The cryptocurrency world easily trains people into a strange kind of being: every year chasing 'what to play this year,' and by the end of the year, there’s only a string of account screenshots and a few emotional summaries—'made money,' 'lost money,' 'next time I won't chase the highs.' But those who can truly become stronger in the long run never review their gains, but rather the quality of their decisions: Why did I make this move at that time? Did I adhere to the boundaries? Was I led by emotions? Did I repeat the same mistake three times? Tools like Falcon are best suited for this purpose because they are inherently 'structured': you can integrate them as a module into your financial plan rather than treating them as a short-term speculative event for a particular year.

So on this final day, I want to give you an “Annual Practice Template.” It doesn’t require you to write lengthy essays, nor does it require you to recreate every transaction; as long as you can tell the story according to the three sections, you can reuse it next year and be calmer and more structured year after year.

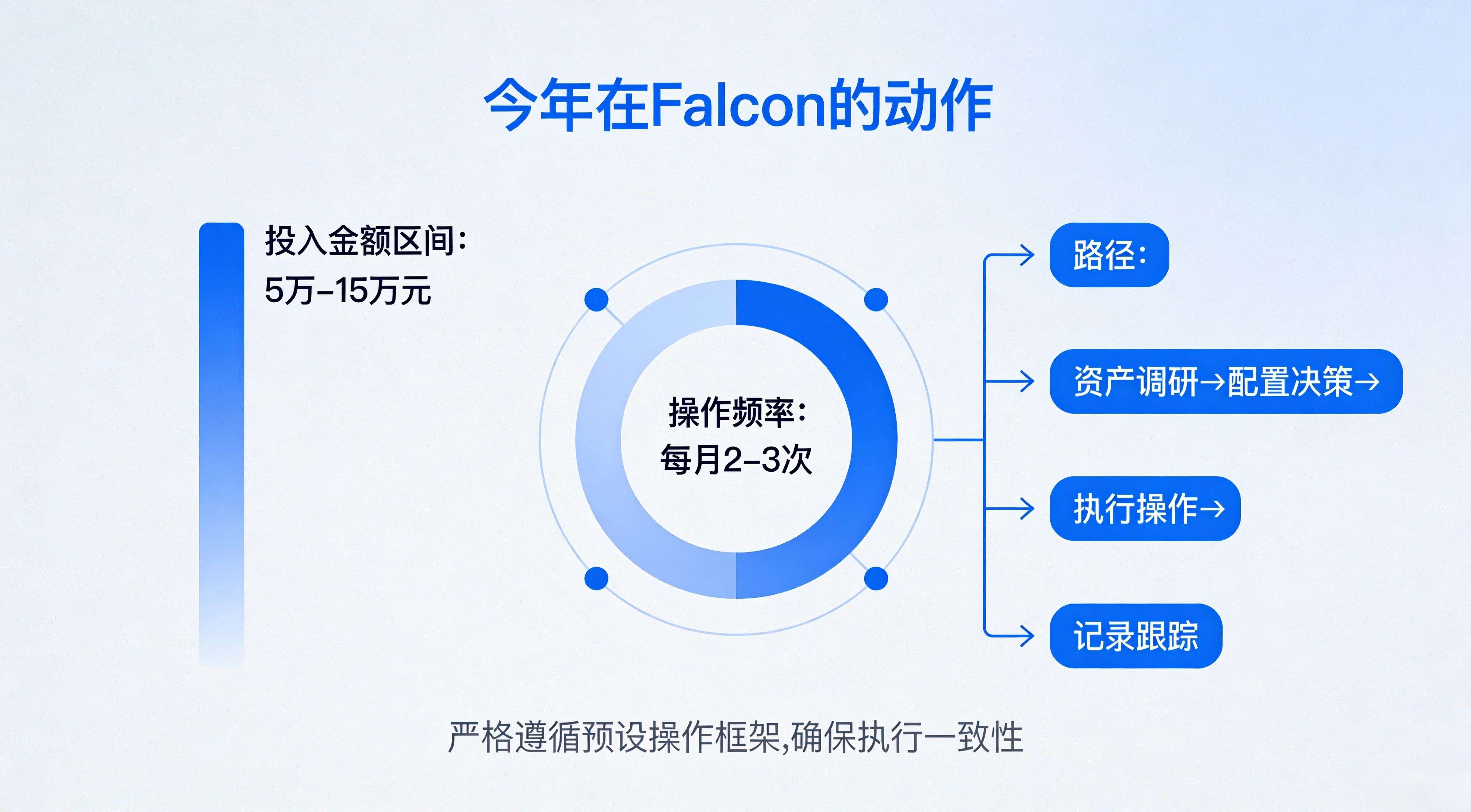

The first section is called “What actions did I take in Falcon this year.” Here, don’t write abstractly; be specific: how much did I approximately invest (you can use ranges, no need for decimals), what was my frequency of operations (for example, once a month, once a quarter, or only made two key adjustments), what paths did I go through (for instance, buying USDf, converting to sUSDf, making one redemption exit, whether I completed the entire process). The focus here is not to boast about the number of actions but to let your future self easily see: did I use it “systematically” this year, or was it just “a whim.”

The second section is called “What were the results.” Many people only write about profits; I hope you write from four dimensions: what level of profit you had (you can also write in ranges), what impact fluctuations had on you (were there uncomfortable phases), what the emotional experience was (did you frequently want to increase your position or withdraw, were you influenced by the community), and most importantly — where the results differed from your initial expectations. Note that this section is not to judge whether Falcon is “good or bad,” but to evaluate whether your own expectation management is “accurate or not.” If you keep failing in expectations every year, the problem often lies not in the tools but in how you set your goals.

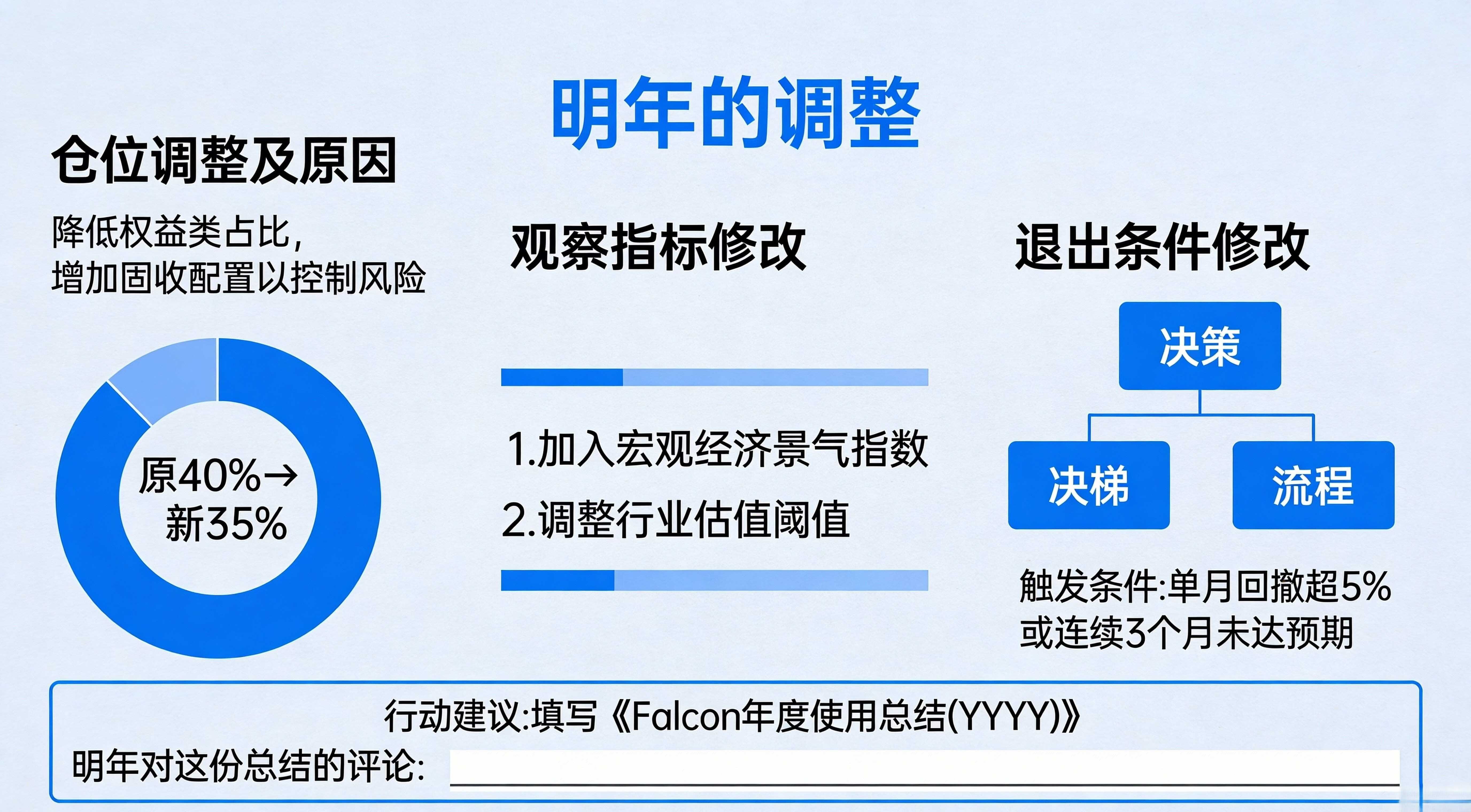

The third section is called “Adjustments for next year.” Here, you only need to answer three questions: do I want to increase or decrease this position next year, and why; do I need to change the observation indicators (for example, from only looking at profits to paying more attention to structural changes, exit path experiences, and discipline execution), and do I need to modify the exit conditions (for example, under what circumstances must I reduce my position or exit). This step will force you to turn the vague statement “next year will be better” into specific executable rules. Once the rules are written down, it will be harder for you to be swayed by emotions next year.

I want to emphasize one thing: this annual summary is not a review of profits but a review of “discipline.” You may not have high profits this year, but if you strictly adhered to position limits, conducted regular reviews, recorded every decision, and successfully navigated the exit path once, then you are actually stronger than many people who “earned this year but relied entirely on luck.” Because discipline can compound, while luck cannot. Treat Falcon as a “module that can be incorporated into your financial plan,” and you will naturally place it in the correct position: it is one of your asset structure components, serving your cash flow, risk boundaries, and long-term goals, rather than serving your momentary impulse needs.

The corresponding rule changes behind this are also very clear: you have shifted from “What to play this year” to “I am building a long-term, stable, and iterative asset system.” When you can write Falcon as a “component” rather than an “event,” you will no longer be led by annual narratives. You will begin to care about: what role does this component play in my system, how does it integrate with my career risks, family expenses, and reserves structure, and whether its boundaries are clear. At this stage, your asset management can be considered to have truly entered a long-term mode.

The final action suggestion, I hope you can do today: open a dedicated document titled (Falcon Annual Usage Summary) — complete it according to the three sections above, and leave a blank space at the end with the words “Comments on this summary for next year.” This blank line is very important because it allows you to look back in the future, as if reading someone else's case, with calmness. True growth means: when you look at this summary next year, you will clearly see where you have become more stable, more structured, and where you are still swayed by emotions. If you can see these things, you are already getting stronger.