As Jerome Powell’s term as Federal Reserve Chair approaches its end, one major question remains:

Was his policy truly successful… or are the markets telling a very different story?

The answer may not be found in inflation or unemployment data.

It may be found in gold.

Gold is not just an asset.

It is a silent measure of monetary policy credibility.

When the system is stable,

gold tends to weaken.

When the system loses balance,

gold strengthens.

In simple terms:

Economic stability = weak gold

Economic instability = strong gold

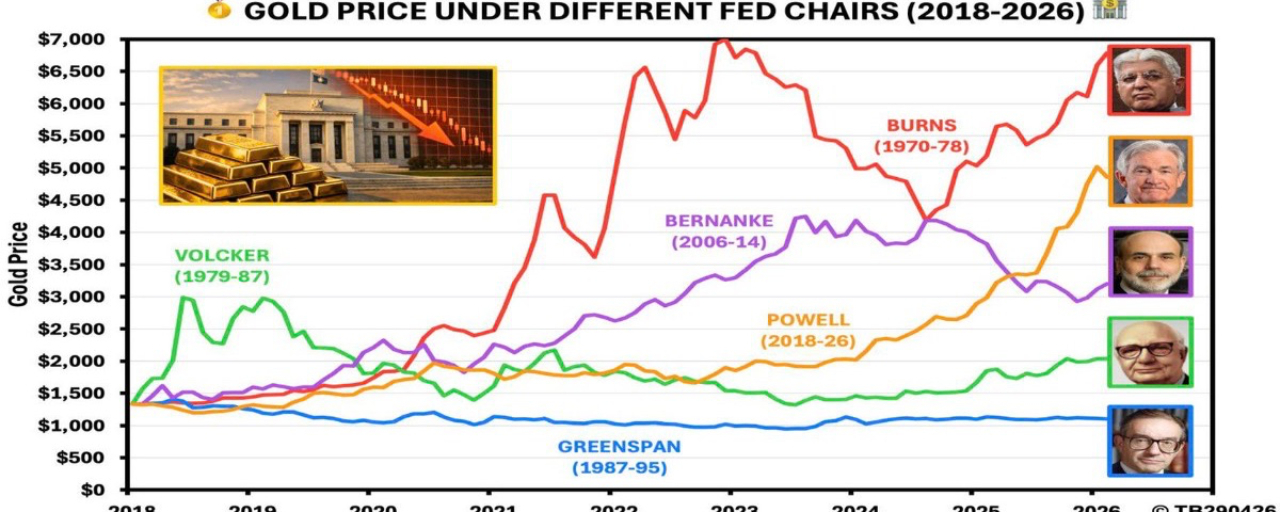

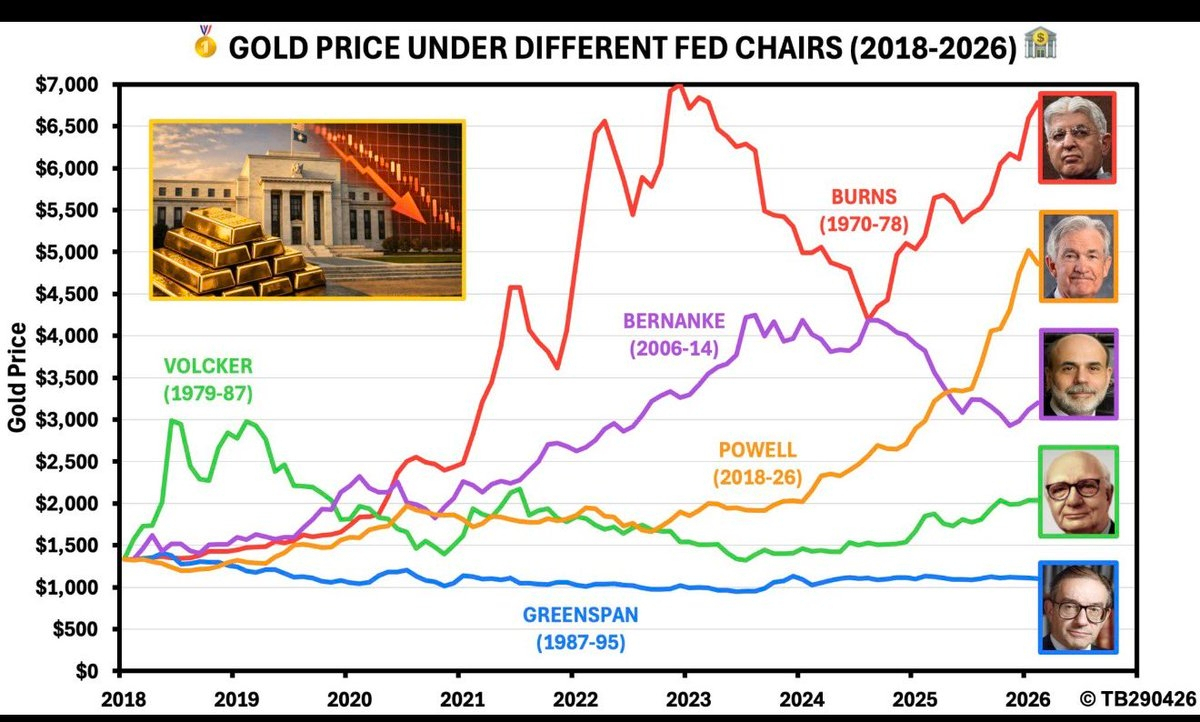

Now let’s look at the numbers.

Gold performance was compared during the first 8 years of the longest-serving Fed Chairs since 1970.

The results were striking:

Burns: +410%

Powell: +265%

Bernanke: +141%

Volcker: +53%

Greenspan: -17%

By this metric, Powell is not among the best.

He is closer to the worst.

Why?

The answer lies in how monetary policy was managed.

The Taylor Rule gives us a simple benchmark:

Were interest rates appropriate relative to inflation?

Under Powell:

Actual interest rate: 2.6%

Suggested rate: 6.1%

That gap is massive.

And it implies policy remained too loose for too long.

This is where the real story begins.

2020–2021:

Massive liquidity injections

while inflation was already accelerating.

2022–2024:

A sudden reversal

with the fastest tightening cycle in decades.

And this pattern is not new.

We saw it before under Burns and Bernanke:

Loose policy

followed by delayed tightening

followed by crises emerging later.

The outcomes were always similar:

• Rising unemployment

• Economic slowdowns

• Financial instability

The only major exception was Volcker.

He tightened early and aggressively.

Painful in the short term,

but he regained control over inflation

and restored confidence in the system.

The takeaway:

The problem is not raising interest rates.

The problem is raising them too late.

When central banks fall behind the curve,

they are eventually forced into extreme tightening.

And the market pays the price.

Today, we may be at that same point again:

• Financial tightening

• Pressure on banks

• A slowing labor market

The real question now is:

Has the impact already peaked?

Or have the biggest risks not appeared yet?

If history repeats itself…

what we are seeing now may not be the end.

It may only be the beginning.