In 2025, the market value of gold RWA will exceed 3 billion USD, evolving from a safe-haven tool into a cornerstone of on-chain finance that integrates payment, collateral, and settlement. With regulatory and institutional support, it becomes the core bridge linking traditional and future finance.

Author, source of the article: CoinFound

0. Take Away

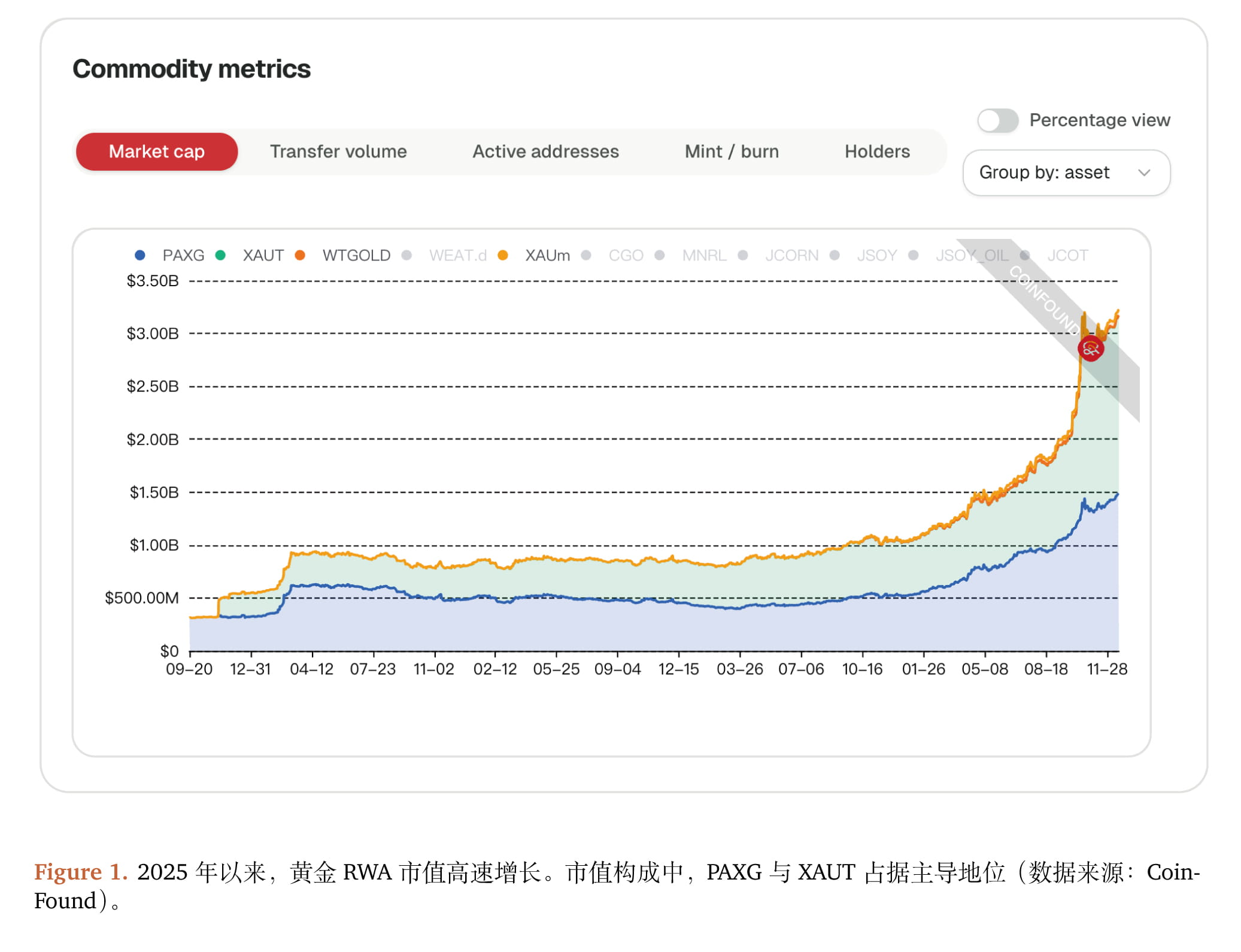

1. The market value of gold RWA is expected to grow nearly 3 times within 2025, breaking through 3 billion USD, with the gold RWA market rapidly expanding in 2025.

2. In the market landscape, the gold RWA market is shifting from a "duopoly" to "multi-functional layered coexistence": XAUt (Tether Gold) and PAXG (Paxos Gold) still dominate, serving respectively as the rulers of liquidity and derivatives (with a market value of 1.63 billion USD) and as benchmarks for compliance and regulation (with a market value of 1.43 billion USD). However, new projects like KAU and XAUm are connecting through payment ecosystems and DeFi yield designs, expanding differentiated pathways.

3. Increased participation from institutional investors: DBS Bank and Standard Chartered Bank are piloting cross-border settlement based on gold RWA, and multi-signature custody and institutional account systems are also being gradually integrated into the gold RWA ecosystem.

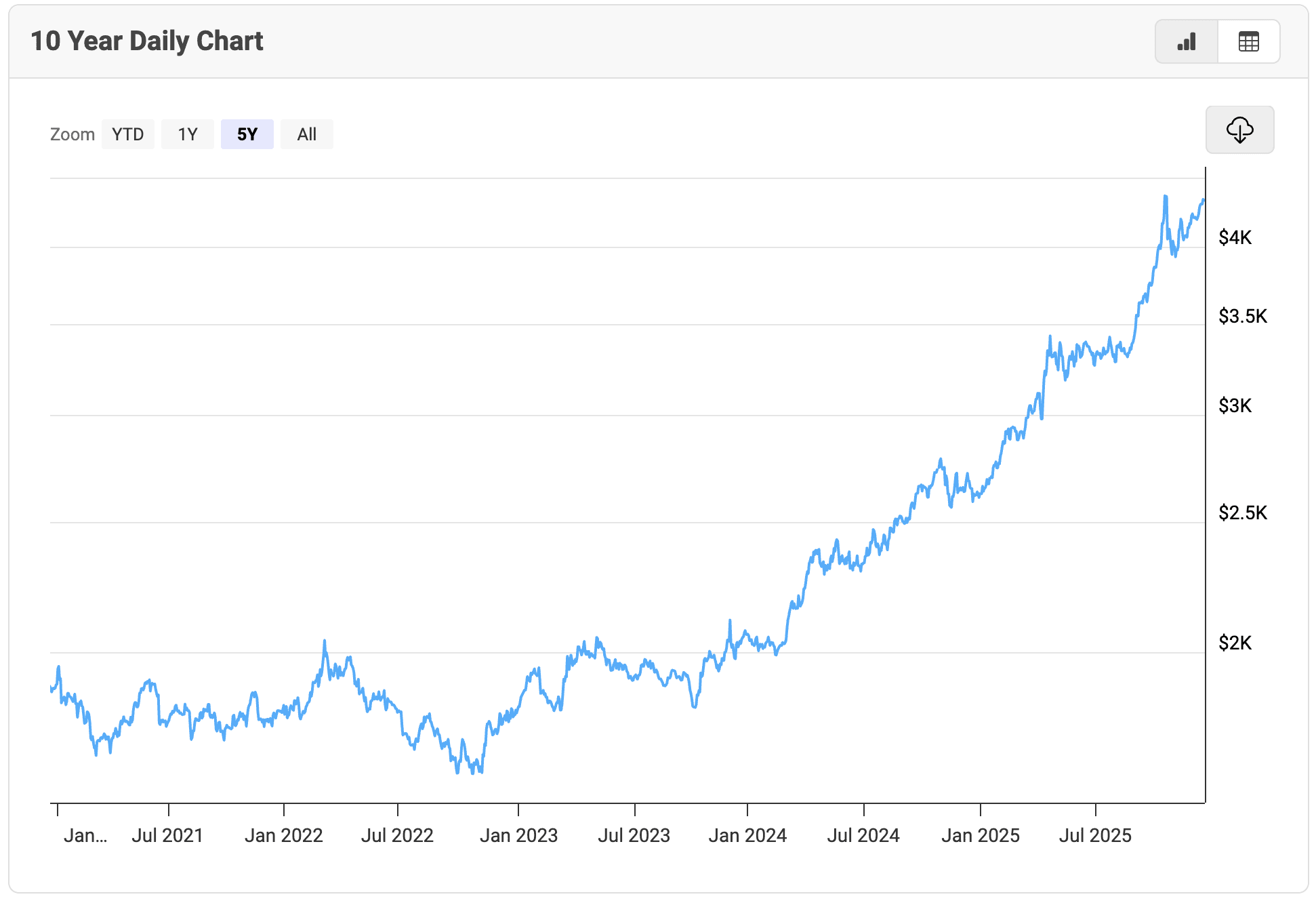

4. Due to the unstable macroeconomic environment, gold prices rose steadily throughout 2025, and the RWA gold price also continued to rise.

5. Currently, the demand for "on-chain gold" is expanding across various scenarios, from stablecoins to payments.

6. From the Bank for International Settlements (BIS) 2025 Annual Report to the US SEC's authorization of the DTCC to provide asset tokenization services in December, in the long run, a new generation of financial system is taking shape. Gold RWA, as a highly trustworthy and low-credit-risk real-world asset, will become a key value bridge in the on-chain financial infrastructure, which can not only assume the function of storing value, but also participate in core functions such as payment, clearing, collateral and cross-border settlement.

7. Gold RWA has multiple uses: a programmable "safe-haven asset," a core asset in on-chain clearing and settlement and collateralization systems, a medium of value in payment transactions, and a "bridge asset" linking traditional finance and facial finance.

8. Gold RWA still faces risks and challenges, particularly centralization risks, operational and transparency risks, and technological risks.

1. Market Status and Landscape 1.1 Rapid Growth of the Gold RWA Market in 2025

In terms of market capitalization, RWA Gold has nearly tripled this year. According to CoinFound data, as of December 19, 2025, RWA Gold's total market capitalization has exceeded $3 billion. Moreover, at the beginning of 2025, its total market capitalization was less than $1 billion.

From the perspective of participants, the number of RWA gold assets and their supporting ecosystem has grown rapidly this year, with more and more institutions entering the market. Before the beginning of 2025, the entire RWA gold market appeared much quieter, with only XAUT (Tether Gold) and PAXG (Paxos Gold) playing a leading role for a long time, while WTGOLD (WisdomTree Gold Token) was only showing a faint presence on the periphery.

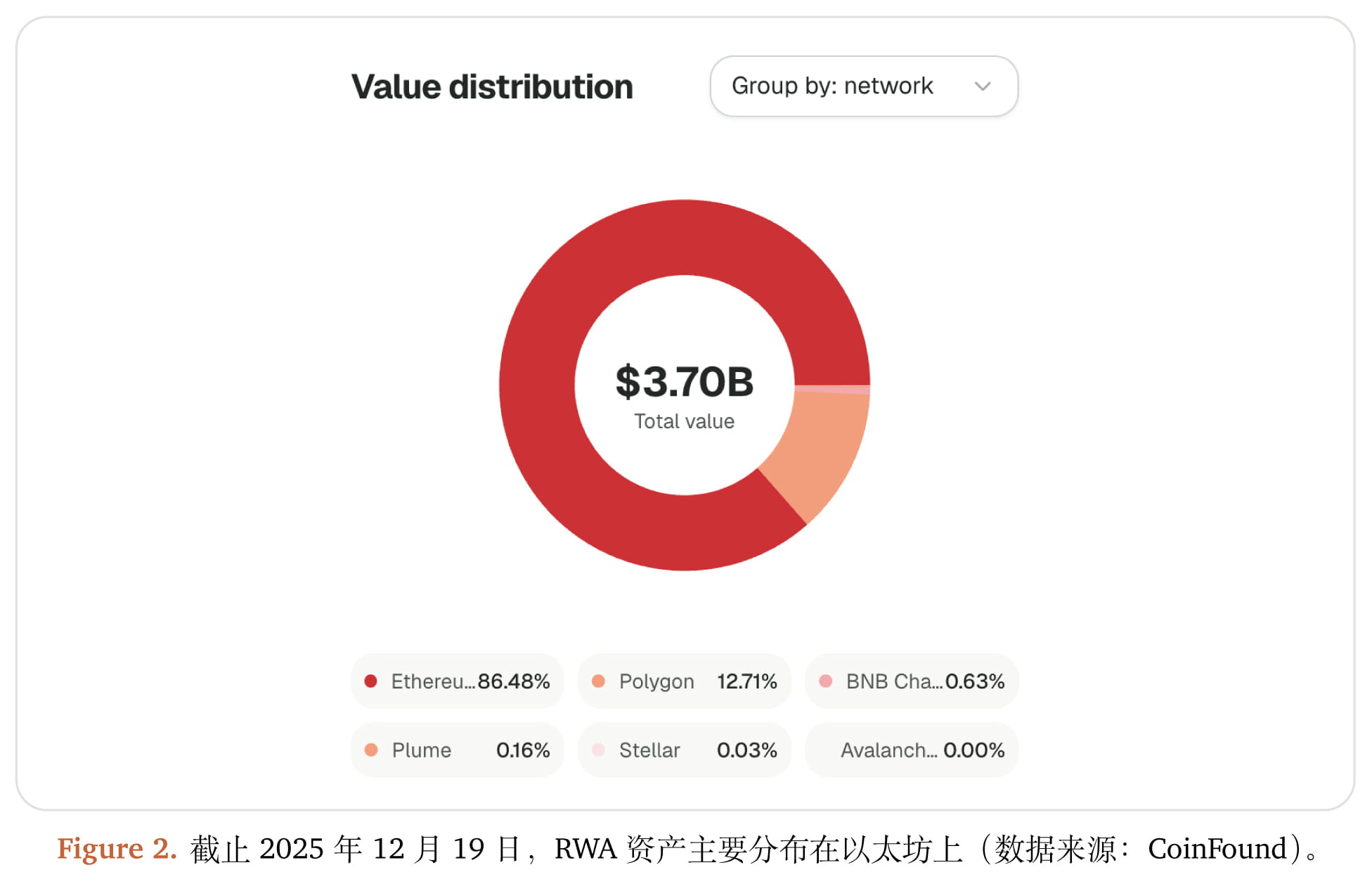

• Gold RWA assets are primarily distributed on the Ethereum blockchain.

1.2 Market Landscape: XAUt and PAXG dominate the market, while emerging players show remarkable growth.

• XAUt (Tether Gold): The Dominator of Liquidity and Derivatives

As of December 19, 2025, XAUt's market capitalization was approximately US$1.63 billion, firmly holding the top position in the sector.

• Core Advantages: Leveraging Tether's vast stablecoin ecosystem, XAUt boasts the deepest liquidity among gold RWA tokens, making it the preferred gold collateral for centralized exchanges (CEXs) and on-chain derivatives protocols.

• Applicable scenarios: Suitable for high-frequency traders and institutions as a large-scale hedging tool.

• PAXG (Paxos Gold): A Benchmark for Compliance and Regulation

As of the same period, its market capitalization was approximately US$1.43 billion.

o Core Advantages: As an asset regulated by the New York State Department of Financial Services (NYDFS), PAXG offers the highest level of transparency in the industry. Its most distinctive feature is "transaction-by-transaction lookup," where users can simply enter their Ethereum address to retrieve the corresponding gold bar's serial number, purity, and weight.

o Applicable scenarios: It is highly favored by traditional regulated institutions that are extremely sensitive to audit risks.

• KAU (Kinesis Gold): Payments and Financial Inclusion

As of December 19, 2025, KAU's market capitalization has steadily climbed to $300 million.

o Core Innovation: Gold Yield Mechanism. Unlike "static assets" such as XAUt and PAXG, KAU introduces a yield model. By returning a certain percentage of network transaction fees to holders, KAU breaks the limitation of gold as a non-productive asset.

o Payment ecosystem: Relying on Kinesis's debit card system, KAU has enabled "gold-swipe consumption" in more than 40 regions, truly transforming gold into a highly liquid everyday currency.

• XAUm (Matrixdock Gold): Profitability and Flexibility

o XAUm performed exceptionally well in 2025, with its market capitalization soaring from the millions of dollars at the beginning of the year to over 60 million dollars, demonstrating its strong institutional appeal.

o Technical Features: Dual-mode asset form. XAUm innovatively supports the exchange between ERC-20 (fungible tokens) and ERC-721 (NFTs). Ordinary users hold tokens, and when the accumulated amount reaches a whole gold bar (e.g., 1kg), it can be packaged into an NFT representing ownership of a specific gold bar, greatly balancing transaction flexibility and transparency of physical ownership.

o DeFi Engine: As a member of the Matrixport ecosystem, XAUm is deeply integrated with various DeFi strategies, allowing users to enjoy rising gold prices while capturing arbitrage profits across different public chains through cross-chain communication protocols (such as Chainlink CCIP). This enables gold to not only serve as a store of value but also generate returns within the DeFi ecosystem.

1.3. Increased participation of institutional investors

• The entry of financial giants and productization:

DBS and Standard Chartered's pilot program: Under the regulatory framework of the Monetary Authority of Singapore (MAS), these traditional banks launched a pilot program in 2025 for cross-border settlement based on gold RWA. They used tokenized gold to replace the movement of traditional physical gold bars, reducing settlement time from days to minutes.

• Institutionalization of managed facilities:

The widespread adoption of multi-signature custody solutions: By 2025, institutional-grade custody platforms such as Fireblocks and Copper will have fully integrated XAUt, PAXG, and XAUm. This means that family offices and hedge funds will no longer need to directly manage private keys, but will instead perform "vault-level" operations through an enterprise-grade interface compliant with the SOC2 standard.

o Phemex Institutional Account System: Trading platforms like Phemex, through their institutional-grade APIs and sub-account system, allow institutional investors to directly use gold tokens as cross-platform margin collateral, significantly improving capital utilization.

• Maturity of the regulatory and compliance system:

o Impact of the US GENIUS Act: The GENIUS Act (Stablecoin Act), passed in July 2025, provides a clear legal definition for physically backed tokens (including gold tokens), greatly reducing legal concerns for institutional investors.

§ Real-time Proof of Reserves (PoR) Becomes an Industry Standard: By the end of 2025, mainstream gold RWA projects had widely adopted the Chainlink PoR oracle. For example, PAXG and XAUm both support 24/7 on-chain auditing, allowing institutional investors to access physical gold bar inventory snapshots from custodian banks (such as Paxos Trust or Matrixport partner banks) at any time.

2. Macro Perspective and Trends 2.1 Unstable macro environment leads to continued rise in gold and gold RWA prices.

In 2025, the global macroeconomic environment will exhibit a high degree of uncertainty.

On the one hand, both debt pressure and fiat currency credit risk are rising. As public debt levels in major economies have reached historical highs, investor confidence in sovereign fiat currencies is structurally weakening. Demand for non-debt assets is expected to reach a ten-year high in 2025.

On the other hand, it's not just inflation risks; geopolitical conflicts are also exacerbating instability in the macroeconomic environment.

In this context, gold has become increasingly important as a safe-haven asset. Gold prices continued to rise throughout 2025, repeatedly hitting new historical highs. Similarly, this has driven up the price of gold RWA assets. In the short term, this trend is expected to continue significantly.

2.2 From stablecoins to payments and other scenarios, the demand for "on-chain gold" is expanding.

With the development of stablecoins, the application of on-chain financial assets in scenarios such as payment and transaction clearing and settlement has been widely verified and is developing rapidly.

However, a noteworthy phenomenon is:

Currently, the underlying assets of mainstream stablecoins such as USDC are US dollar cash equivalents and short-term US Treasury bonds, but their total reserves are only slightly over one trillion US dollars, which is clearly insufficient to support global applications. If the scope is expanded to include long-term US Treasury bonds or other risky assets, stablecoins will inevitably bear similar maturity and credit risks as commercial banks.

However, on the other hand, due to the instability of the global macroeconomic environment, diversification has become an important consideration in order to ensure the stability of the underlying asset value in payment, clearing and settlement, and even future collateralization scenarios. A still-popular example is USDT and Tether. In recent years, Tether has been continuously increasing the proportion of gold and Bitcoin in its reserve assets and has been increasing its gold reserves to enhance its resilience against inflation and credit risk of US Treasury bonds.

In short, the current "on-chain financial world" needs "gold," and this demand is expanding, driven by the development of stablecoins and application scenarios such as payments and clearing and settlement.

However, physical gold and gold ETFs are insufficient to meet the demand:

The physical form of gold severely limits its feasibility as a payment medium. Within the existing financial system, gold lacks programmability, divisibility, and high-frequency liquidity, making it difficult to integrate into modern financial networks, especially failing to meet the needs of cross-border payments and on-chain finance. Compared to digital assets such as fiat currency and stablecoins, physical gold cannot be directly used for electronic settlements and lacks the ability to interact with infrastructure such as payment gateways, clearing networks, and smart contracts.

Similarly, while gold ETFs offer convenience for gold investment within the traditional framework, their adaptability and flexibility are clearly insufficient in an "on-chain" context, making it difficult to meet the core requirements of the decentralized era for assets to be "highly active, readily available, and composable." Specifically, while gold ETFs serve as an important tool connecting the gold market and the financial market, allowing investors to obtain price exposure without actually holding physical gold, they are essentially still restricted products within the traditional financial system. In particular, gold ETFs are securitized assets, unable to achieve peer-to-peer transfers or real-time settlements, making them difficult to use for payments, and lacking the ability to embed on-chain financial protocols.

Additionally, gold ETFs have an extra drawback for investors: purchasing a gold ETF only grants legally recognized equity certificates, not ownership of the gold itself. Essentially, it remains a "closed-end financial instrument."

Therefore, the on-chain world needs "gold," and it needs a "form-matching" gold, specifically:

• To provide a reliable, stable, and composable value anchor for the on-chain world that needs "gold" to act as a credible "asset component".

• It requires "gold" and must be programmable and composable, allowing for flexible integration with DeFi ecosystem lending protocols, liquidity pools, and yield aggregation mechanisms.

Therefore, the demand for gold-based RWAs has emerged.

Core advantages

Scope of application

physical gold

No counterparty risk (personal ownership), physical realism, absolute risk aversion in extreme environments, and no reliance on numbers.

Long-term wealth transfer, physical reserves, gifts, and personal non-liquid collections.

Gold ETF

Extremely high secondary market liquidity (stock market), subject to strong regulatory audits, no need to worry about physical storage, and low transaction costs.

Traditional stock account holders, institutional asset allocation portfolios, and intraday swing trading.

Gold RWA

24/7 trading, atomic splitting, on-chain composability (DeFi), cross-chain transfer, and real-time reserve auditing (PoR).

On-chain payment clearing, DeFi collateralized lending, cross-protocol yield strategies, high-frequency global hedging, and programmable financial management.

2.3 A new generation of financial system is emerging, and gold RWA is an important component.

In December 2025, the U.S. Securities and Exchange Commission (SEC) issued a No-Action Letter to the Depository Trust Company (DTC), a subsidiary of the Depository Trust and Clearing Corporation (DTCC), authorizing it to provide tokenization services for certain real-world assets in a controlled production environment. This authorization covers highly liquid assets such as U.S. stocks, ETFs, and U.S. Treasury bonds, opening a compliant channel for traditional capital markets to "go on-chain" and demonstrating that mainstream regulation is supporting the practice of asset tokenization.

Going back further, in the second half of 2025, SEC Chairman Paul Atkins repeatedly stated publicly that "asset tokenization is the future trend of capital markets" and promoted discussions related to Project Crypto, including the classification framework and regulatory applicability of tokenized securities. Even earlier, the passage of the GENIUS Act (2025) laid the legal foundation for the compliant use of stablecoins and the on-chaining of assets.

It appears that in the United States, the tokenization of financial assets is accelerating with regulatory support, and "asset tokenization" seems to be the next generation of financial system form.

Moreover, this trend is not limited to the United States; rather, it is evolving into a common direction at the global financial system level.

The Bank for International Settlements (BIS), in its 2025 Annual Economic Report, outlined a framework for the technological form and asset structure of the "next-generation financial system." The BIS explicitly states that the traditional financial system is moving from an architecture centered on accounts and centralized ledgers to a new paradigm based on tokenization and programmable platforms. The BIS describes this system as a financial infrastructure operating through multiple types of tokenized assets, including:

• Tokenized form of central bank reserves (as the final settlement asset of the system).

• Commercial bank deposit tokens or regulated stablecoins (as payment and liquidity instruments).

• Tokenized forms of government bonds and other high-quality assets (serving as collateral for safe assets and financial markets).

BIS emphasizes that the core value of tokenization lies not in "simply mapping assets to the blockchain," but in integrating payments, clearing, settlement, and asset transfer onto the same programmable infrastructure, thereby significantly reducing cross-border transaction costs, shortening settlement cycles, and reducing systemic friction. This assessment is highly consistent with the SEC's support for securities tokenization and the DTCC's promotion of on-chain clearing and settlement practices.

Naturally, within this framework, Real-World Assets (RWAs) are seen as a crucial bridge connecting the real-world financial system with on-chain financial infrastructure. Among various RWAs, gold holds a unique position: as a globally recognized store of value, a long-term safe asset, and high-quality collateral, it naturally meets the "highly trustworthy, low-credit-risk asset" requirements emphasized by the BIS. When gold is introduced into the on-chain system in the form of an RWA, it can not only exist as a store of value but also participate in core financial functions such as on-chain payments, clearing, collateralization, and cross-border settlements.

In short, a new generation of financial system is emerging, and this system requires gold in the form of "RWA".

3. Uses of Gold (RWA) 3.1 Programmable "Safe-Haven Asset"

Gold has long been recognized globally as a safe-haven asset and a store of value, and the RWA Gold ETF further enhances this by introducing programmability and financial composability. This brings additional benefits:

• Divisible and composable: Gold can be broken down into the smallest units of value and embedded in DeFi, custodial accounts, or institutional financial contracts;

• Programmable rules: By setting transfer, locking, liquidation, or triggering conditions through smart contracts, gold can be transformed from a "passively held asset" into an "asset that actively participates in financial logic";

• On-chain transparency: The custody, issuance, circulation and redemption paths are verifiable on-chain, reducing reliance on centralized intermediaries.

One direct manifestation of these benefits is the ability to generate returns while "hedging." For example, XAUm holders can participate in protocols such as AlphaLend, Navi, and Suilend to earn returns.

3.2 Value Mediums in Payment, Transaction and Cross-border Payment Networks

Beyond its functions as an inflation hedge and store of value, gold can also be embedded in the future digital financial system as a medium of exchange and a payment asset. For example, with the emergence of stablecoins and the rapid expansion of RWA, gold tokens are expected to become a neutral payment interface linking on-chain finance and the real economy.

Specifically, the current stablecoin system exhibits a clear dollar-centric characteristic, with its underlying asset structure highly concentrated in US Treasury bonds. While this structure enhances liquidity, it also introduces geopolitical, regulatory spillover, and credit concentration risks. The emergence of gold tokens provides an institutional buffer for this system.

Against the backdrop of a gradually multipolar global payment network (with local currency settlement systems such as mBridge and BRICS Pay developing in parallel), gold tokens have the potential to become "bridging clearing assets":

• It will not replace sovereign currencies;

However, as a neutral interface between different monetary systems and payment networks, it reduces friction and the cost of political maneuvering.

In this architecture, the role of gold RWA has far exceeded that of an "investment asset," evolving into an institutional-level foundational component of a new generation of global financial networks. At this level, gold RWA may not be competing with stablecoins, but rather forming a strategic complement in their liquidity structure: stablecoins handle high-frequency circulation, while gold RWA provides a low-credit-risk value foundation.

3.3 Core Collateral in On-Chain Clearing and Settlement and Collateral System

On the one hand, in DeFi scenarios, gold tokens (such as XAUT and PAXG) are gradually being regarded as "neutral collateral." Unlike fiat stablecoins, gold does not rely on any single sovereign credit; its price is determined by global market consensus, giving it greater stability in extreme macroeconomic or geopolitical situations. This makes it an important supplement to hedging the systemic risks of stablecoins in lending, synthetic assets, and structured protocols.

On the other hand, in the CeFi and derivatives markets, gold RWA can also represent a structural innovation in the margin system. Leading trading platforms can support gold tokens as cross-currency margin assets, enabling institutional investors to participate in leveraged trading and risk hedging directly with gold positions without converting them into fiat currency or stablecoins. This mechanism essentially realizes the "release of gold capital efficiency": gold is no longer just a passively allocated asset, but becomes a liquid unit that can continuously participate in financial activities.

3.4 "Bridge Assets" Connecting Traditional Finance and On-Chain Finance

From a systems perspective, a key role of Gold RWA is lowering the barriers for traditional financial institutions to enter the on-chain system. For banks, asset management institutions, and clearing institutions:

Gold is a familiar asset;

• Custody, auditing, and compliance pathways are relatively mature;

• It has a clear legal nature and high acceptance across jurisdictions.

Therefore, gold RWA often becomes the entry point for institutions to first try on-chain assets, on-chain liquidation, or on-chain collateral, and is an important "transitional asset" for traditional finance to move towards the tokenized world.

4. Risks and Challenges

While Gold RWA demonstrates significant advantages in liquidity, capital efficiency, and institutional neutrality, as a hybrid form connecting real-world assets with the on-chain financial system, it still faces a series of structural risks and practical constraints. These risks do not negate the long-term value of Gold RWA, but at the current stage of development, they must be systematically identified and assessed.

4.1 Centralization Risk

4.1.1 Physical Custody and Redemption Risks

The core premise of Gold RWA is the one-to-one correspondence between on-chain tokens and off-chain physical gold. This relationship decisively relies on real-world custodian institutions, vault operators, and redemption mechanisms, thus inevitably introducing centralized trust. The main risks are:

• Custody concentration risk: Most gold RWA projects rely on a few international treasuries or custodians. In the event of operational disruptions, legal disputes, or extreme political events, the ability to redeem tokens may be affected.

• Redemption friction: Physical redemption often has minimum quantity thresholds, geographical restrictions, and time costs, which partially offset the "on-chain immediacy" in off-chain processes;

• Liquidity disruption in extreme scenarios: In systemic crises or regulatory conflicts, on-chain tokens may remain in circulation, but off-chain physical delivery is restricted, resulting in a mismatch between "nominal liquidity" and "real liquidity".

Therefore, while the RWA (Rated Waiver of Gold) has improved the financial availability of gold, its security still highly depends on the robustness and legal enforceability of the custody system.

4.1.2 Operational and Transparency Risks

The value of RWA gold comes not only from gold itself, but also from the market's trust in the issuer, custodian, and auditing mechanisms. Potential risks include:

• Insufficient audit frequency and depth: Although some projects provide reserve certificates, the audit cycle is too long or lacks real-time timeliness, which makes it difficult to meet the institutional-level risk control requirements;

• Information asymmetry: Custody details, redemption terms, and legal structure are often scattered across multiple documents, making it difficult for ordinary users to fully assess them;

• Reputation spillover effect: If a credit incident occurs in an individual Gold RWA project, it may have a negative impact on the entire sector and affect market acceptance.

At this level, the risk characteristics of gold RWA are closer to those of a "financial infrastructure-level product," and its success or failure depends heavily on long-term reputation building rather than short-term market performance.

4.2 Technological Risks: Systemic Challenges of On-Chain Financial Complexity

Although Gold RWA operates on a mature public blockchain, its technology stack typically involves multiple complex components such as smart contracts, cross-chain bridges, oracles, and custodial interfaces. The overall security of the system depends on the weakest link.

Key technological risks include:

• Smart contract vulnerability risks: Vulnerabilities in token minting, destruction, mapping, and cross-chain logic may lead to asset freezing, mismatch, or malicious exploitation.

• Cross-chain and interoperability risks: Cross-chain bridges have always been a high-risk area for on-chain security incidents. Once Gold RWA becomes a cross-chain liquid asset, its systemic risk exposure will increase accordingly.

• Oracle and data synchronization issues: Delays or errors in the on-chain synchronization of price, status, or reserve information may trigger cascading liquidations or market distortions.

Unlike native crypto assets, the technical risks of Gold RWA not only affect the token itself, but may also propagate to broader financial protocols through staking, liquidation, and payment systems, exhibiting stronger systemic spillover effects.

4.3 Regulatory Uncertainty Risk: Long-Term Variable Across Jurisdictions

Gold RWA sits at the intersection of commodities, securities, payment instruments, and digital assets, and its regulatory attributes vary significantly across different jurisdictions, which constitutes a long-term uncertainty.

This is mainly reflected in:

• Inconsistent legal characterization: Gold tokens may be regarded as commodity tokens, security tokens, or payment instruments in different countries, and the applicable compliance frameworks vary considerably;

• Complexity of cross-border compliance: Gold RWA naturally possesses cross-border flow attributes, but in reality, foreign exchange management, precious metal regulation, and anti-money laundering rules are still mainly based on the principle of territoriality.

• Inconsistent policy pace: Even as regulation becomes more open in major markets such as the United States and the European Union, the attitudes and enforcement efforts of different regulatory agencies may still change in stages.

This means that in the short term, gold RWA is more suitable to be promoted through institutional pilots, compliance sandboxes, and limited-scale applications, rather than boundless expansion.

Risk Warning

This report, based on publicly available information, industry interviews, third-party research, and a reasonable analytical framework, aims to explore the development trends and potential impacts of Gold RWA (Real-World Asset Tokenization). However, due to limitations in market development stages and information disclosure conditions, the conclusions still face the following major risks and uncertainties, which are hereby noted:

I. Risks Related to Data Integrity and Statistical Standards

Gold RWA is still in a phase of rapid evolution. Data on market size, circulation, and use cases mainly come from project disclosures, on-chain statistical tools, and third-party research institutions. Different sources may differ in statistical definitions, calculation methods, and time dimensions. Some data may be outdated, estimated, or have insufficient sample coverage, thus affecting the accuracy and comparability of the analysis results.

II. Risks Related to Asset Custody and Redemption Execution

The value of Gold RWA relies on the physical existence of off-chain gold, compliant custody, and enforceable redemption arrangements. Although mainstream projects typically employ third-party custody and auditing mechanisms, risks such as delayed redemptions, restricted redemptions, or a mismatch between on-chain liquidity and off-chain settlement capabilities may still arise in cases of extreme market volatility, legal disputes, or cross-jurisdictional conflicts.

III. Technical and Systemic Operational Risks

Gold RWA typically relies on smart contracts, public blockchain infrastructure, cross-chain protocols, and oracle systems to operate. Its overall security depends on the coordinated stability of these multiple technical components. Potential contract vulnerabilities, cross-chain mechanism failures, abnormal oracle data, or network congestion can all adversely affect asset transfer, collateral liquidation, and payment settlement functions, and trigger systemic risk spillover.

IV. Uncertainty in Regulatory Policies and Legal Environment

Gold RWA involves the cross-identification of its commodity, security, and payment attributes, and there are significant differences in regulatory classification, compliance requirements, and policy pace across different countries and regions. Future adjustments to the regulatory framework, changes in enforcement standards, or tightening of cross-border compliance requirements may have a substantial impact on the issuance, circulation, custody, and use cases of related products.

V. Market Liquidity and Price Volatility Risks

Although gold itself possesses long-term value stability, the secondary market for gold RWA is still in its early stages of development, with its liquidity depth, participant structure, and price discovery mechanism not yet fully mature. Under certain market conditions, the trading price of gold RWA may deviate from the value of the underlying asset.

VI. Research Hypotheses and Forward-Looking Risk Assessment

Some of the analyses in this report are based on forward-looking judgments on industry development trends, technological paths, and policy directions. The relevant assumptions may be adjusted due to changes in the macro environment, technological progress, or regulatory changes, and the actual results may differ from expectations.

VII. This report does not constitute investment advice.

This report is for research and information exchange purposes only and does not constitute any form of investment advice, offer, or commitment. Investors should make independent judgments based on their own risk tolerance and bear the relevant risks themselves.