The number I keep failing to find is the active operator count. Newton's entire compliance model runs through a decentralized network of operators who evaluate transactions against policy rules inside Trusted Execution Environments — TEEs — and produce cryptographic proofs confirming the checks were done correctly. NEWT is the collateral those operators stake to participate. Which means operator count isn't a background metric. It's the structural variable the whole demand model rests on. And as far as I can tell, nobody publishes it cleanly anywhere.

That absence is worth sitting with.

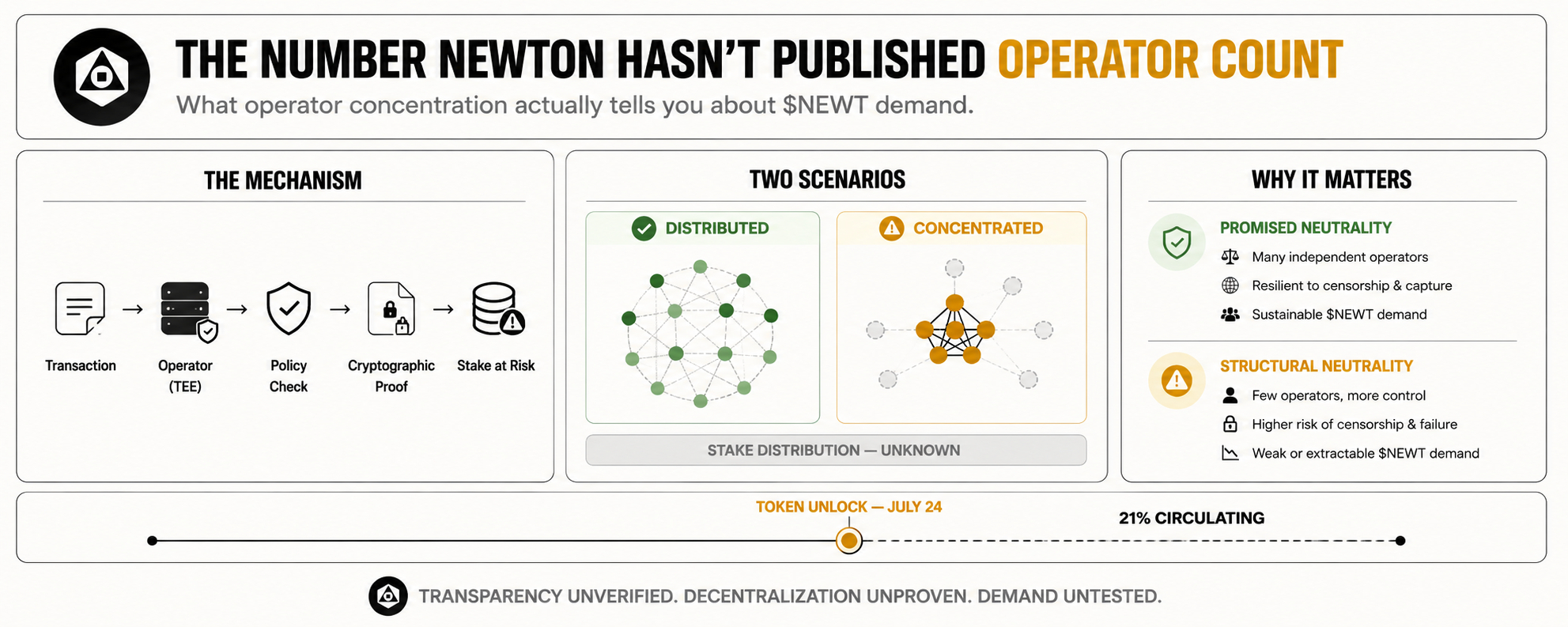

Mechanically, what Newton is selling is credible neutrality. The pitch to institutions and developers is that compliance checks aren't being run by a single party that can be pressured, manipulated, or captured — they're being run by a decentralized set of independent operators whose incentives are aligned through staked collateral. If an operator behaves dishonestly, they lose stake. If they behave correctly, they earn fees. The system only works if there are enough operators that no small group can coordinate to produce false attestations undetected.

The assumption buried inside that model is that operator participation scales with protocol adoption. As more developers integrate Newton's policy client, more transactions flow through the network, more fees are generated, and more operators are economically incentivized to join. Demand for NEWT rises because staking demand rises alongside fee revenue. Clean loop. The problem is that assumption hasn't been tested publicly yet, and the team hasn't answered what the operator set actually looks like today.

In the best case, Magic Labs spent the last year quietly onboarding a distributed operator base through its existing relationships — 200,000 developers, 50 million wallets, enterprise clients like Polymarket and Helium all represent natural on-ramps to a credible early operator network. If those relationships translated into genuine operator participation before the token went public, the decentralization is real and the compliance narrative holds even under scrutiny.

In the less good case, the operator network is still thin. A handful of entities running most of the TEE infrastructure, staking enough NEWT to appear distributed without meaningfully being so. That wouldn't invalidate the technology. But it would quietly undermine the core sales pitch to institutions — which is that the neutrality is structural, not promised. And institutional adoption, which is the demand vector Newton is explicitly chasing after the BeInCrypto Institutional 100 recognition, depends on that distinction mattering to the buyers.

Neither case is legible from the outside right now. The explorer shows proofs. It doesn't show operator concentration, stake distribution, or how many independent entities are actually running the infrastructure. Those are the numbers that would tell you whether the decentralized compliance thesis is already real or still directionally true.

There's also a timing problem. The next token unlock hits July 24 — another 17 million NEWT entering a market where real circulating supply is already only 21 percent of total. If operator demand hasn't grown enough to absorb that supply through genuine staking participation, the unlock lands into a thinner demand base than the tokenomics assume.

The condition that would change how I read this: a published breakdown of active operators by stake size, updated on a cadence that lets you track whether participation is growing or concentrated.