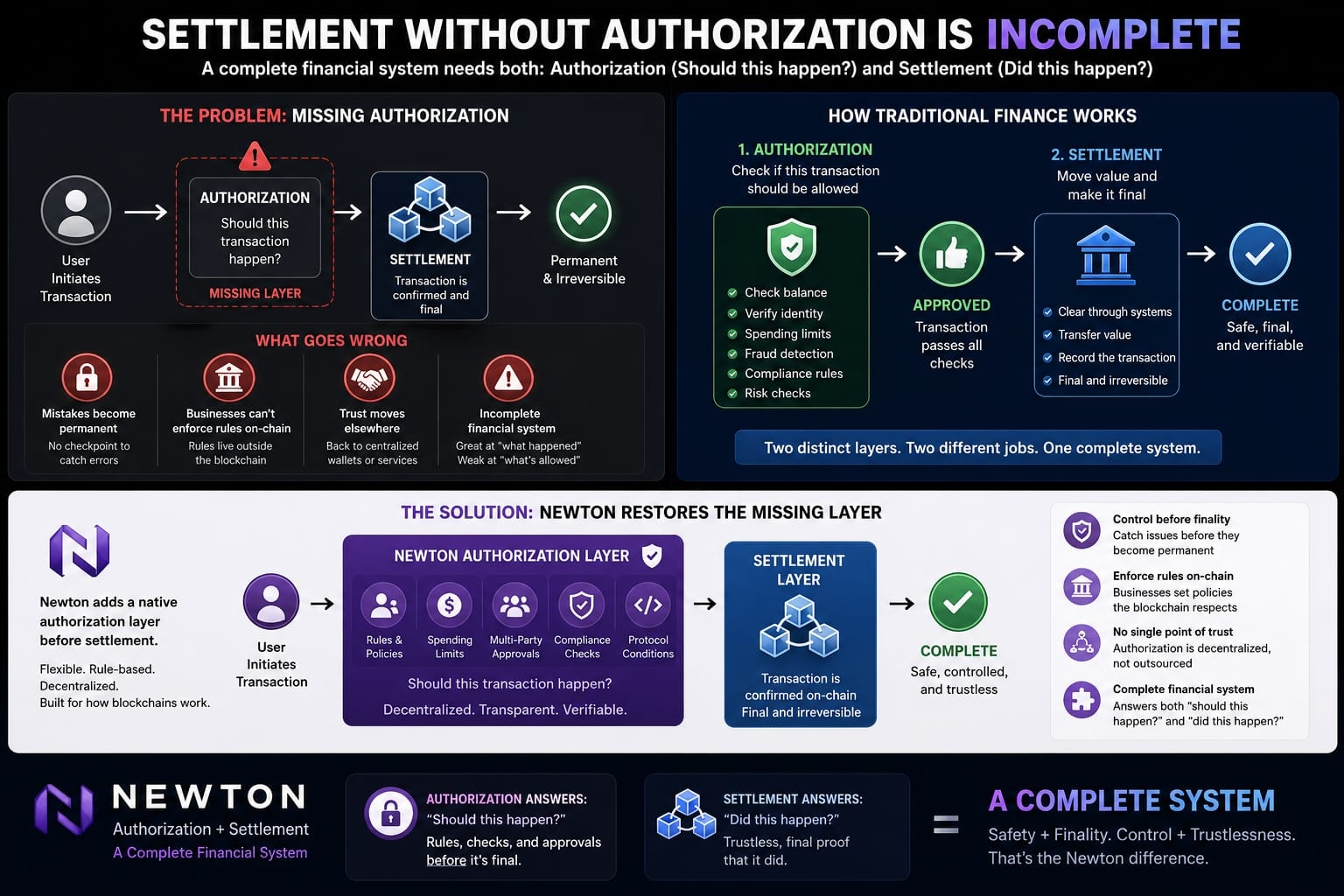

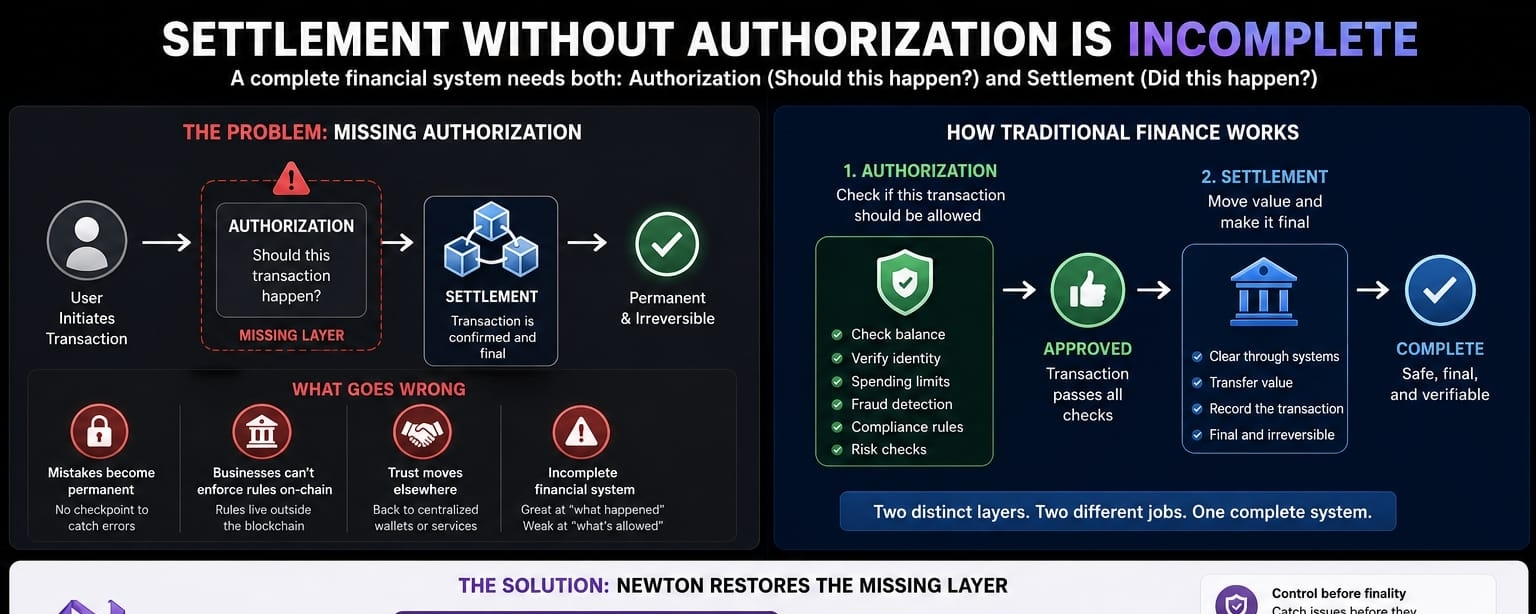

Blockchains solved a hard problem. They let two strangers move value to each other without trusting a bank, a clearinghouse, or each other. This is called trustless settlement, and it is a real achievement. But settlement is only one piece of how money moves in the real world. There is another piece that traditional finance always had, and that most blockchains quietly skipped: authorization.

What Settlement Actually Means

Settlement is the final step in a transaction. It is the moment when value actually changes hands and the deal is done. On a blockchain, settlement happens when a transaction is confirmed and added to the chain. Once that happens, it is final. Nobody can reverse it, and nobody needs to trust a middleman to make sure it really happened.

This is powerful. In traditional finance, settlement can take days, and it depends on banks and clearing systems trusting each other. Blockchains removed that need. Two people anywhere in the world can settle a transaction directly, with proof that anyone can check.

The Missing Piece: Authorization

But before settlement happens, there is always a question that comes first: should this transaction happen at all?

In traditional finance, this question is answered by an authorization layer. Before your card payment settles, your bank checks if you have enough money, if the transaction looks normal, and if it follows the rules. A wire transfer goes through compliance checks before it is sent. A trade gets approved by risk systems before it settles. This authorization step is not just a formality. It is what makes the system safe to use at scale.

Most blockchains never built this layer properly. A blockchain can tell you, with total certainty, that a transaction happened. But it usually cannot tell you, ahead of time, whether that transaction should have been allowed in the first place. Many systems leave this job to the user's wallet, to a centralized app, or to nothing at all.

This is why settlement without authorization feels incomplete. You get a system that is excellent at proving what happened, but weak at controlling what is allowed to happen.

Why This Gap Matters

This gap shows up in real ways:

Mistakes become permanent. If a transaction should not have happened, like a stolen key being used or a bad smart contract approval, the blockchain still settles it perfectly. There is no checkpoint to catch the error before it is final.

Businesses cannot enforce rules on chain. A company that needs spending limits, approval steps, or compliance checks usually has to build these things outside the blockchain, in a separate app. The blockchain itself does not know about these rules.

Trust moves somewhere else. Without a real authorization layer, people end up trusting a wallet provider, a custodian, or a centralized service to do the checking. This brings back the exact kind of trust that blockchains were supposed to remove.

In short, blockchains decentralized the "what happened" part of finance, but the "what is allowed to happen" part often stayed centralized, hidden, or missing.

How Traditional Finance Handles This

It helps to look at how traditional finance separates these two layers.

When you make a payment, there is usually a clear order of steps. First, the system checks if you are allowed to make this payment. This might involve checking your balance, your identity, your spending limits, or fraud signals. Only after passing these checks does the transaction move to settlement, where the money actually moves.

This separation exists for a good reason. Authorization needs to be flexible. Rules change based on context, like who is sending money, how much, to whom, and under what conditions. Settlement, on the other hand, needs to be final and simple. Mixing these two jobs together would make the system harder to trust and harder to fix when something goes wrong.

Blockchains got very good at the settlement side. They mostly skipped building a flexible, native authorization layer on top.

How Newton Fills This Gap

Newton is built around the idea that authorization should not be an afterthought bolted onto a blockchain. It should be a real layer that sits before settlement, doing the job that banks and clearing systems have always done, but in a way that fits how blockchains work.

Instead of treating every signed transaction as automatically approved, Newton adds a clear authorization step. This means rules, conditions, and checks can be applied to a transaction before it becomes final. A business can set spending limits. A team can require multiple approvals. A protocol can check conditions that matter for safety, all before the transaction settles on chain.

This does not slow down or weaken the trustless nature of blockchain settlement. The settlement layer stays exactly as strong and verifiable as before. What changes is that transactions now pass through a real checkpoint first, the same way payments do in traditional finance. Newton essentially restores the missing half of the system, without giving up the part that already works well.

Putting the Two Layers Together

When you put authorization and settlement together properly, you get something closer to a complete financial system. Settlement still gives you trustless, final proof that a transaction happened. Authorization gives you control, safety, and the ability to enforce rules before that transaction becomes unstoppable.

Blockchains proved that settlement does not need a trusted middleman. Newton's approach is to apply that same thinking to authorization, building a layer that is flexible and rule-based, but still works in a decentralized way instead of depending on a single trusted party.

The Bigger Picture

Trustless settlement was never meant to be the whole story. It is one half of how real financial systems work. The other half, authorization, decides what should happen before settlement makes it permanent.

By skipping this layer, many blockchain systems left a gap that users, businesses, and developers had to fill with workarounds, centralized apps, or extra trust in third parties. Newton's goal is to close that gap directly, bringing a proper authorization layer to blockchain settlement instead of treating it as optional.

Settlement answers the question "did this happen?" Authorization answers the question "should this happen?" A complete system needs both, and that completeness is what Newton is built to provide.

@NewtonProtocol is designed to address.