Everyone should thoroughly dispel the myth of high valuation VC projects.

Currently, there is a huge gap between the **'primary market valuation bubble' and 'secondary market real liquidity'** in the crypto market.

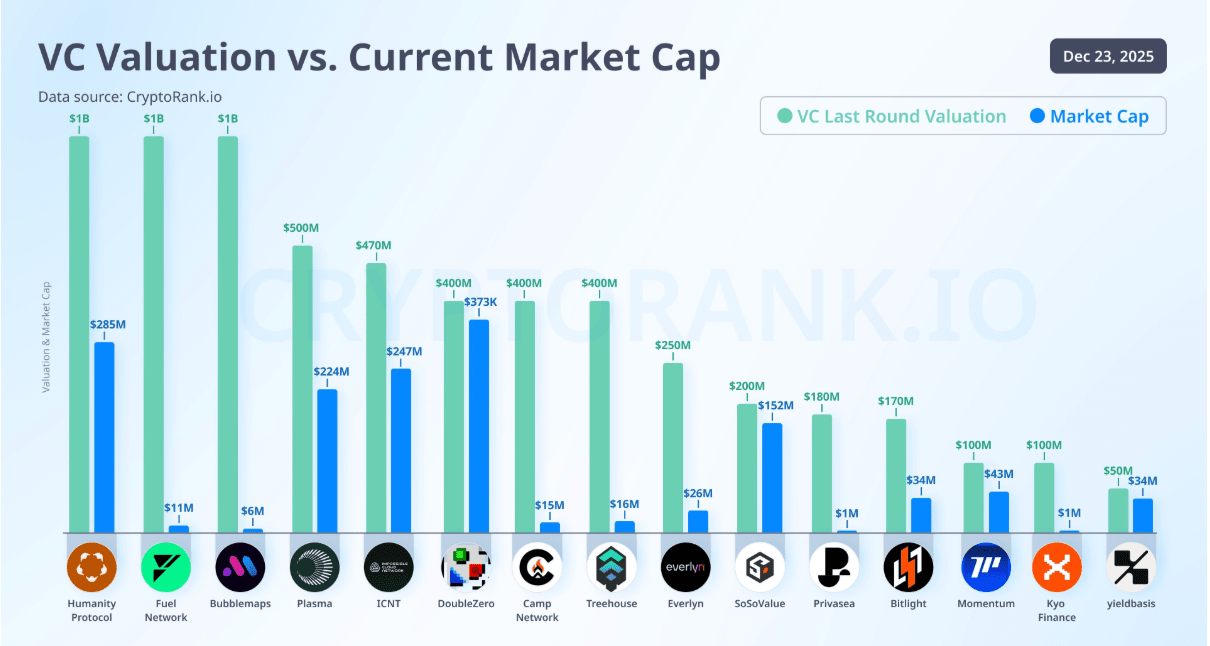

The VC valuation and current market value comparison chart released by CryptoRank shows that

most projects have seen their market value drastically shrink compared to venture capital valuations.

Correction of excessively high valuations after a shift in market sentiment.

The past 'unicorns' are in a miserable state in the secondary market;

This is not only a shrinkage in market value but also a collective dispelling of the **'VC myth'**.

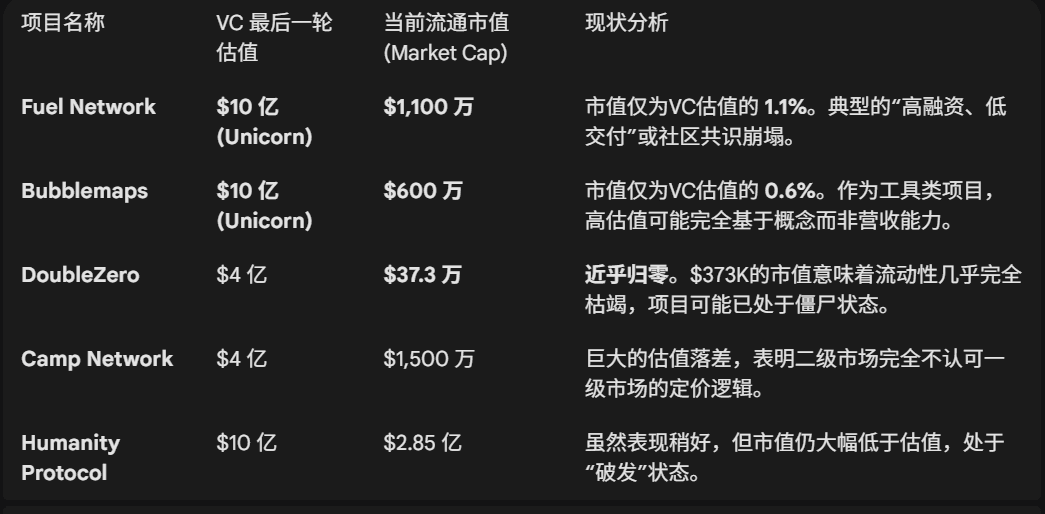

Among them, the VC valuations of Humanity Protocol, Fuel Network, and Bubblemaps are all $1 billion, but their current market values are only $285 million, $11 million, and $6 million, respectively.

Projects like Plasma, ICNT, DoubleZero, Camp Network, and Treehouse have market caps far below their VC valuations, at $224 million, $247 million, $373,000, $15 million, and $16 million respectively.

In addition, projects like Everlyn, SoSoValue, Privasea, Bitlight, Momentum, Kyo Finance, and Yieldbasis also have market caps below their VC valuations, with Everlyn's market cap only at $26 million while its VC valuation reaches $250 million.

Why has everyone 'de-mystified'?

The failure of VC pricing power:

In the past, 'top VC investments' were a signal for retail investors to charge forward;

Now, high VC valuations are often seen as **'scythe warnings'**.

The market shows that VC pricing in the private placement stage has completely detached from the actual market absorption capacity.

Refusing to become 'Exit Liquidity':

This huge price difference indicates that retail investors in the secondary market are no longer blindly buying.

When VC costs are extremely low and valuations are extremely high, token unlocks mean significant selling pressure.

Retail investors' strategies are now more cautious.

Narrative > Substance's end:

Many high-valuation projects (like Fuel, Bubblemaps) have grand technological narratives,

but lack real on-chain revenue or user retention.

When the tide goes out (market sentiment shifts), these high-valuation projects without moats suffer the most.

How to avoid pitfalls?

Based on this phenomenon, when conducting Web3 investment research, the following dimensions can be added for consideration:

Beware of 'heavenly doomed' projects:

For those projects with massive funding amounts, VC valuations extremely high (like >$100 million), but low community enthusiasm and slow product delivery, be extremely careful.

Pay attention to FDV/MC ratio:

Do not only look at circulating market cap (MC), but also consider fully diluted valuation (FDV). If a project currently has a very low market cap (like $10M), but a high FDV (because VCs hold a large number of tokens yet to be unlocked), this is not undervaluation, but rather potential massive selling pressure.

Look for 'community pricing' projects:

The current trend is shifting towards fair launches or projects starting at low valuations, which have healthier chip structures, rather than being controlled by a few VCs.

The Internet of Everything, Digital is King | For more airdrop activities, focus on #welinkBTC

Focus on Web3, blockchain gaming, AI, AirDrop investment opportunities 🫙 Monitor 100 influencers in the crypto space🔥 Let's navigate through bull and bear markets together $BNB