I’m not looking at this from a trader’s perspective today @NewtonProtocol , and instead switching to a more ordinary identity: imagine I’ve opened a small on-chain shop that sells digital services, accepting USDT or USDC. Each day the orders aren’t huge—anywhere from dozens to a few hundred in value. Customers come from different regions: some are old customers, and some are paying for the first time. This scenario doesn’t sound earth-shattering, but I feel it’s actually closer to where real on-chain payments need to land.

When people talk about stablecoin payments, the first reaction is usually: fast, cheap, and convenient for cross-border transactions. Those points are true, but if you really treat it as a business, the problems are far more complex than just “how quickly it arrives.”

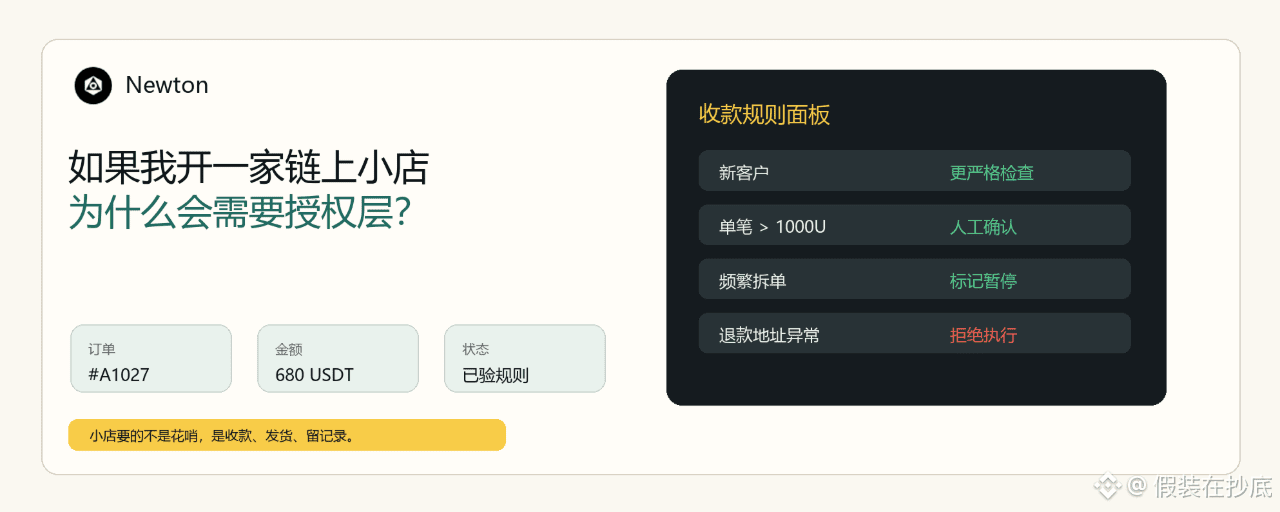

For instance, say today a customer paid 680 USDT and the blockchain shows it arrived—I’m obviously happy. But I’ll also wonder: Has this address interacted with any high-risk protocols before? Is this amount clearly beyond their usual spending habits? If the platform asks me about this order later, can I prove that checks were done at the time? And if one day a partner demands I provide payment records, am I just able to hand over a string of tx hashes and say, “Go look on-chain yourself”?

On-chain hashes can prove that the money moved, but they can’t explain why this money should be received.

This is what I find interesting about @NewtonProtocol l. In its whitepaper, it talks about an authorization layer—sounds technical, but in a small merchant scenario, it can actually be translated into one sentence: before money enters the door, the questions that should be asked are asked first.

For example, I can set a few simple rules for my own payment contract:

If a single transaction exceeds 1000 USDT, pause first and wait for manual confirmation.

For a new customer’s first payment, stricter address risk checks are required.

Funds from certain high-risk sources don’t go directly into the main account.

If the same address frequently splits orders and makes payments within 24 hours, mark it.

For small orders from whitelisted existing customers, things can go through more smoothly.

These rules aren’t meant to make running a business complicated; they’re meant to avoid disputes after the fact. It’s the same in real life: cashiers don’t ask the boss about every single transaction, but they’ll be alerted above a certain amount; members and unknown customers are handled differently; abnormal orders leave records. If on-chain payments are to become a normal business tool, they also need the capability to “automatically do what should be automatic and block what should be blocked.”

A lot of on-chain tools have a problem: they’re good at execution, but not good at explanation. When the money arrives, it arrives; when it’s transferred, it’s transferred; when it fails, it fails. But the longer a business runs, the more it needs explanation: why was this order accepted? What rules were used at the time? Who checked it? If there’s a problem later, can we look back?

Newton’s compliance receipt is perfect to understand here. It’s not decoration for technical people—it’s like a payment note in the order backend. It records the transaction intent, the policy that was evaluated, the operator’s response, signatures, and block information. Regular users might not open it every day, but once something goes wrong, it can become evidence.

I actually quite like Newton’s approach to privacy. Checking is needed to run a business, but it doesn’t mean exposing all customer privacy on-chain. The whitepaper mentions verifiable credentials—simply put, customers can prove they meet a condition without disclosing all personal information. For example, they can prove they come from allowed regions or meet some compliance requirement, but they don’t expose complete personal data to everyone.

This part is crucial. For on-chain payments to truly be used by more people, you can’t choose between “no checks at all” and “full privacy exposure.” The former is too risky, and the latter users won’t accept. What Newton is trying to do is a third option: rules are executable, results are verifiable, and underlying privacy is preserved as much as possible.

Now look at the AI agent scenario—small shops will use it too. In the future, I might have an agent automatically handle renewals, shipping, refunds, and simple customer service. It can be diligent, but it can’t refund money at will, can’t make payments to unknown addresses, and can’t divert order funds just because of a forged instruction. At that point, an authorization layer like Newton is like the store’s “cashier system”: staff can do things, but each kind of operation has its permissions.

For example, an agent can automatically process small refunds below 30 USDT; refunds above 100 USDT require manual confirmation; if the same customer requests multiple refunds within a day, pause it; the refund address must be linked to the payment address; and if the order status is abnormal, don’t execute the transfer first. Write these as policies, so you can check before a transaction happens—not by me waking up in the middle of the night to flip through records.

To me, this is more real than “AI helps me make money.” Because most ordinary people won’t use AI for high-frequency trading at the beginning—they’ll use it first for small things like payments, subscriptions, receiving money, reimbursements, and inventory. There are many small tasks, they’re repetitive, and they’re ideal for automation; but as soon as money is involved, there must be boundaries.

More specifically, what small shops fear most is “low-frequency but extremely annoying” disputes. For example, a customer claims they paid, but the order backend can’t match it; or the payment address and the ordering account aren’t the same; or the customer requests a refund, but the refund address provided is completely unrelated to the original payment address. Traditional platforms can still rely on payment service provider backends to look up orders, but on-chain, if only the tx hash remains, many details have to be assembled manually. If authorization records like Newton’s can be integrated with the order system, then the check results at the time can be preserved as well: whether rules were passed before payment, whether the payment address matches, whether the amount is within range, and whether the refund complies with policy.

This reduces a lot of psychological burden for small merchants. Not every seller has a professional risk-control team, and not everyone understands on-chain analysis. Most people just want to get paid, ship, keep a record, and avoid trouble. If you can hide complex checks inside the process and turn the key results into verifiable receipts, it’s more useful for them than explaining layers of underlying architecture.

So when I look at $NEWT , I don’t want to interpret it only as a market hotspot. It’s more like adding an infrastructure piece to on-chain commerce: put rules in place before transactions happen, leave receipts after rules are executed, and free users from having to hard-pick between speed and security.

If this direction works out, in the future small shops could even have their own “payment rule templates.” Selling digital subscriptions is one set, selling in-game items is another, and cross-border services are yet another. Beginners don’t need to write strategies from scratch—they can start with default templates and then adjust based on their own risk tolerance. On-chain payments would then have a chance to evolve from a tool for tech enthusiasts into an everyday tool that ordinary merchants dare to integrate.

I think this is what “automation” is truly supposed to look like. Not handing over all the keys and then living in constant worry every day; but being able to receive payments normally during the day, while at night the system can handle low-risk orders according to the rules. AI and contracts take care of repetitive work, and humans set boundaries and handle exceptions. If that division of labor holds, then small on-chain businesses can look more like businesses—not like a daily battle between wallets, hashes, and risk-control alerts.

If stablecoin payments really do move into more small shops, games, subscription services, and cross-border freelance scenarios in the future, I think people will care more and more about this: not whether money can be transferred, but whether it should be transferred, whether it should be received, and whether—if something goes wrong—it can be explained clearly.

The on-chain world is already very good at “confirming that it arrived.” Next, it may need to learn how to “confirm that it arrived for a reason.” That’s how I understand Newton Protocol today.#Newt