.5%

1-year cliff: 0 unlocking in the first 12 months.

The next 3 years linear: equivalent to being bound by a 4-year labor contract.

TGE circulation: about 23.4%.

Mainly for: ecosystem, community, liquidity incentives.

What can truly act in the market are users and builders, not investors.

Total supply: 10 billion FF.

The bulk is reserved for the ecosystem (about 35%) and the foundation (about 24%), used to incentivize real behavior rather than decorate a cap table.

The result is a strikingly contrasting picture:

On-chain Falcon has 'retail investors running first, institutions following behind.'

VCs are not waiting for you to take over at the finish line but are tied to the starting point, bearing the entire early cycle with you.

When VCs are locked for a year: who is backing FF's price?

Most people's first reaction to 'VC only has 4.5%' is:

'Great! The pressure to dump is less!'

But what's really interesting is: this structure directly changes the behavior function of VCs.

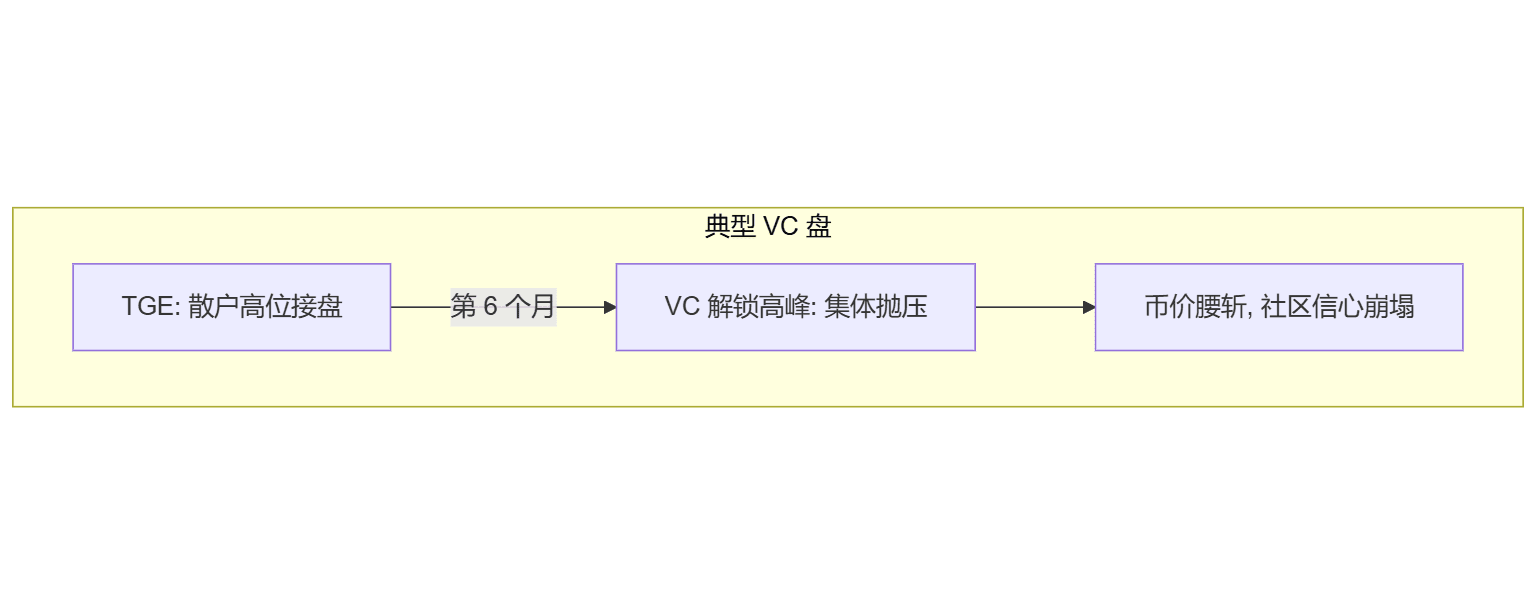

For a typical VC market, the timeline looks like this:

Falcon's timeline tells another story:

TGE2[TGE: 23.4% community/ecosystem circulation] -->|Months 0-12| Cliff[VC fully locked: cannot sell] -->|From month 13| Drip[Starting 3 years linear: slowly released like a faucet] --> Stable[Coin price supported by protocol revenue & real demand]

Key difference:

Typical projects:

6–12 months is the peak of selling pressure, with low VC costs and quick unlocking. 'Rational choice' means selling at a high.

Falcon:

In the first 12 months, a VC cannot move a single FF.

What truly affects the price are the actual usage by users, TVL growth, and the performance of the protocol's revenue.

In other words, Falcon has taken away the early dumping freedom from VCs,

while also giving them a very realistic multiple-choice question:

'Whether FF is $0.1 or $10 a year later depends on whether you are willing to help me scale the protocol now.'

This is not sentiment; this is a hard economic constraint.

The 4.5% VC: has transformed from 'capital side' to 'BD with capital investment.'

If you take the 4.5% in the Falcon Investor column as 'investor welfare', then you're looking too shallow.

A more accurate statement is:

This 4.5% is the 'margin' paid by VCs— a kind of on-chain staking proof (Proof of Skin in the Game).

Because:

Small share: no matter how many resources you get, you can't become rich just by selling.

Locked for a long time: 1 year cliff + 3 years vesting, extending the timeline throughout the entire cycle.

To achieve decent returns on this 4.5%, VCs must do a few things:

Bringing in your network from TradFi:

Introducing RWA partners, bank custody, market-making teams, compliance licenses;

Helping Falcon access more assets and users:

Making USDf truly enter institutional balance sheets rather than just staying in the white paper;

Coordinating the secondary market:

Until they unlock, no one wants to see FF priced reasonably and with real buy orders more than they do.

They have transformed from 'the ones who pay' to 'those who work for the protocol.'

For retail investors, this means one thing:

You see VC's profit curve for the first time, highly bound to the same timeline as you.

Smart contracts are written in stone: this time it's not a 'promise', it's a physical rule.

Many projects also shout 'we are long-termists' and 'VCs won't dump',

but those who have been truly educated by the market know: as long as the authority is in multi-signature, any verbal promise is worthless.

Falcon has done two hard things:

1 year cliff + 3 years linear vesting, all written into the token contract.

No backdoor for 'team proposal modifications';

No black box for 'special circumstance early unlocks';

Everything is based on block.timestamp, verifiable and calculable on-chain.

A high proportion allocated to the ecosystem rather than capital.

About 35% for the ecosystem (incentivizing real usage).

About 24% for the foundation (long-term development budget).

The 4.5% from VC feels more like 'the role of staking' rather than 'the main character's chips.'

The ultimate meaning of this design is:

Falcon does not profit from 'who took how much initial allocation',

but rather from 'how much actual cash flow the protocol can generate' to price all holders of FF.

The spring for retail investors? It’s not about giving away money, but rather the rules being on your side for the first time.

Returning to the question in the title:

Does the 'humble' share of 4.5% really mean spring has come for retail investors?

My answer is: it at least means that the rules are clearly biased towards you for the first time.

Early selling pressure is no longer determined by VCs, but by real demand + protocol performance;

VCs are no longer the ones who leave early but are locked in the car with you to bear the entire cycle;

FF is no longer just a governance token but has become in this structure:

A participation chip for users.

The margin for VCs.

Leverage for protocol growth.

I still say: Institutional design is the hardest benefit.

The next time you look at a new project's token allocation, remember to ask first—

'How much did VC take? When can they sell?'

In Falcon Finance, the answer is: 4.5%, selling slowly after 4 years.

In such a game structure, even if no one promises 'not to dump', mathematics has already made the choice for you.

I am like a boat seeking a sword, looking at the real flow of power on-chain in the tiniest line of numbers in the token distribution table.@Falcon Finance $FF #FalconFinance