One of the questions that are not asked frequently enough is what makes people purchase utility tokens over and over again, not at the time of its release. Hype cycles fade. Airdrops get dumped. The first listings are corrected and spike. The only difference between a token that has sustainable demand, and one that had an excellent first week is whether the underlying system actually needs the token to be in operation - and whether that system continues to expand.

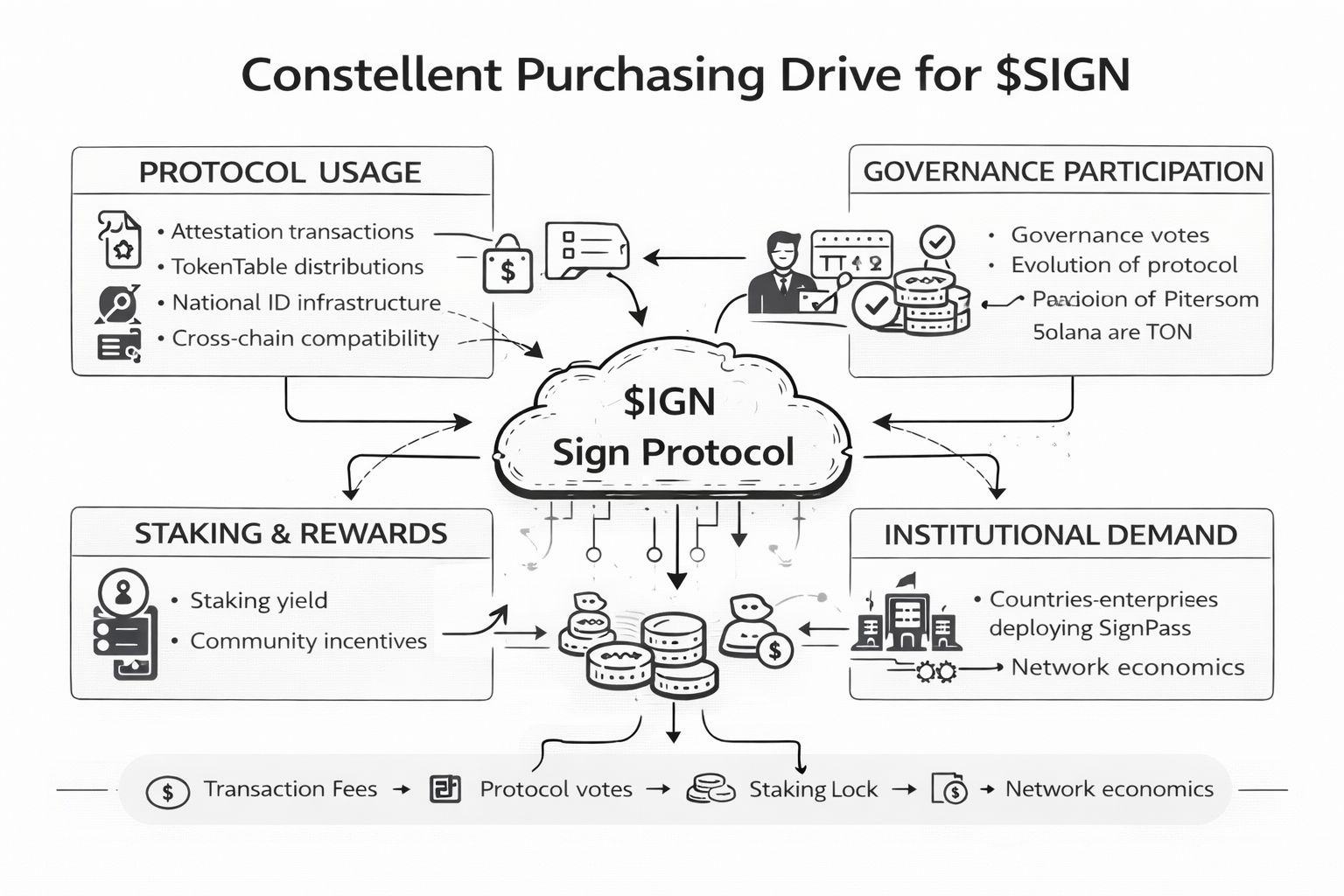

In the case of @SignOfficial , the response begins with the real usage of the protocol. Any attestation that has been handled by Sign Protocol attracts a transaction fee. Each token distribution that is operated using TokenTable creates network activity. National identity infrastructure built by any government using SignPass creates substantial transaction volume on a regular basis. These aren't one-time events. They are operating expenses that incur each time the system is utilized - and with a larger scale in the number of chains, institutions and countries that the protocol is applied to, the frequency of such transactions multiplies. The fact that the fees are specified in terms of $SIGN implies that the actual usage is directly converted into token demand. That is a structural correlation between price and adoption which does not rely on sentiment.

The governance layer introduces one more layer. $SIGN holders are involved in choices of the evolution of the protocol - which chains are given priority, how the fee structure is changed, how ecosystem funds are distributed. The participation in governance is not philosophical only. Governance rights are weighty in real-life protocols involving real income and real institutional customers. Users wishing to have an input into a system that handles billions of tokens being distributed and with sovereign governments as its patrons have a tangible impulse to own and hold $SIGN instead of selling into every spurt.

Next is the staking and rewards layer. The ecosystem gives 40th of total supply to community incentives - a large sum meant not to encourage short-term speculation but to encourage long-term participation. The mechanisms of staking that tie tokens in exchange to yield decreases the supply circulating with time, which is important in a market where the availability of float has a direct impact on price sensitivity. All tokens in a staking contract represent a token that is not on an exchange order book to be sold.

The institutional aspect is an aspect that should be considered. SIGN is not operating a few small applications. It is used in the UAE, Thailand as well as Sierra Leone. It has a CBDC infrastructure agreement to Kyrgyzstan. It made 15 million dollars in 2024 with a physical product line that businesses and governments are charged to utilize. As the institutional deployments become larger, the participants in playing the game, be they government agencies, enterprise clients, or ecosystem developers, frequently need to possess or purchase SIGN as a means of engaging in network economics. That is demand not caused by retail speculation. It is provided by long-term and need operation entities.

Here, the cross-chain system is also important. Sign Protocol is compatible with Ethereum, Solana, BNB Chain, Base, and TON, and others. The pool of users and developers that are first interacting with SIGN each time a new chain integration is launched increases. New integration is effectively new distributable surface, not of the token itself, but of the uses of the token which make it demandable.

None of this is a guarantee. Markets of tokens are unstable and adoption curves are seldom curvy. However, the thing that SIGN can do that most tokens cannot is a system, in which the utility of the token is not added as an additional layer, but one that is actually part of the infrastructure. Whether it is governments checking identity, enterprises allocating billions of assets, developers creating credential systems, all of them are built on the same protocol, and that protocol is built on $SIGN. There is the basis on which, when continually experienced, the buying pressure, will, as a rule, build on.